Key Takeaways:

- Convergence Strategy: 41% of fiber customers also use AT&T wireless, creating lower churn and higher lifetime values

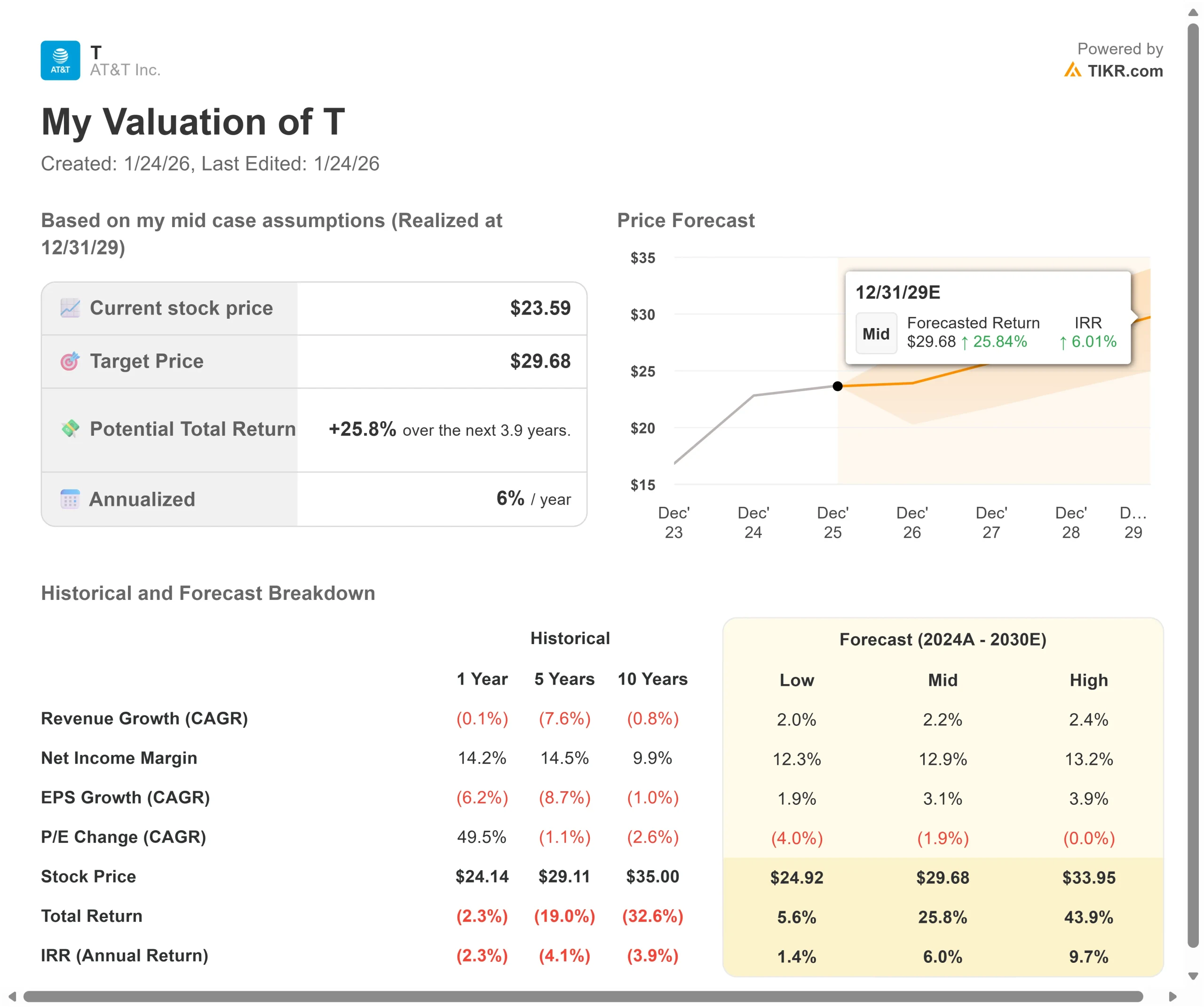

- Price Projection: Based on current execution, the stock could reach $30 by December 2029

- Potential Gains: This target implies a total return of 26% from the current price of $24

- Annual Return: Investors could see roughly 6% annual growth over the next 3.9 years

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

AT&T (T) just delivered its highest broadband additions in over 8 years. The company added more than 550,000 fiber and Internet Air subscribers in Q3, surpassing its performance from a year ago.

CEO John Stankey is executing a deliberate convergence strategy where customers subscribe to both wireless and home internet services. These bundled relationships generate higher revenues and show significantly lower churn than single-product customers.

The results speak for themselves.

- AT&T passed 31 million locations with fiber by Q3 and expects to reach over 60 million by 2030.

- Consumer Wireline EBITDA margins expanded by 350 basis points year-over-year to drive 15% EBITDA growth.

- With strategic acquisitions from EchoStar (spectrum) and Lumen (fiber assets) closing in early 2026, AT&T is positioning itself to lead retail connectivity service revenue by decade’s end.

Despite flat or negative revenue growth over recent years, AT&T stock trades at $24, offering upside for investors who recognize the company’s fiber expansion and fixed wireless opportunity.

See analysts’ full growth forecasts and estimates for T stock (It’s free) >>>

What the Model Says for AT&T Stock

We analyzed AT&T through the lens of its transformation from a legacy telecom into a modern connectivity provider focused on fiber and convergence.

The company is methodically transitioning away from outdated copper infrastructure while investing in fiber buildouts and 5G wireless. With only 41% penetration of wireless services among fiber households, AT&T has significant room to grow converged relationships.

The EchoStar spectrum acquisition will cover nearly two-thirds of the U.S. population by mid-November, accelerating Internet Air expansion. The Lumen fiber assets will add scale to markets where AT&T previously lacked presence.

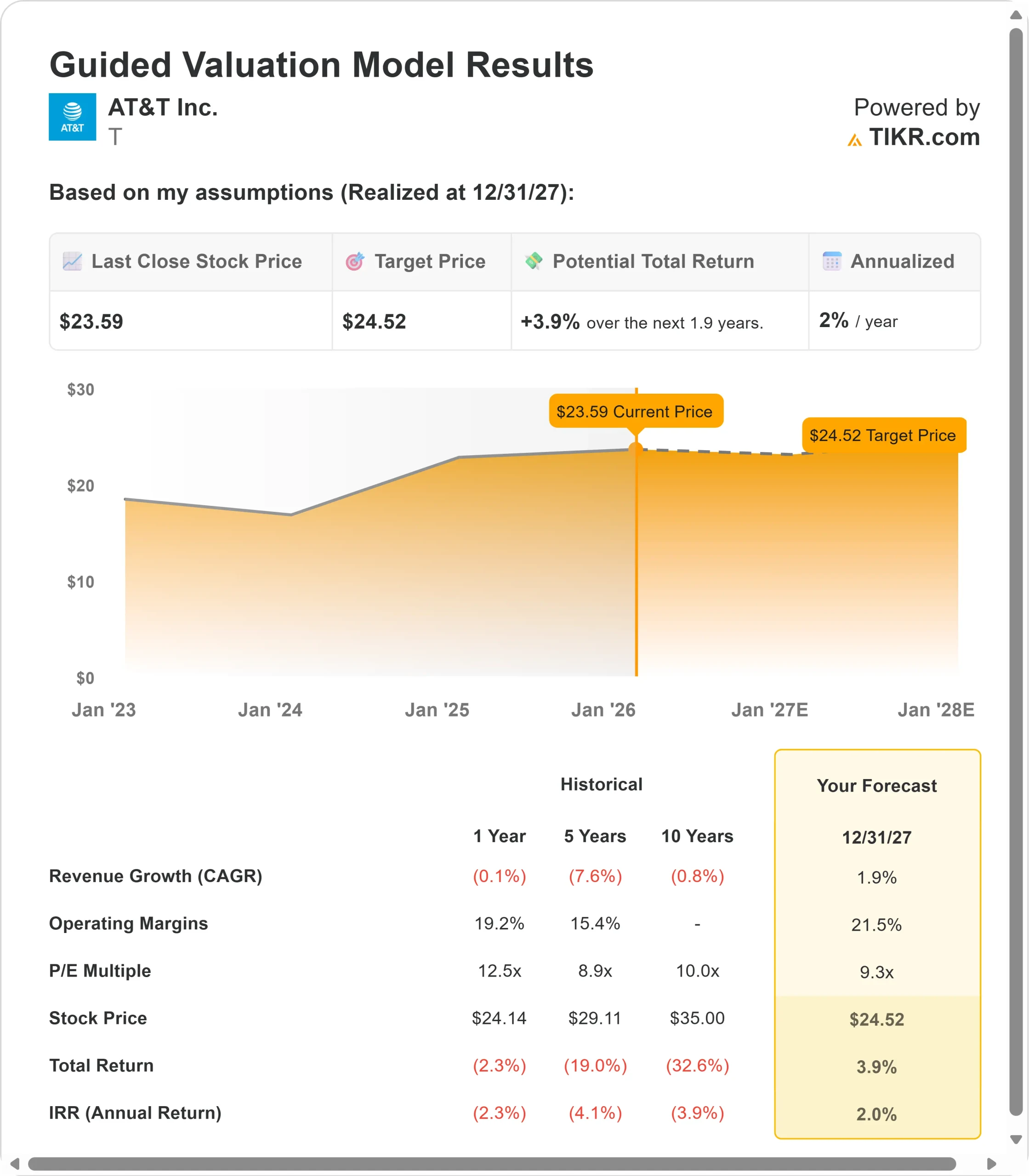

Using a forecast of 1.9% annual revenue growth and 21.5% operating margins, our model projects the stock will rise to $25 within 1.9 years. This assumes a 9.3x price-to-earnings multiple.

That represents a compression from AT&T’s current P/E of 10.9x. As the company invests in fiber expansion and spectrum deployment while managing legacy declines, the multiple faces near-term pressure. However, sustainable margin expansion and improving revenue trends should support gradual multiple recovery.

The real value lies in executing the convergence playbook and completing the transition to a simplified, higher-margin business model.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for T stock:

1. Revenue Growth: 1.9%

AT&T’s growth story centers on replacing legacy services in decline with expanding fiber and wireless offerings.

Fiber Expansion: The company reached 10 million premium fiber subscribers in Q3, more than doubling its base in under 5 years. Fiber revenues grew 16.8% year-over-year. The path to 60 million locations by 2030 creates a multi-year runway for subscriber growth.

Convergence Economics: Over 41% of fiber households also subscribe to AT&T wireless, up 180 basis points from last year. These converged customers exhibit the lowest churn and highest lifetime values. CFO Pascal Desroches noted that while convergence initially pressures ARPU through bundling discounts, it drives higher total service revenues.

Fixed Wireless Acceleration: AT&T added 270,000 Internet Air subscribers in Q3, double the year-ago pace. More than half of Internet Air customers also choose AT&T for wireless. The EchoStar spectrum deployment will significantly expand addressable markets in 2026.

Business Wireline Stabilization: Advanced connectivity services (fiber and fixed wireless) grew 6% year-over-year in Q3, accelerating from 3.5% in Q2. This growth offsets legacy service declines, which management expects will be moderate.

2. Operating margins: 21.5%

AT&T is delivering margin expansion while investing in growth.

Current Performance: Adjusted EBITDA grew 2.4% with margins expanding 30 basis points to reach new highs. Consumer Wireline margins jumped 350 basis points on fiber revenue growth and legacy copper cost reductions.

Cost Structure Improvements: As copper infrastructure comes offline, AT&T eliminates maintenance expenses and power costs. The wireless network modernization, substantially complete by end-2027, will drive further efficiency gains.

Acquisition Benefits: The Lumen deal adds high-quality fiber assets at attractive economics. EchoStar spectrum defers capacity-related capital while enabling wholesale revenue growth as Boost customers migrate to AT&T’s network.

3. Exit P/E Multiple: 9.3x

The market currently values AT&T at 10.9x earnings. We assume the multiple compresses to 9.3x through our forecast period.

Reflects Transition Phase: AT&T’s P/E has averaged 12.5x over the past year and 10.0x over 10 years. The lower multiple acknowledges ongoing headwinds from legacy service declines and competitive wireless markets.

Undervalues Long-Term Potential: As fiber penetration deepens and convergence rates climb, AT&T should command a higher multiple. The company expects to generate nearly $16 billion in annual free cash flow, maintains strong market positions, and is investing strategically in future growth platforms.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Established telcos face technology transitions and competitive pressure. Here’s how AT&T stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth slows to 2.0% and margins compress to 12.3%, the stock still offers a 1.4% annual return.

- Mid Case: With 2.2% growth and 12.9% margins, we expect an annual return of 6.0%.

- High Case: If convergence accelerates and AT&T maintains 13.2% margins while growing at 2.4%, returns could hit 9.7% annually.

See what analysts think about T stock right now (Free with TIKR) >>>

The range reflects execution on fiber expansion, success in migrating copper customers, and competitive dynamics in wireless.

In the low case, cable competitors slow fiber penetration, or wireless pricing pressure intensifies.

In the high case, the Lumen integration succeeds ahead of schedule, Internet Air scales faster with new spectrum, and converged customer growth accelerates meaningfully.

How Much Upside Does AT&T Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!