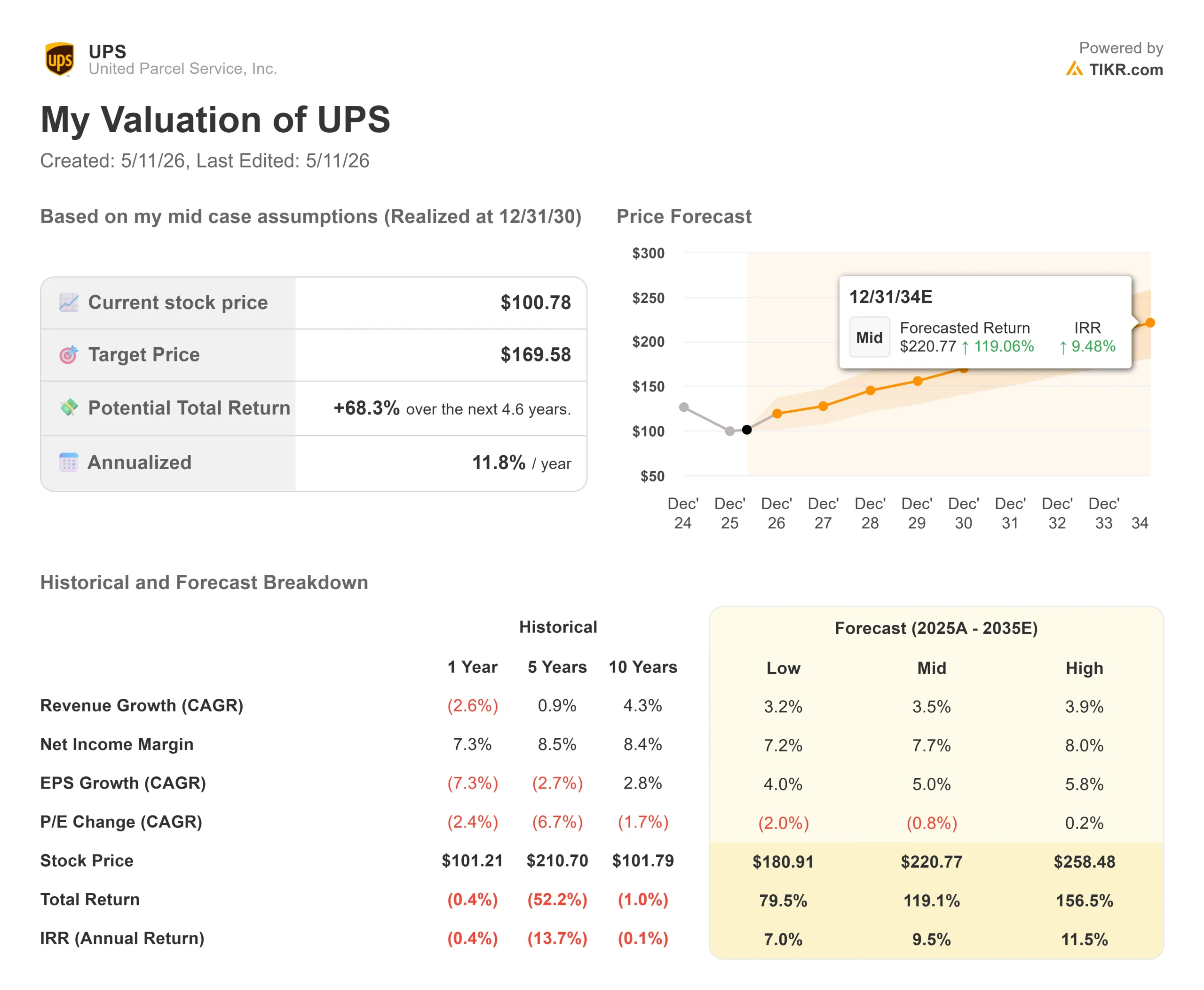

Key Stats for United Parcel Service Stock

- Current Price: $100.78

- Target Price (Mid): ~$170

- Street Target: ~$113

- Potential Total Return: ~68%

- Annualized IRR: ~12% / year

- Earnings Reaction: +2.57% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Parcel Service (UPS) stock has spent three years being defined by what it’s walking away from. With the Amazon glide-down set to complete by June 2026, the market is finally confronting a different question: what does United Parcel Service look like when the transformation noise stops? Bulls argue the company has already built the infrastructure for a structurally more profitable business record, SMB penetration, a historic healthcare quarter, and $3 billion in cost savings on track for the year. Bears point to four years of actual EPS erosion and a margin recovery that still needs to be delivered in the back half. The unresolved question is whether the H2 2026 inflection that CEO Carol Tomé has repeatedly promised is real, or whether it gets pushed out again.

UPS is rebuilding around three growth engines: small and medium-sized businesses (SMBs), business-to-business logistics, and healthcare that carry structurally higher revenue per piece than the high-volume, low-yield e-commerce traffic being shed. The Q1 2026 earnings call gave investors the clearest read yet on whether those engines are already working.

See historical and forward estimates for United Parcel Service stock (It’s free!) >>>

The Amazon Exit Is Almost Done. Here’s What It Unlocked

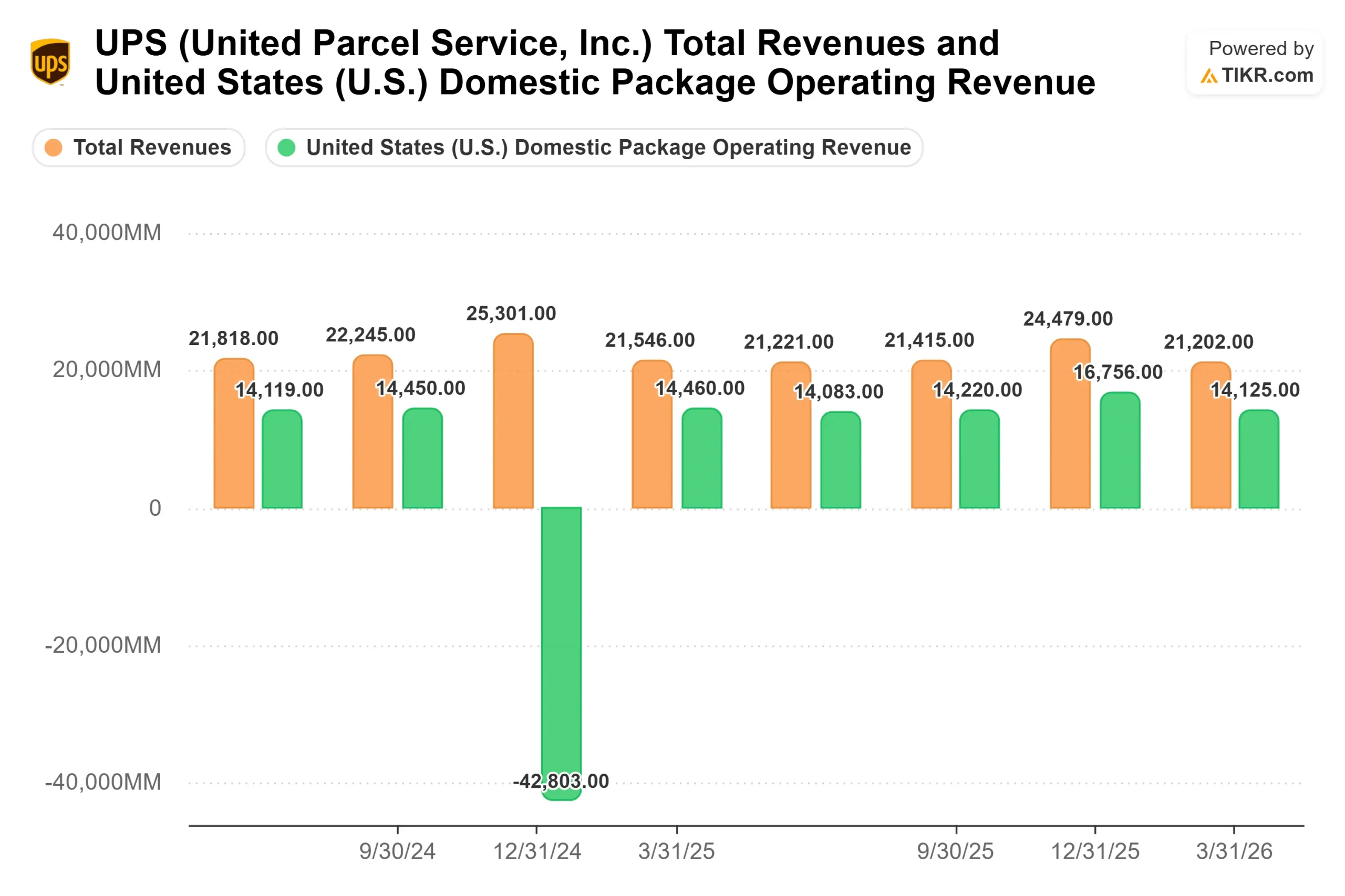

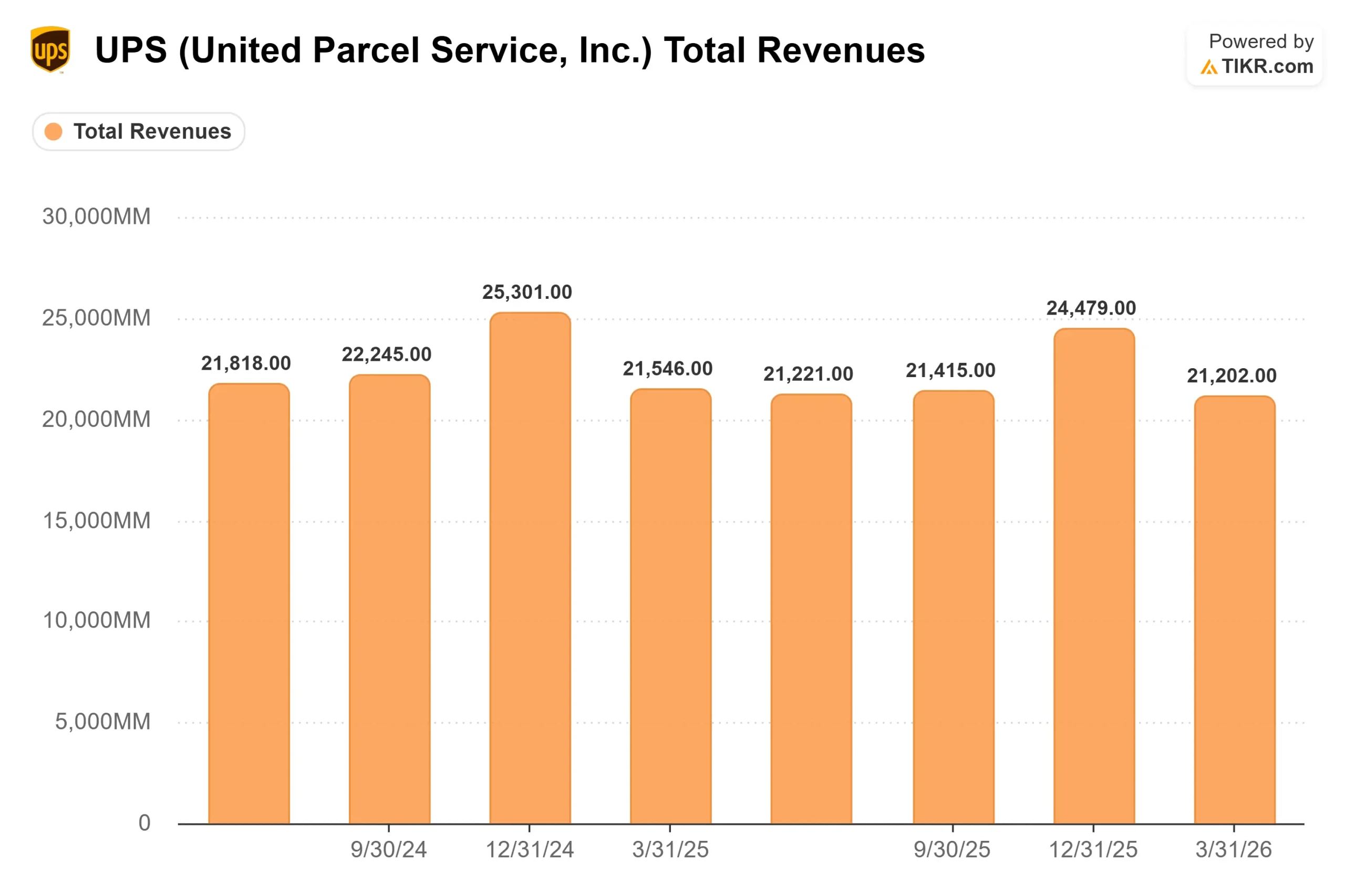

The most important operational fact from Q1 is how far along the Amazon exit already is. UPS reduced Amazon average daily volume by another 500,000 pieces per day during the quarter, bringing Amazon’s share of total revenue to 8.8%, down from above 13% not long ago. CEO Carol Tomé confirmed on the Q1 2026 earnings call that with roughly two months to go, the company is “comfortably in the home stretch” of the most extensive U.S. network reconfiguration in its history.

Freed capacity went straight toward higher-value customers. SMB average daily volume grew 1.6% year-over-year, and SMB penetration hit 34.5% of total U.S. volume, the highest in company history, per CFO Brian Dykes. B2B volume represented 45.2% of total U.S. volume, a 140-basis-point improvement year-over-year and the highest Q1 B2B penetration in six years. That mix shift is showing up in pricing: revenue per piece grew 6.5%, with 200 of those basis points coming purely from customer and product mix improvements, structural gains that don’t depend on fuel surcharges or one-time pricing.

The remaining Amazon relationship is more valuable than the volume decline suggests. Tomé noted that 19% of all e-commerce sales are returned, and UPS leads the market in boxless, labelless returns. “That relationship with Amazon is just going to continue to grow,” she said pointing to reverse logistics and specialized services rather than the commodity volume being wound down.

The $3 Billion Healthcare Quarter the Market Hasn’t Priced In

UPS posted $3 billion in global healthcare revenue in Q1 2026, its first $3 billion healthcare quarter ever, with all three business segments growing year-over-year in the category. Healthcare logistics carries double-digit operating margins across every segment, making it the highest-quality revenue stream in the company. UPS has grown its global healthcare market share every year since 2021, a five-year streak in a sector that is expanding structurally.

The forward-looking piece is GLP-1 drugs, the weight-loss and diabetes medications increasingly shipped direct-to-consumer rather than through traditional pharmacy distributors. Tomé was direct on the call: “With just the changes that we’re seeing in pharmaceutical companies with GLP-1 drugs and how they’re going direct to consumer rather than through distributors, that’s such an opportunity for us and proud to say that we lead the market in that area.” Direct-to-consumer drug delivery requires cold-chain capability and precise, time-definite service. That is exactly what UPS has been building.

UPS recently expanded its Incheon Airport hub in South Korea and opened its largest logistics center in Taiwan, extending the Asia-Pacific footprint in the manufacturing, high-tech, and healthcare corridors that matter most to premium volume growth.

What Q2 Has to Deliver

The near-term test is straightforward: U.S. Domestic operating margin needs to recover from 4% in Q1 to the guided 7.5%–8.5% range in Q2. The $350 million in one-time costs that weighed on Q1 temporary aircraft leases during the MD-11 fleet retirement, Ground Saver USPS transition expenses, weather, and casualty costs are largely behind the company. The USPS Ground Saver transition is complete. New 767 deliveries are continuing. And 77% of the 7,500 Driver Choice positions exited in April, flowing directly into Q2 cost savings.

The network is also running at a 20-year productivity high. With 67.5% of buildings automated and those facilities running 28% lower cost-per-piece than non-automated ones, the efficiency infrastructure is already in place. The question is whether it shows up in the margin line once the transition noise clears.

FedEx, UPS’s closest peer, raised its 2026 profit and revenue forecasts after its own recent results, a signal that underlying parcel demand isn’t deteriorating. On the TIKR Competitors page, FedEx trades at 10.77x NTM EV/EBITDA versus UPS at 8.49x. That discount reflects the transformation risk, but it also means a successful back half could drive multiple expansion on top of earnings growth.

UPS carries a 6.5% dividend yield at current prices, backed by approximately $5.5 billion in expected 2026 free cash flow and $5.4 billion in planned dividend payments, both figures stated by CFO Brian Dykes on the earnings call. The income floor is meaningful while investors wait for the margin recovery.

On the tariff front, UPS processed 16 million IEEPA-related entries and remitted over $5 billion to the U.S. Treasury since last year. With tariff refunds now available through U.S. Customs and Border Protection, UPS has applied and will pass every dollar back to customers. As Tomé put it: “As soon as we get that money, we’re going to remit it right back to our customer.” There is no P&L benefit to UPS, but it reinforces customer trust at a critical moment in the relationship.

See how United Parcel Service performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $100.78

- Target Price (Mid): ~$170

- Potential Total Return: ~68%

- Annualized IRR: ~12% / year

See analysts’ growth forecasts and price targets for United Parcel Service stock (It’s free!) >>>

The TIKR mid-case target of ~$170, realized at 12/31/30, uses a revenue CAGR of 3.5% and a net income margin of 7.7%. Both sit below UPS’s own 10-year historical performance, 4.3% revenue CAGR, and 8.4% net income margin, which means the model doesn’t require UPS to outperform its own history. It just requires the company not to underperform.

The two revenue growth drivers are healthcare logistics growing above-market with GLP-1 direct-to-consumer as a building tailwind and SMB/B2B mix improvement, where higher revenue per piece accretes as Amazon-era volume is replaced. The margin driver is the automated network. The primary risk is execution timing: if the H2 2026 recovery slips into 2027, the EPS trough extends and dividend coverage optics weaken. The free cash flow profile and 6.5% yield provide a meaningful income floor while that plays out.

Conclusion

Watch the U.S. Domestic operating margin on July 28, when UPS reports Q2 2026 results. Management guided 7.5%–8.5%. Anything below 7.5% signals transformation costs aren’t clearing on schedule, putting the full-year 9.6% operating margin target at risk. Above 8% confirms the inflection has arrived and makes the 2027 setup materially cleaner.

UPS at $100.78 is priced for a company still mid-transition. The Q1 data record SMB penetration, a $3 billion healthcare quarter, and 6.5% revenue per piece growth suggest the new business mix is already working. The transformation isn’t finished. The case for owning it before the market recognizes that it may be building.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in United Parcel Service?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up United Parcel Service, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Parcel Service alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze United Parcel Service on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!