Key Takeaways:

- Integration Momentum: The $35 billion Discover acquisition is delivering expected synergies while unlocking strategic growth opportunities.

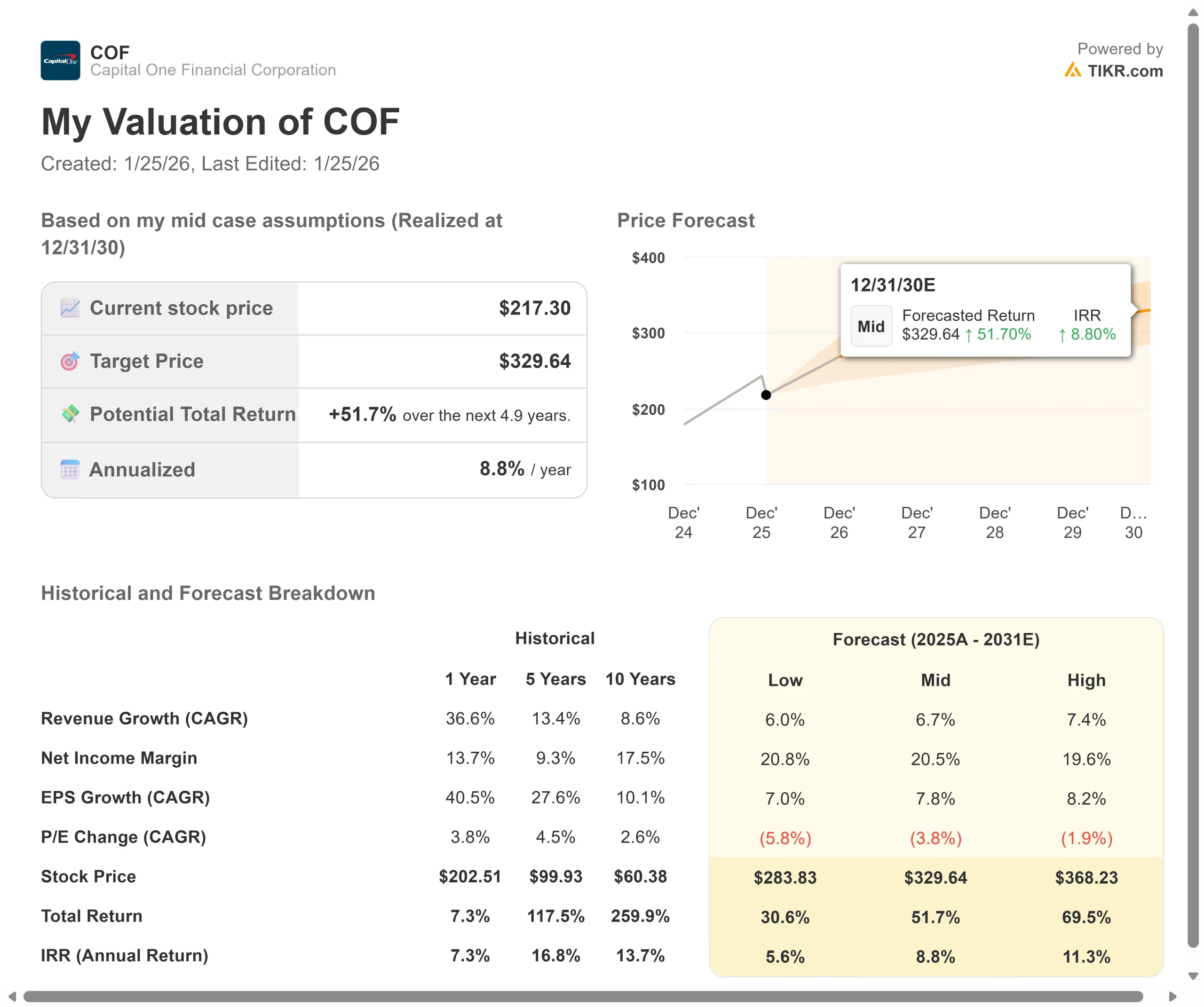

- Price Projection: Based on fundamental analysis, COF stock could reach $329 by December 2030.

- Potential Gains: This target implies a total return of 52% from today’s price of $217.

- Annual Return: Investors could see roughly 9% annual growth over the next 4.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Capital One (COF) closed one of 2025’s most transformative banking deals by acquiring Discover Financial, creating a payments and banking powerhouse. The company now operates one of only four U.S. payment networks and commands the third-largest small business credit card franchise.

- Fourth quarter results showed the strategy working. Revenue jumped 58% year over year, as the combined entity generated $2.1 billion in quarterly earnings.

- Perhaps more importantly, CEO Richard Fairbank announced a $5.15 billion agreement to acquire Brex, accelerating Capital One’s push into corporate payments and spend management.

The company returned $2.5 billion to shareholders through buybacks in Q4 alone and currently trades at $217.

That creates an opportunity for investors who understand Capital One’s transformation from a traditional bank to an integrated payments platform.

See analysts’ full growth forecasts and estimates for COF stock (It’s free) >>>

What the Model Says for Capital One Stock

We analyzed Capital One through the lens of its evolution into a full-spectrum banking and payments company. The Discover acquisition brought immediate scale, adding a payment network and deposit base while creating cross-sell opportunities across consumer and business segments.

The company is pursuing multiple growth vectors simultaneously. At the premium end of consumer cards, Capital One is seeing its strongest growth among heavy spenders.

The national retail banking business continues expanding organically, now enhanced by Discover’s deposit franchise. On the commercial side, Brex brings a modern tech stack and corporate card capabilities.

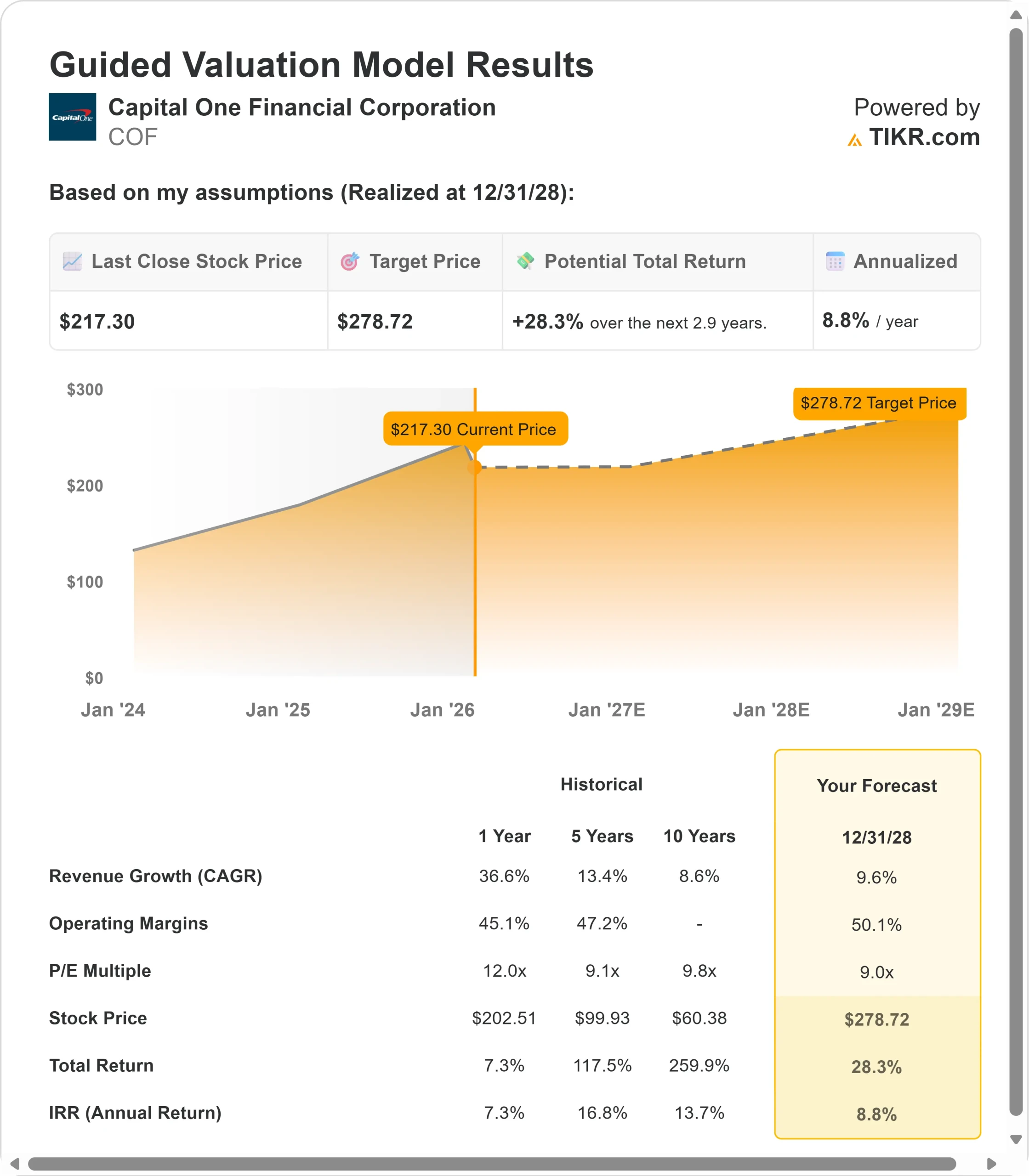

Using a forecast of 9.6% annual revenue growth and 50.1% operating margins, our model projects the stock will rise to $279 within 2.9 years. This assumes a 9.0x price-to-earnings multiple.

That represents modest compression from Capital One’s current P/E of 10.6x. As the company invests heavily in Discover integration, network acceptance, and new growth initiatives like Brex, near-term margin pressure could weigh on the multiple.

However, these investments target long-term franchise building in structurally attractive markets.

The real value lies in execution across three pillars: capturing Discover synergies, scaling the payment network internationally, and leveraging technology for AI-driven products.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for COF stock:

1. Revenue Growth: 9.6%

Capital One’s growth engine spans multiple businesses, creating diversified revenue streams.

Discover Integration Synergies: The company remains on track to deliver expected cost and revenue synergies from the Discover deal. Network economics are already improving as debit conversions complete and credit card migrations begin.

Payment Network Scale: Capital One is aggressively building international acceptance for the Discover network, focusing first on destinations where Americans travel. Every growth opportunity—from merchant acceptance to card issuance—requires this same foundational investment.

Premium Card Momentum: Purchase volume growth is strongest at the top of the market, where Capital One competes for heavy spenders. The company is leaning into marketing and premium benefits to build this franchise despite intense competition.

Brex Acceleration: The Brex acquisition opens the business cards market, where Capital One currently has limited presence. It also brings spend management tools that can enhance existing personal liability offerings and power a national small business bank.

2. Operating margins: 50.1%

Capital One operates with disciplined expense management while investing in future growth.

Investment Cycle: The company is in a heavy investment period across Discover integration, network buildout, AI development, and now Brex. These investments create near-term pressure on the efficiency ratio but target long-term earnings power.

Credit Normalization: Auto charge-offs have stabilized near pre-pandemic levels. Card charge-offs declined 113 basis points year-over-year to 4.93% and appear to be settling out after almost a year of improvement.

3. Exit P/E Multiple: 9.0x

The market currently values Capital One at 10.6x earnings. We assume compression to 9.0x through our forecast period.

Reflects Investment Phase: Capital One’s P/E has averaged 12.0x over the past year and 9.1x over five years. The lower multiple reflects significant near-term investments across multiple initiatives before synergies and growth fully materialize.

Quality Platform Warranted: Capital One deserves a market multiple due to its third-largest small-business card franchise, one of four U.S. payment networks, modern cloud-based technology infrastructure built for AI, strategic Brex capabilities in high-growth corporate payments, and consistent capital generation that enables $2.5 billion in quarterly buybacks.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Banking faces regulatory uncertainty and competitive intensity. Here’s how Capital One stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 6.0% and operating margins compress to around 20.8% (from investments not paying off as expected), the stock still offers a 5.6% annual return.

- Mid Case: With 6.7% growth and 20.5% margins (our base assumptions converted to net income margins), we expect an annual return of 8.8%.

- High Case: If Discover integration accelerates, network monetization succeeds, and Brex captures corporate payment share while maintaining 19.6% margins and growing at 7.4%, returns could hit 11.3% annually.

See what analysts think about COF stock right now (Free with TIKR) >>>

The range reflects different outcomes for Capital One’s ambitious growth agenda.

In the low case, competitive intensity in cards escalates, Discover integration proves costlier, or regulatory headwinds like proposed interest rate caps materialize.

In the upside case, payment network acceptance drives new issuance opportunities, Brex’s corporate platform scales rapidly, and Capital One’s AI investments create differentiated customer experiences across banking and payments.

How Much Upside Does Capital One Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!