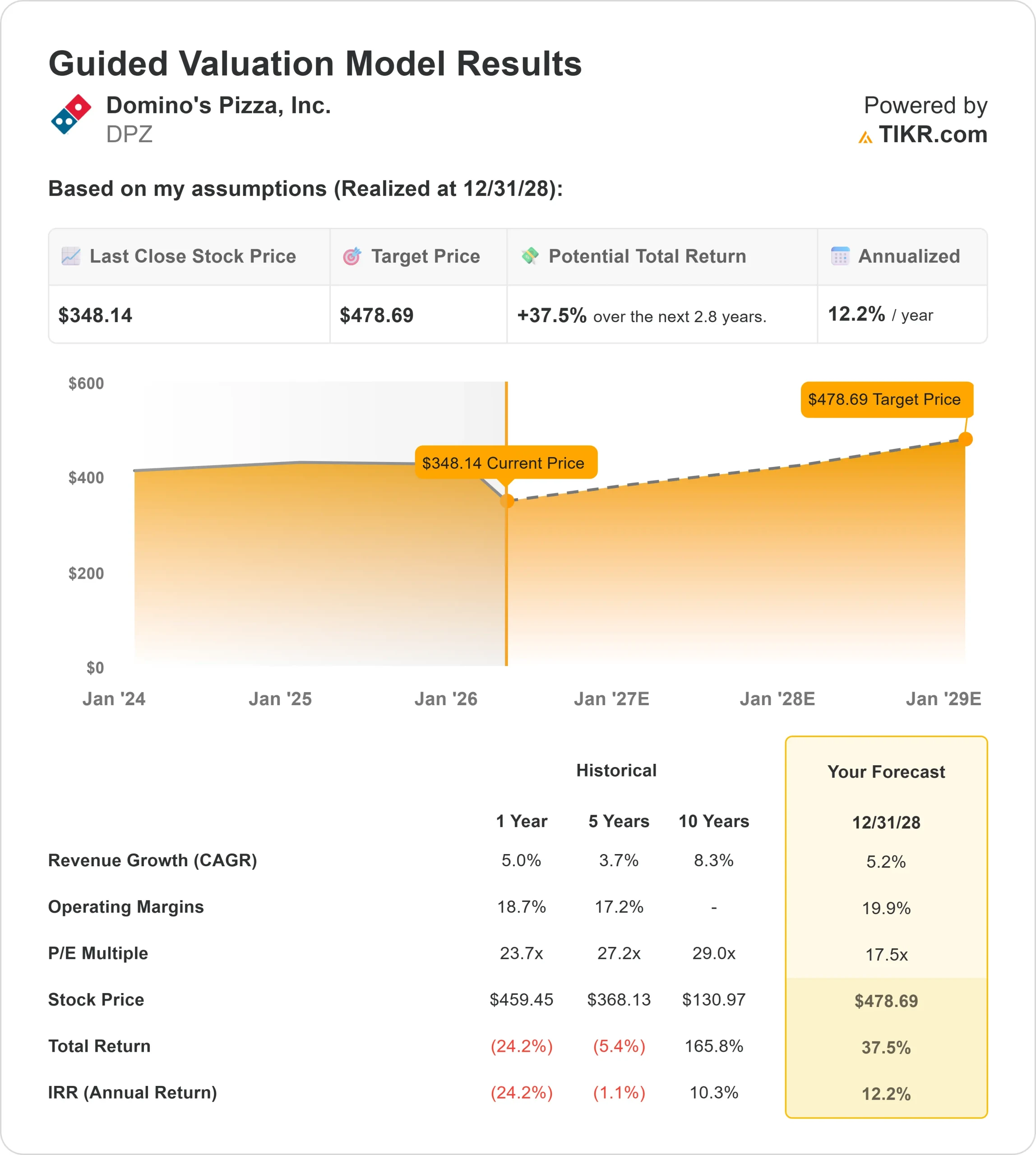

Key Stats for DPZ Stock

- This-Week Performance: -7%

- 52-Week Range: $346 to $499

- Valuation Model Target Price: $479

- Implied Upside: 37%

Analyze your favorite stocks like Domino’s Pizza with TIKR (It’s free) >>>

What Happened?

Domino’s Pizza, Inc. is facing growing pressure in 2026 as investors question whether value-driven traffic can translate into consistent profitability, and the company has become part of that debate alongside peers like McDonald’s and Yum Brands, which have leaned more aggressively into pricing and promotions to sustain traffic, while Domino’s relies more on delivery efficiency and loyalty programs to drive repeat orders.

Domino’s Pizza, Inc. stock fell about 7% this week, finishing near $348 per share, primarily because of notable insider selling and cautious investor positioning ahead of earnings, which raised concerns about near-term confidence in the company’s outlook.

CFO Sandeep Reddy sold about $315,000 in shares, alongside additional sales of about $379,000 from other senior executives including Chief Accounting Officer Jessica Parrish and Chief Supply Chain Officer Cynthia Headen, with the timing of these transactions amplifying concerns around demand trends and margin performance.

Analyst and institutional activity reinforced the mixed outlook. JPMorgan reduced its stake by 39.1% to about 153,394 shares worth about $66 million, while separately upgrading the stock to “overweight” and lowering its price target to $450, signaling longer-term confidence but near-term caution.

Hudson Bay Capital Management cut its position by 95.3%, while other firms showed more constructive positioning, including Berkshire Hathaway increasing its stake by 13.2% to about 2.98 million shares valued at about $1.29 billion, Marshfield Associates raising its stake by 4.0%, Lido Advisors increasing its position by 8.0%, and Brevan Howard boosting its stake by 69%, highlighting a split in investor conviction.

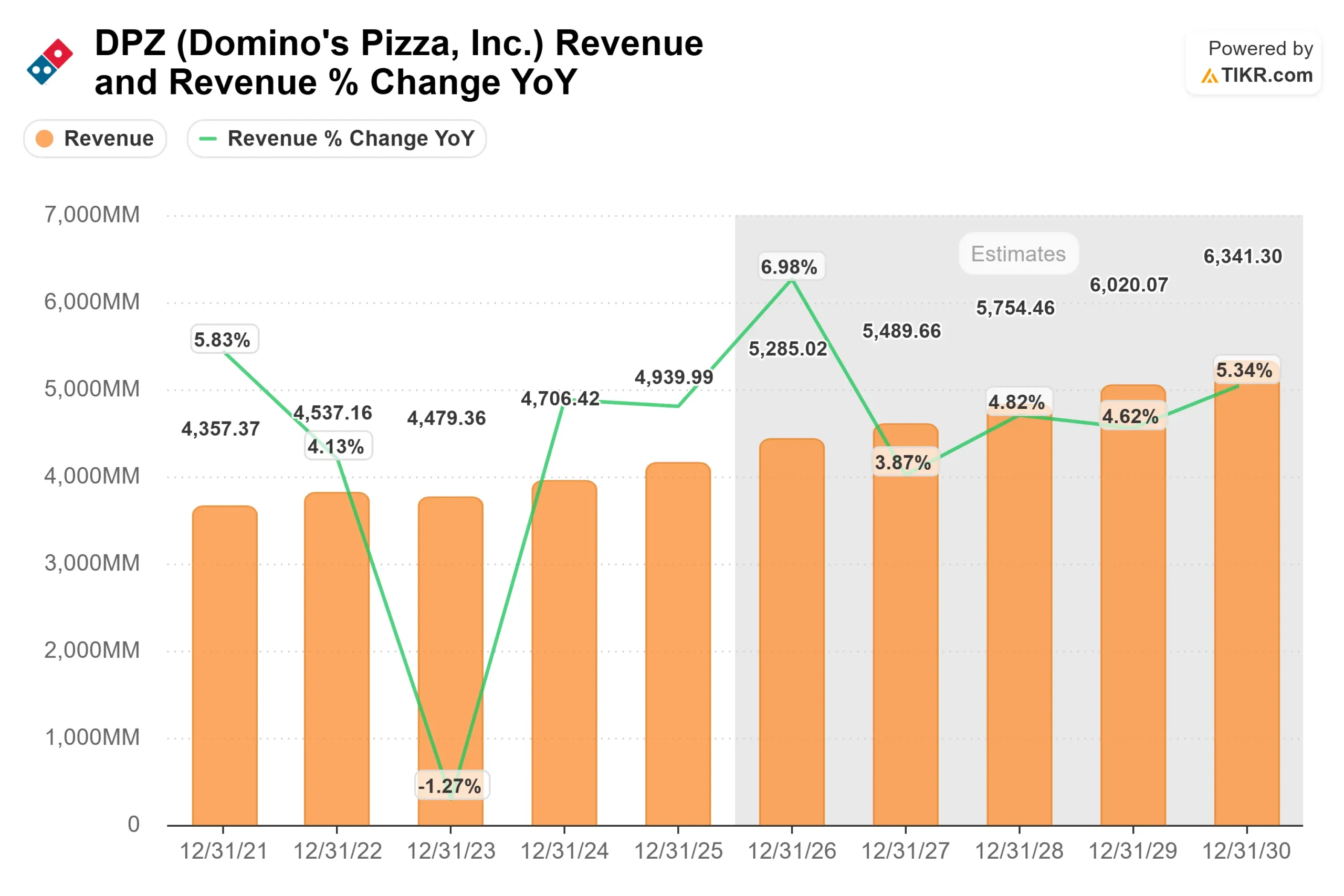

Recent company updates provided a more stable underlying picture, with Domino’s reporting 2025 revenue of about $4.94 billion and global retail sales growth of 5% excluding currency impacts, while adding 776 net new stores to reach 22,142 locations globally.

Management noted the business remains focused on driving “sales, store growth, market share and profitability,” while the key issue is whether traffic driven by promotions can translate into sustained margin expansion, which continues to shape sentiment around the stock this week.

Value Domino’s Pizza instantly (Free with TIKR) >>>

Is DPZ Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 5.2%

- Operating Margins: 19.9%

- Exit P/E Multiple: 17.5x

Revenue growth is expected to remain in the mid-single-digit range, supported by steady global store expansion and continued strength in digital ordering, which allows Domino’s to drive higher order frequency without relying heavily on price increases.

See analysts’ growth forecasts and price targets for Domino’s Pizza (It’s free) >>>

The company’s digital platform and loyalty ecosystem are central to this strategy, helping drive repeat orders and improve customer retention, while delivery scale allows Domino’s to operate more efficiently than smaller competitors.

Margin performance depends on balancing promotional activity with cost control, as higher discounting can support traffic but pressure profitability if supply chain and labor costs are not managed effectively.

Compared to McDonald’s and Yum Brands, which rely more heavily on pricing and menu innovation, Domino’s growth is more dependent on delivery efficiency, franchisee economics, and consistent store-level execution.

Additional upside could come from international expansion and third-party delivery partnerships, which extend reach and support order volume, though they may carry lower margins and require disciplined execution to protect profitability.

At current levels, Domino’s appears undervalued, with future performance driven by margin stability, franchise profitability, and steady global expansion, with the key question being whether the company can convert stable demand into consistent earnings growth over the next 12 months.

How Much Upside Does DPZ Stock Have From Here?

Investors can estimate Domino’s Pizza’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Domino’s Pizza in under 60 seconds with TIKR (It’s free) >>>