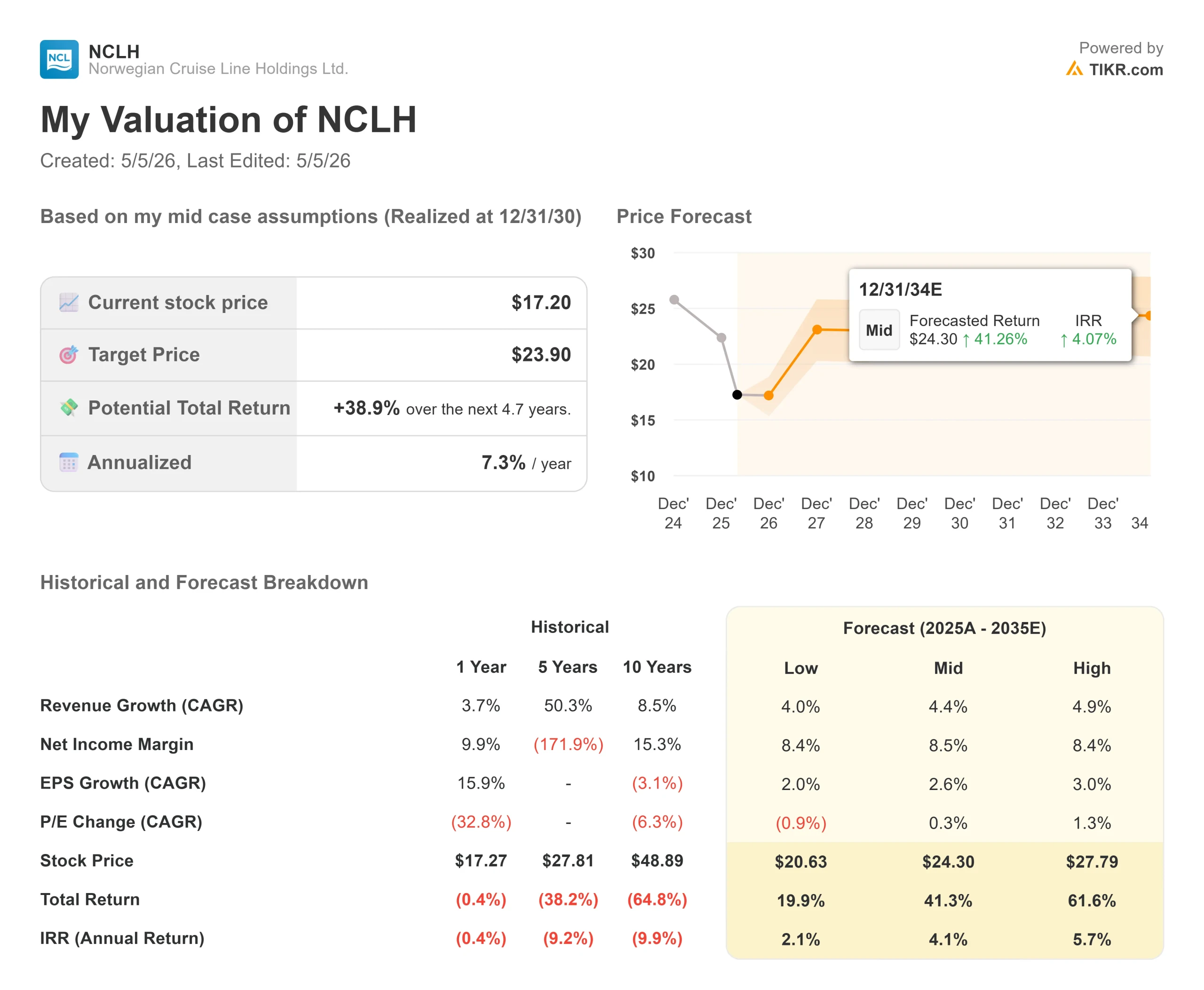

Key Stats for Norwegian Cruise Line Stock

- Current Price: $17.22

- Target Price (Mid): ~$24

- Street Target: ~$24

- Potential Total Return: ~39%

- Annualized IRR: ~7% / year

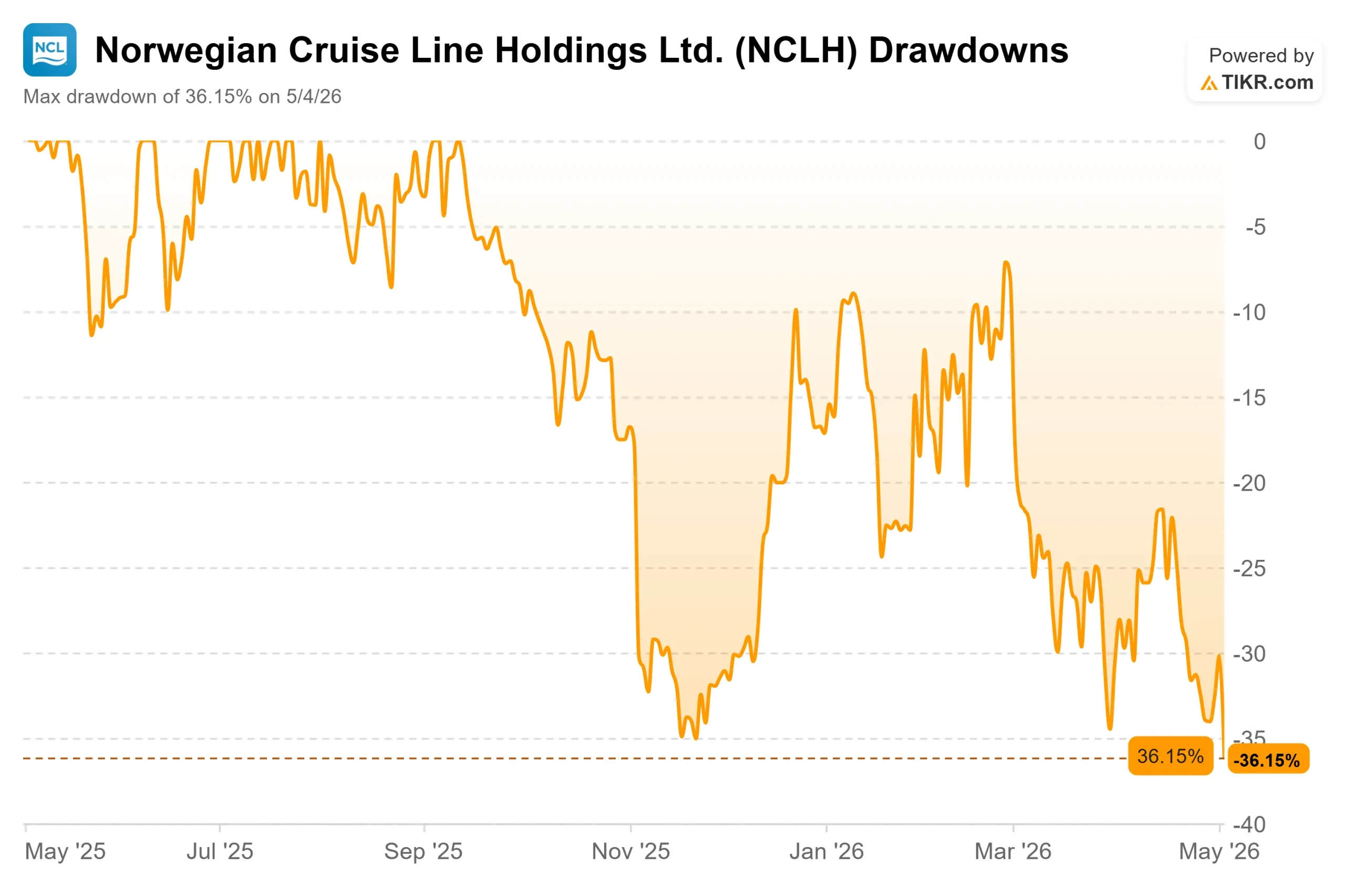

- Earnings Reaction: -8% (May 4, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Norwegian Cruise Line Holdings (NCLH) has fallen about 36% from its recent high, and Monday’s 8% single-day drop after Q1 2026 earnings brought shares close to their 52-week low of $16.78. The market’s read is straightforward: guidance was slashed, the yield outlook turned negative, and a new CEO is still working through problems that have been building for years. Bulls counter that the selloff punishes a company whose core issues are self-inflicted and fixable, whose luxury brands are performing well, and whose costs are improving faster than the Street expected. The question is whether the Norwegian brand can be rebuilt quickly enough to justify buying at current prices.

The answer depends less on the macro than most investors think.

What Happened and Why the Market Sold

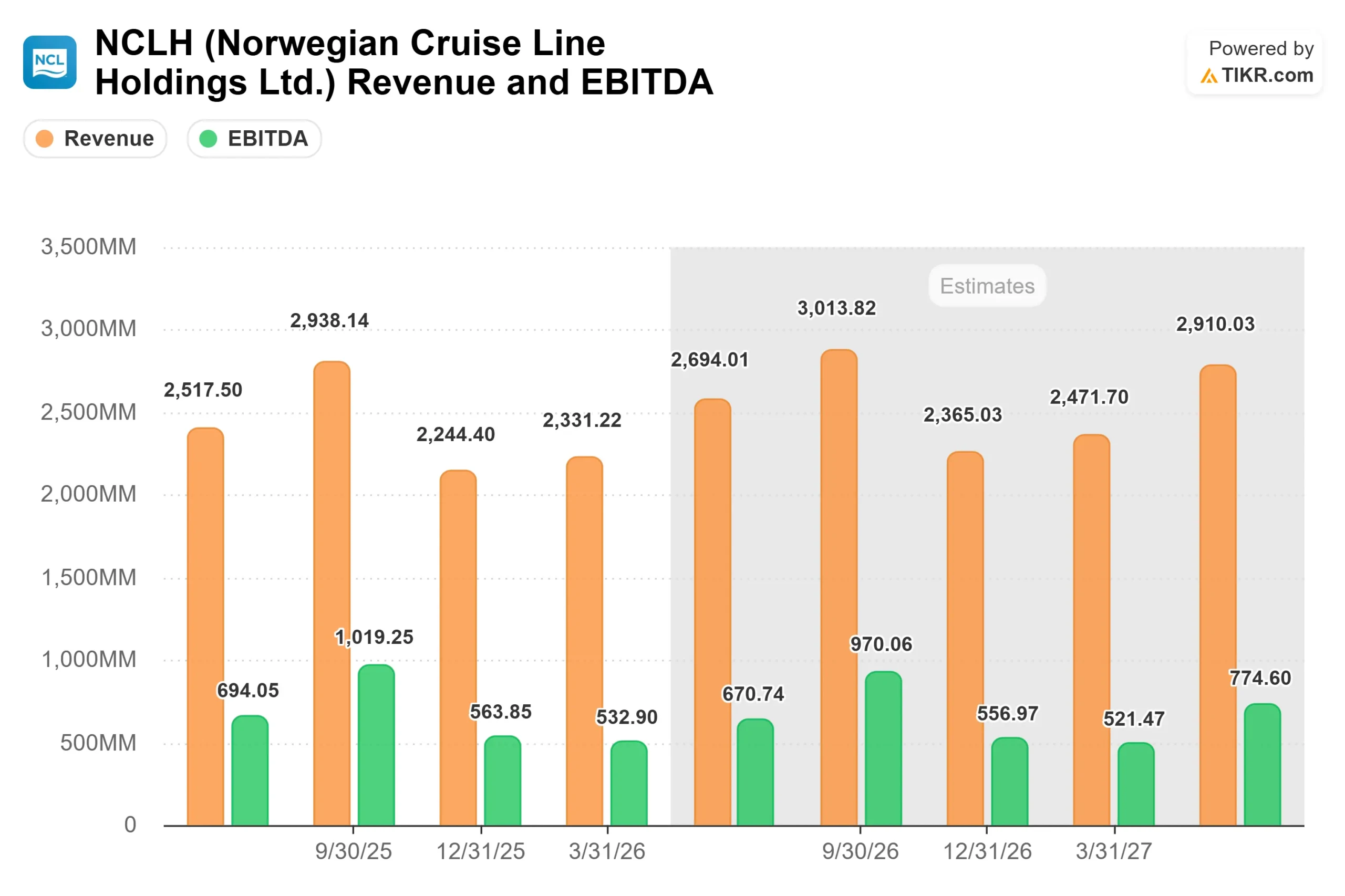

On May 4, 2026, NCLH reported Q1 2026 adjusted EPS of $0.23, beating the analyst consensus of $0.14 by 61.25%, per TIKR’s Beats and Misses data. Adjusted EBITDA of $532.90 million came in 6.24% above estimates. Revenue of $2.33 billion grew 9.6% year over year, though it missed consensus by about 1.2%. The market sold anyway because of what came after it.

Management cut full-year 2026 adjusted EPS guidance from $2.38 to a range of $1.45 to $1.79, a reduction of about 30% at the midpoint. Full-year adjusted EBITDA guidance was cut to between $2.48 billion and $2.64 billion. Net yield (revenue per available passenger cruise day, the cruise industry’s key operating metric) is now expected to decline 3% to 5% for the full year.

Two forces are driving that reset. The first is external. Ongoing conflict in the Middle East pushed full-year fuel expense to approximately $800 million, elevated crew airfare and logistics costs, and hit European bookings hard. NCLH has outsized exposure here: roughly 26% of its capacity is deployed in Europe during Q2, rising to 38% in Q3. Because NCLH sources a larger share of its European passengers from the United States than its peers do, American hesitation about overseas travel hits Norwegian harder than it hits Royal Caribbean or Carnival.

The second force is internal. CFO Mark Kempa, Executive Vice President and Chief Financial Officer, noted on the call that NCLH entered 2026 already behind its ideal booking curve, which meant the external headwinds compounded problems that were already there. CEO John Chidsey, Chairperson and Chief Executive Officer, put it directly: “We are not comparable to our peers at the moment. I said this is a turnaround. That’s why the change was made. That’s why I’m sitting here now.”

The market heard “turnaround” and sold.

See historical and forward estimates for Norwegian Cruise Line stock (It’s free!) >>>

What the Selloff Misses

The market is treating two very different problems as one. The external yield shock from the Middle East conflict is real but unlikely to be permanent. The internal execution gap is serious but fixable.

The Norwegian brand drifted from its core customer (premium families with children and seasoned cruisers) over several years. Marketing spend grew dramatically relative to competitors without matching returns. On the call, Kempa said NCLH had been spending probably twice as much as peers on a per-bed basis. The bundled air program had become more of a subsidy than a demand driver. The company also transitioned to a new revenue management system whose calibration was still incomplete and whose team was still being built out.

None of these are structural flaws. They are execution failures that a disciplined team can fix.

As Chidsey said on the call, “I don’t look at it as you have to repair damage. I look at it as we just got to get back to maximizing what we can get out of that brand.”

What the Cost Numbers Already Show

Before dismissing the turnaround as a promise, look at what management has already delivered. NCLH announced $125 million in annualized run-rate SG&A savings through organizational streamlining and marketing efficiency improvements. Salary and benefits costs are expected to decrease approximately 15% on an annualized basis. In 2026, those savings contribute approximately a 2 percentage point reduction in adjusted net cruise cost, excluding fuel.

The company has achieved sub-inflationary unit cost growth for three consecutive years, with cumulative savings approaching $400 million, already exceeding its three-year $300 million target.

The capital picture strengthens into 2027 and beyond. Per TIKR’s estimates, capital expenditure falls from approximately $3.21 billion in 2026 to around $2.04 billion by 2028 as ship deliveries slow from two per year to one. Free cash flow is projected to turn substantially positive as a result: from negative $427 million in 2027 to positive $605 million in 2028 and positive $1.97 billion in 2029, per TIKR estimates. NCLH also carries no significant debt maturities until 2030, giving management room to focus on the recovery without near-term refinancing pressure.

The Revenue Recovery and Why 2027 Is the Real Test

The cost improvements will come faster than the revenue improvements. Chidsey said so explicitly. Rebuilding a revenue management team, reorienting marketing toward the right customer, and re-establishing credibility with travel agents takes quarters, not months.

Q3 2026 will be the hardest stretch. Kempa said on the call that Q3 could see high-single-digit negative yields, because European exposure peaks at 38% of deployment and the company is still chasing bookings that should have been secured months earlier. The Great Tides Waterpark at Great Stirrup Cay is scheduled to open by the end of Q3, which management expects to support Caribbean demand heading into Q4.

The luxury brands (Regent Seven Seas and Oceania) are performing to expectations throughout all of this, with Chidsey noting encouraging signs from both in the weeks ahead of the call. Onboard spending across the fleet also remains healthy. The problem is at the top of the marketing funnel, not after guests board. That is a more solvable problem than lost product quality.

For 2027, the cost savings carry forward as structural tailwinds. Kempa reaffirmed on the call that nothing is structurally preventing NCLH from returning to its approximately 39% EBITDA margin target. “I don’t think there’s anything structural in front of us that would preclude us from getting back to 39-plus percent,” he said. The 2027 guidance update, expected with Q3 2026 results, will be the first real signal of whether the revenue rebuild is on track.

See how Norwegian Cruise Line performs against its peers in TIKR (It’s free!) >>>

How NCLH Stacks Up Against Peers

NCLH currently trades at an NTM EV/EBITDA of 8.84x, per TIKR’s Competitors page. That sits just above Carnival Corporation at 8.50x but well below Royal Caribbean at 11.80x. Royal Caribbean has earned its premium through stronger pricing discipline and more consistent commercial execution. The gap is real and currently justified, but it also shows the re-rating potential if NCLH can demonstrate that the Norwegian brand’s execution issues are truly behind it.

TIKR Advanced Model Analysis

- Current Price: $17.22

- Target Price (Mid): ~$24

- Potential Total Return: ~39%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for Norwegian Cruise Line stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of around 4.4% and a net profit margin of approximately 8.5% through 12/31/30, reflecting a conservative return to normalized demand growth as the Norwegian brand rebuilds. The primary risk is a yield recovery that takes longer than expected: if the marketing and revenue management rebuild extends meaningfully into 2028, the earnings timeline shifts out, and the IRR compresses.

On the upside, if the Norwegian brand regains pricing traction in 2027 as the new commercial team gels, EBITDA would inflect sharply given the mostly fixed cost base and the CapEx tailwind. The TIKR model’s high case puts the stock at around $28 by 12/31/30. On the downside, if macroeconomic conditions worsen and leverage limits flexibility, the stock could stay range-bound near current levels, with the low case at around $21.

At $17.22, NCLH is priced as though the low case is the base case. The TIKR model says that is too pessimistic.

Conclusion

Watch Q3 2026 net yield. If the number lands closer to negative 7% than negative 10%, it signals the trough was less severe than feared, and the Q4 Caribbean recovery narrative is intact. NCLH is a turnaround story where the cost side is already delivering, the revenue side requires patience, and the assets, brands, and margin structure needed for a re-rating all exist.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Norwegian Cruise Line?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Norwegian Cruise Line, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Norwegian Cruise Line alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Norwegian Cruise Line on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!