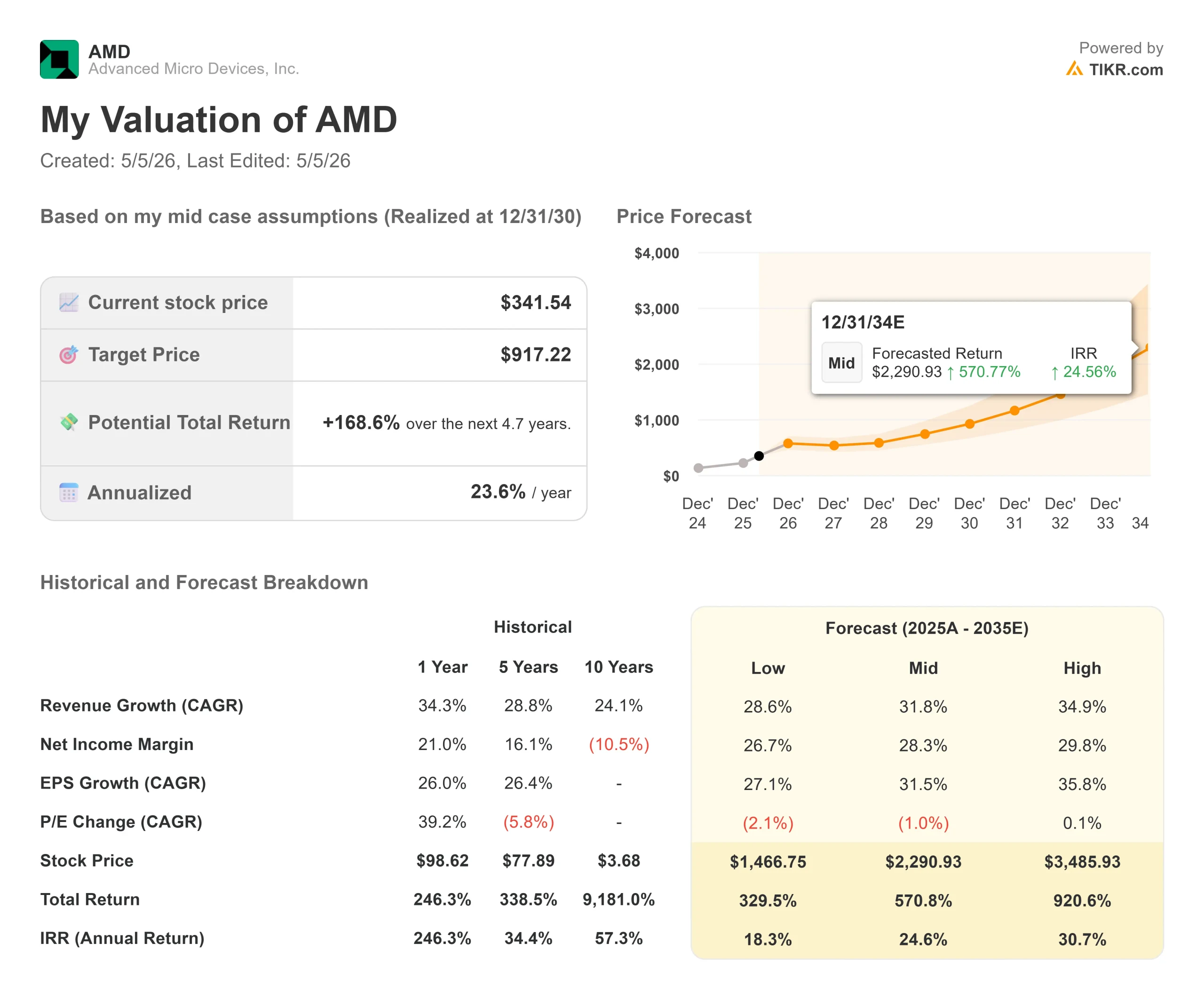

Key Stats for AMD Stock

- Current Price: $341.54

- Target Price (Mid): ~$917

- Street Target (Mean): ~$310

- Potential Total Return (Mid): ~169%

- Annualized IRR: ~24% / year

- Q4 2025 Earnings Reaction: -17.31% (February 3, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The semiconductor market just posted one of its most extraordinary months in recent memory, and Advanced Micro Devices (AMD) led it. According to S&P Global Market Intelligence, AMD rocketed 74.3% in April, compared to a 14.4% gain for NVIDIA over the same period. Tonight’s Q1 2026 report, due after the market close with the call beginning at 5:00 PM ET, is the first real stress test of whether that move was rational or simply momentum running ahead of execution.

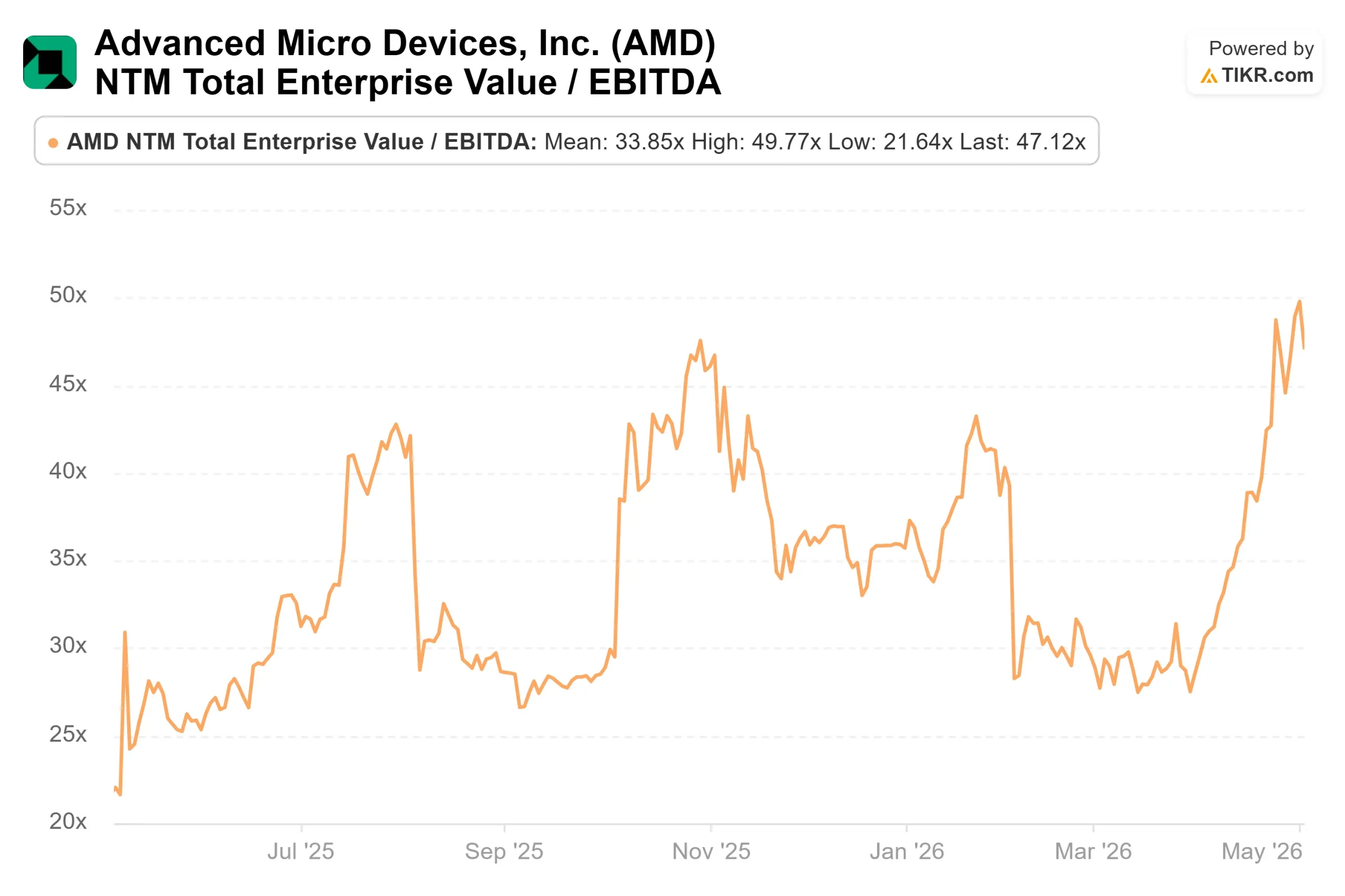

Bulls argue the rally reflects the market repricing AMD as a contracted AI infrastructure supplier. The structural catalyst is the February 24 partnership with Meta: AMD and Meta announced a 6-gigawatt agreement to power Meta’s next generation of AI infrastructure, with shipments supporting the first gigawatt deployment scheduled to begin in the second half of 2026. Bears counter that AMD now trades at 47.12x NTMEV/EBITDA per TIKR, the MI450 rack-scale GPU has not yet generated a dollar of revenue, and a 74% surge in a single month raises the bar for anything short of a flawless quarter.

The single unresolved question tonight: does the Q1 print give investors enough evidence that the contracted H2 2026 ramp is real?

What Lisa Su Said at Morgan Stanley That the Market Hasn’t Fully Priced In

AMD CEO Dr. Lisa Su’s appearance at the Morgan Stanley Technology, Media & Telecom Conference on March 3, 2026, was one of her most substantive public sessions of the year. Several things she said deserve more attention than they received.

On the Meta deal’s architecture, Su explained the partnership was built differently from standard procurement: “What we wanted to do at this point is we actually see an inflection point in AI infrastructure. There is a much more detailed workload specification.” Rather than selling off-the-shelf chips, AMD designed the MI450 “starting from the workload first,” building it around Meta’s Llama-class model characteristics from the chip level up through the system level. AMD’s CFO Jean Hu noted at the February investor call that this deployment is expected to generate revenue of “significant double-digit billions of dollars per gigawatt.” With six gigawatts committed across multiple product generations, the revenue potential embedded in this relationship is structurally significant relative to AMD’s $34.6 billion full-year 2025 revenue base.

Su was equally direct about the OpenAI partnership, which carries the same 6-gigawatt scale and came first: “Our relationship with OpenAI is better than it has ever been. We are basically co-validating together. We’re planning those installations together.” Two 6-gigawatt contracted relationships, both actively co-validating MI450 systems, both with first shipments targeting H2 2026.

The most underappreciated part of the transcript is Su’s CPU commentary. “Even the hyperscalers are surprised. The demand for CPU computing sitting along AI was perhaps something that was under forecasted.” She noted at AMD’s Financial Analyst Day that she expected a high-teens CAGR for the broader compute market, then upgraded that view at Morgan Stanley: “Every indication that I’m seeing today is that the compute market is even larger than that.” Agentic AI workloads, which spawn large numbers of parallel software agents each requiring CPU orchestration, are pulling server CPU orders forward faster than most analyst models assumed. This adds a second growth engine alongside GPU demand that the market has not fully credited.

See historical and forward estimates for AMD stock (It’s free!) >>>

The Numbers That Matter

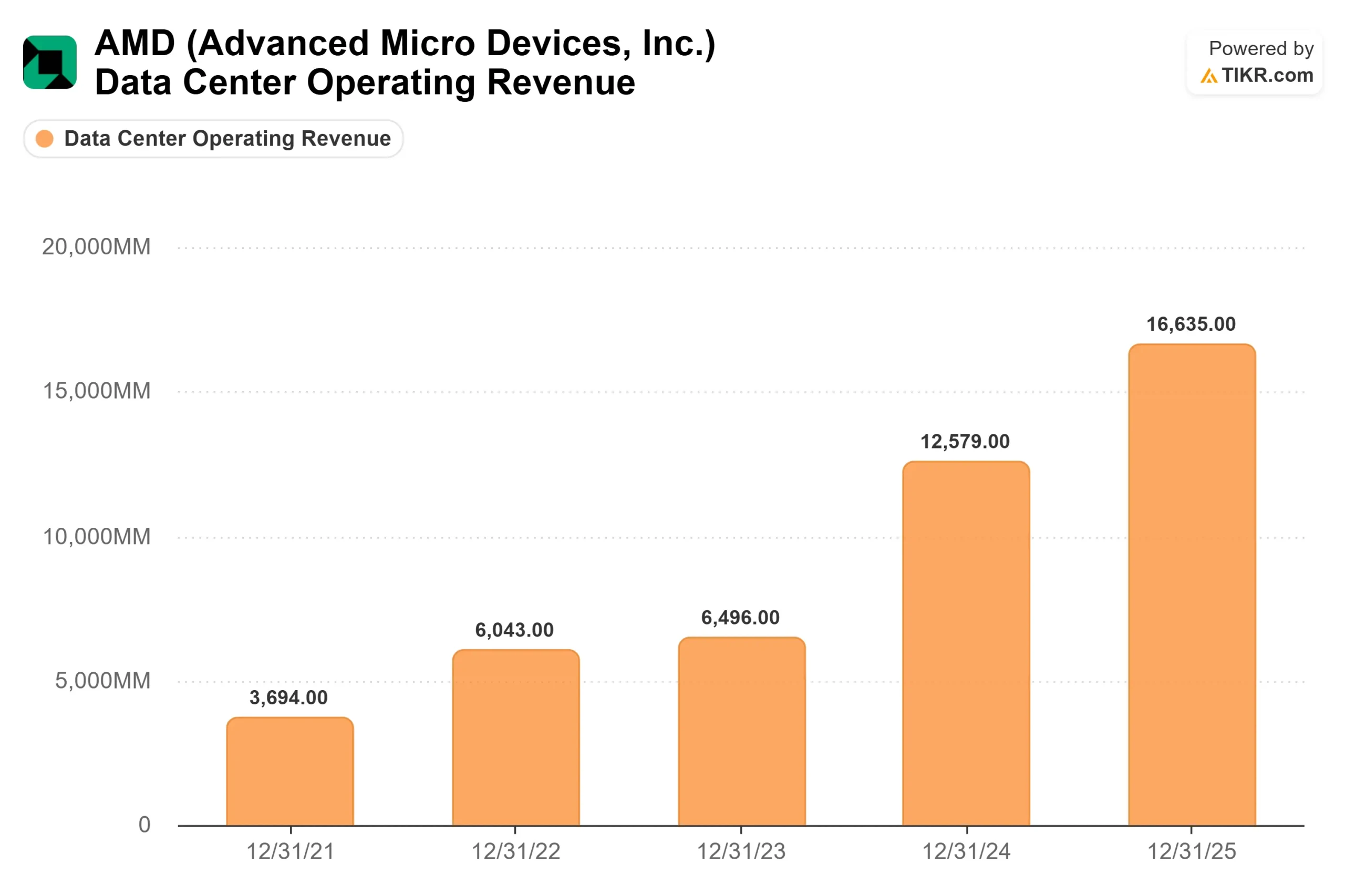

AMD’s fundamentals heading into tonight are genuine. Full-year 2025 revenue reached $34.6 billion, up 34.3% year over year. Data Center generated $16.6 billion of that total, up 32% year over year, and Q4 2025 data center revenue hit a record $5.4 billion, up 39% year over year, per AMD’s official results. AMD has beaten adjusted EPS consensus in each of the last four quarters, with Q4 2025 being the most decisive: actual adjusted EPS of $1.53 came in 15.98% above the $1.32 estimate, per TIKR’s Beats & Misses page.

Per AMD’s Q4 2025 earnings call, management guided Q1 2026 revenue to approximately $9.8 billion (±$300 million), reflecting around 32% year-over-year growth, including approximately $100 million in MI308 GPU sales to China. According to Zacks consensus, data center revenue for Q1 is estimated at $5.56 billion, up 51.5% year over year. That is the number Wall Street is watching tonight. A clean beat there, alongside Q2 guidance showing continued sequential data center growth, largely validates the H2 ramp thesis.

On valuation, TIKR’s Competitors page shows AMD at 47.12x NTM EV/EBITDA against NVIDIA at 18.99x and Broadcom at 24.56x. The premium reflects the market pricing in the Meta and OpenAI ramps before they appear in the income statement. HSBC downgraded AMD to Hold while raising its price target slightly to $340, citing stretched valuation and TSMC capacity dependence. D.A. Davidson upgraded to Buy with a $375 target, pointing to the Meta deal and agentic AI driving CPU demand well above prior estimates. The spread between those two calls captures exactly what investors are debating tonight.

The China risk is real but bounded. AMD guided approximately $100 million in MI308 GPU sales for Q1, with no additional China revenue in the forward outlook, while license applications for the MI325 series remain under review. Su was direct at Morgan Stanley: “It is still a little bit complicated.” An approval would be unmodeled upside. Further restrictions would remove even the $100 million floor.

See how AMD performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $341.54

- Target Price (Mid): ~$917

- Potential Total Return: ~169%

- Annualized IRR: ~24% / year

See analysts’ growth forecasts and price targets for AMD stock (It’s free!) >>>

The TIKR mid-case model targets approximately $917 per share by 12/31/30, implying around 169% total return and roughly 24% annualized from today’s $341.54 entry. The model uses a ~32% revenue CAGR and projects net income margins expanding from 19.7% in 2025 to around 28% by 2030, per TIKR.

Two revenue CAGR drivers underpin the mid-case. The first is Data Center AI GPU revenue scaling as the MI450 Helios cycle ramps across Meta, OpenAI, and other hyperscalers in H2 2026 and into 2027. The second is EPYC server CPU share gains as the Venice architecture on TSMC’s 2nm process targets its own H2 2026 launch, capturing the agentic AI CPU demand Su described at Morgan Stanley. The margin driver is operating leverage from mix shift toward higher-margin data center products.

The primary risk Su acknowledged at Morgan Stanley is worth repeating directly: “These are very complex systems. I will be clear with that.” The H2 2026 MI450 Helios rack-scale ramp is the single most binary event in the AMD thesis through 2027. A smooth ramp converts the Meta and OpenAI commitments from press releases into revenue that feeds the TIKR model. A stumble delays the entire free cash flow curve and would compress the 47x NTM EV/EBITDA multiple that currently prices in perfect execution.

Conclusion

Watch the Data Center segment revenue when AMD reports tonight. According to Zacks consensus, the estimate is $5.56 billion, up 51.5% year over year and a modest step above Q4 2025’s $5.4 billion record. A beat at that level alongside a strong Q2 guide confirms the ramp is real. A miss below $5.2 billion likely reverses a material portion of April’s gains. AMD now holds contracted positions as the second-source GPU supplier for the world’s two largest foundational model builders. If tonight’s numbers hold, the 74% April run may prove to be the beginning, not the end.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in AMD?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMD, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMD alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!