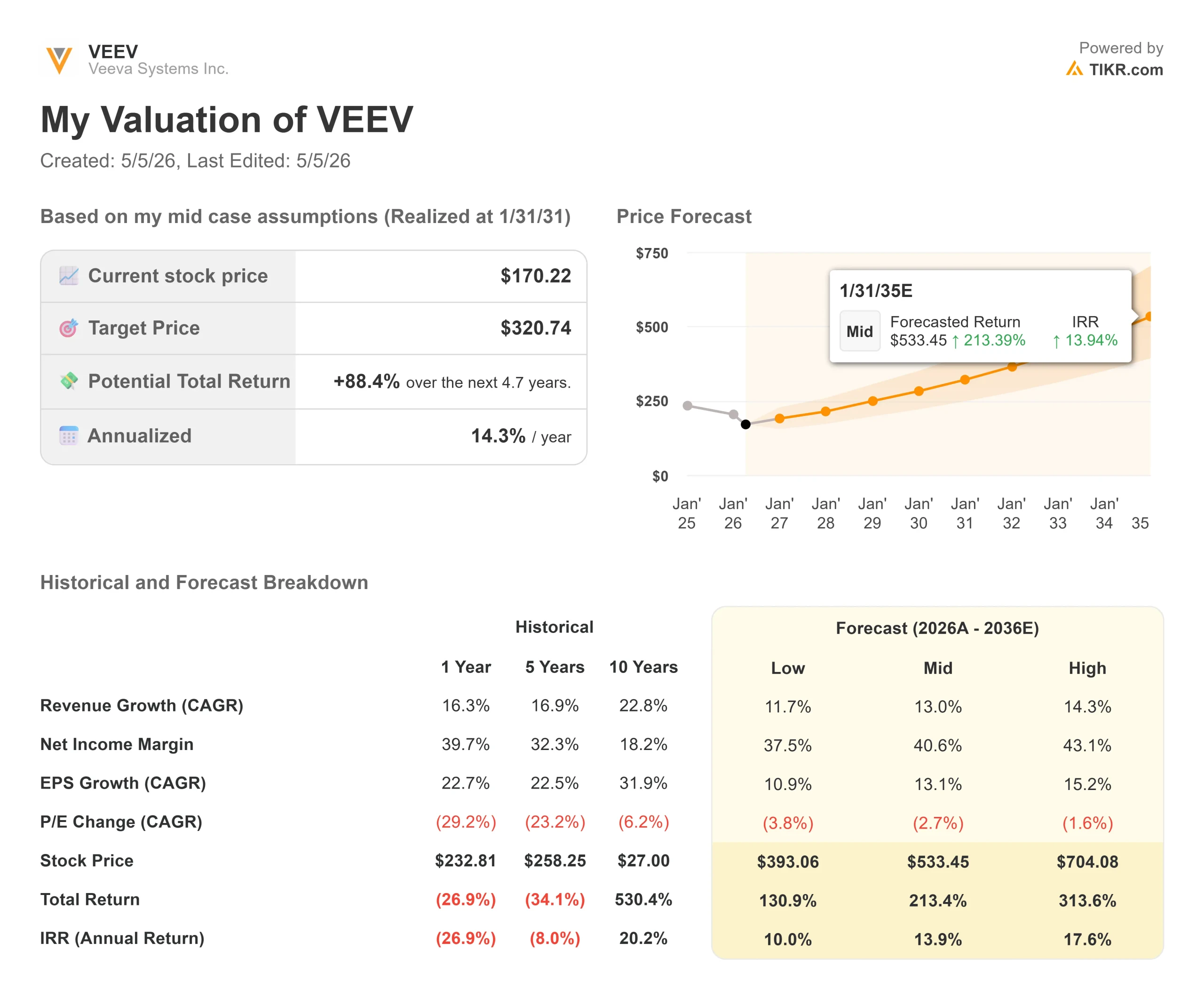

Key Stats for Veeva Stock

- Current Price: $168.92

- Target Price (Mid): ~$321

- Street Target: ~$264

- Potential Total Return: ~88%

- Annualized IRR: ~14% / year

- Earnings Reaction: +4.02% (March 4, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

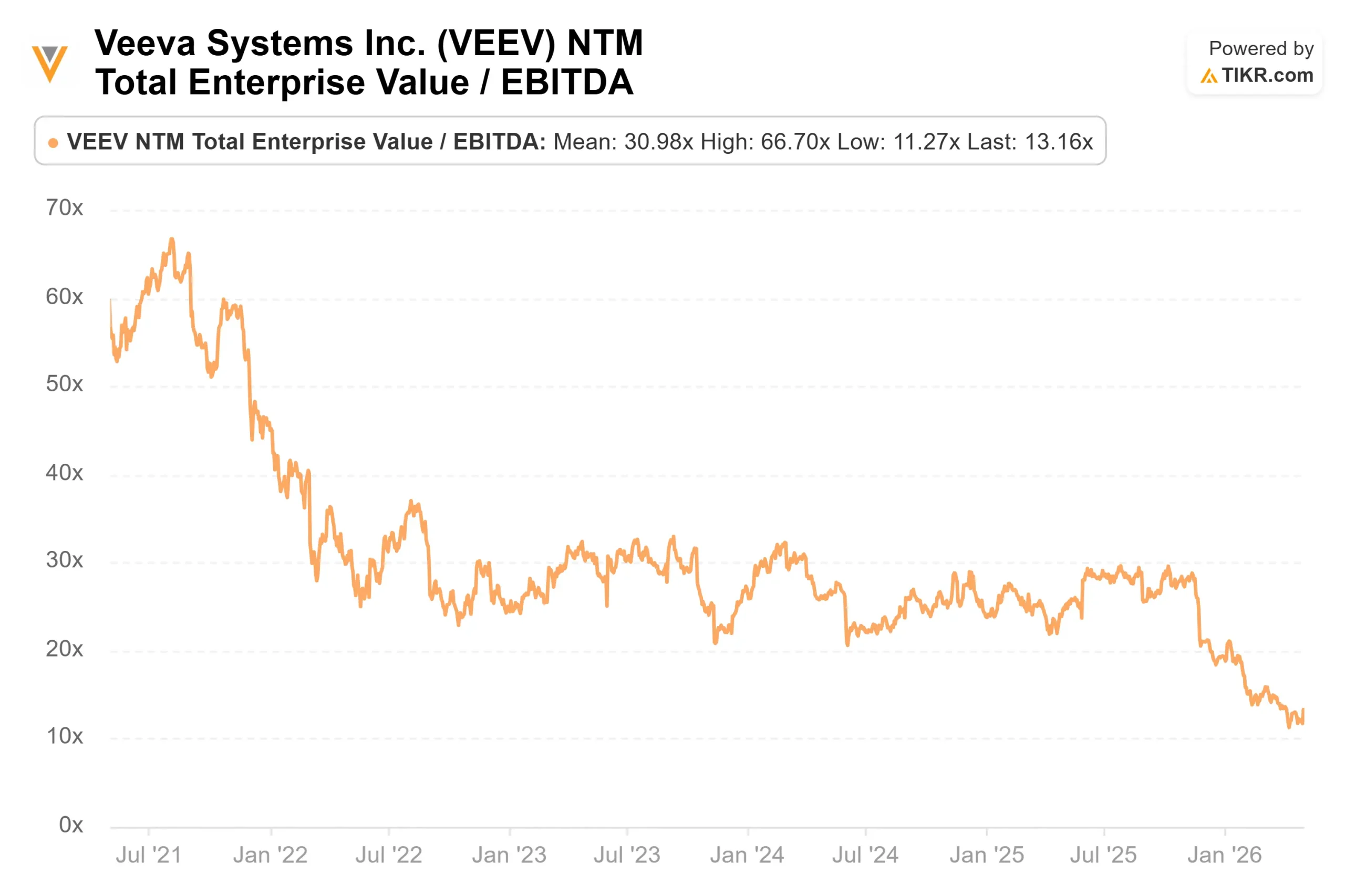

Veeva Systems (VEEV) stock has lost nearly half its value from a 52-week high of $310.50, and the debate is as sharp as the drop. Bears point to Salesforce’s dedicated Life Sciences Cloud, a Vault CRM top-20 commitment count that came in below earlier expectations, and a forward growth rate they say no longer warrants a premium multiple. Bulls counter that the NTM EV/EBITDA has compressed from roughly 25x at the start of fiscal 2026 to 13x today, pricing in far more damage than five consecutive quarters of revenue beats would suggest. Then on April 30, Veeva’s S&P 500 inclusion, effective May 7, triggered a 10% single-session surge from the mid-$150s. The stock sits at $168.92. The question is whether those bounce marks are a real floor or a brief reprieve.

The Drop and What the Market Missed

The max drawdown reached 50.55% on April 10, 2026. Three things drove it. On the Q3 FY2026 call in November 2025, CEO Peter Gassner revised the expected Vault CRM top-20 pharma commitment to roughly 14 of 20, down from the prior expectation of closer to 18. Analysts cut targets sharply in response. Then a broad software sector de-rating compressed the multiples further.

What the market underweighted was execution. By the Q4 call on March 4, EVP of Strategy Paul Shawah confirmed close to 140 customers live on Vault CRM, including two top-20 pharmaceutical companies fully deployed across the U.S., Europe, and Japan. Shawah also noted that win rates outside the top 20 are expected to be higher than within it, because smaller companies want a trusted partner with a working product today. The company also pulled the Veeva CRM end-of-support date forward to December 2029 from September 2030, a signal that migration execution is running ahead of schedule.

On the financial side, Q4 FY2026 revenue came in at $835.95 million against a consensus estimate of $810.95 million. Full-year revenue hit $3,195.31 million, up 16.3% year over year. The stock’s earnings reaction was a modest +4.02% on March 4, still weighed down by the CRM overhang.

See historical and forward estimates for Veeva stock (It’s free!) >>>

The R&D Story That CRM Headlines Are Drowning Out

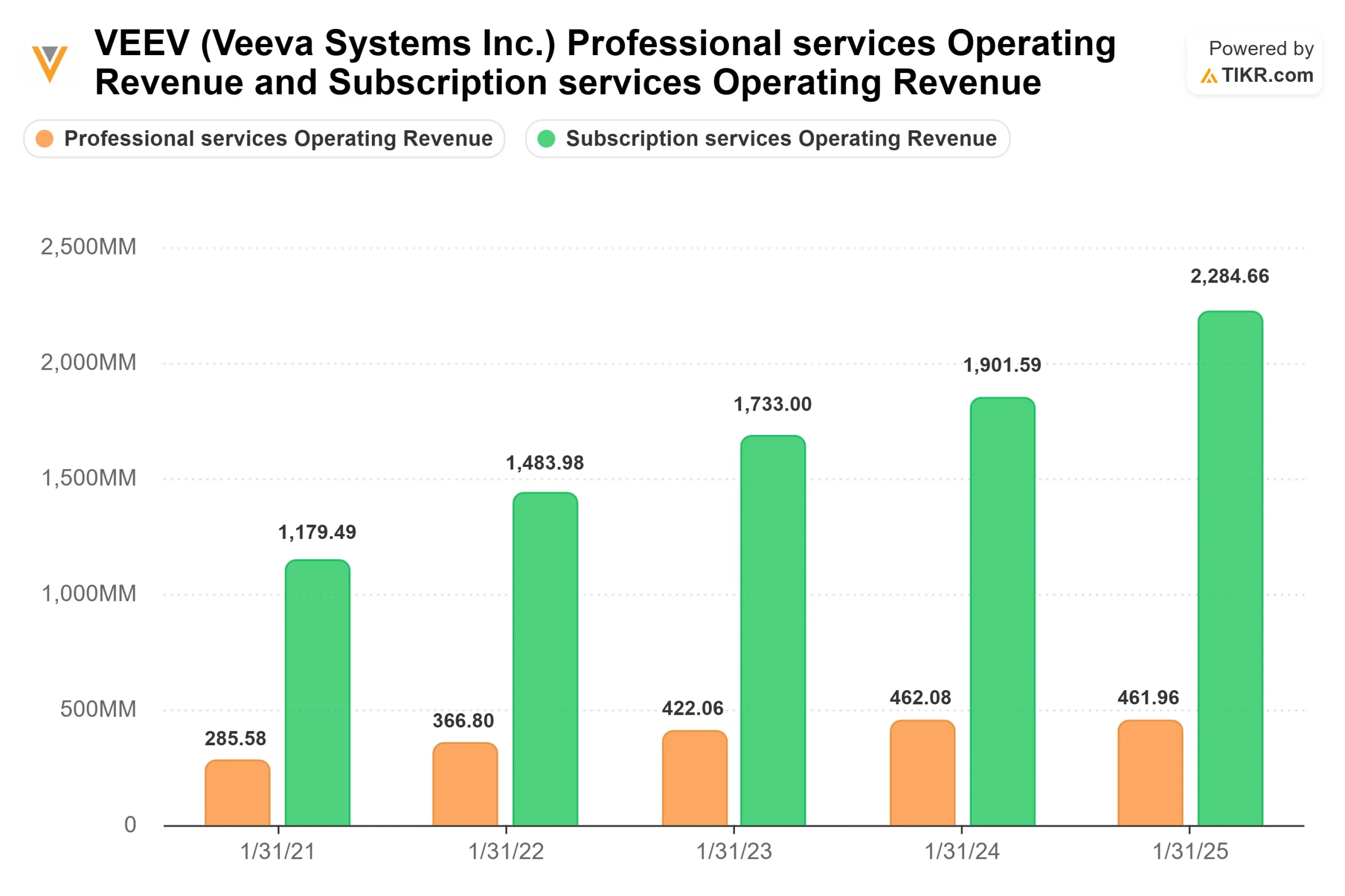

The Q4 call included a milestone that got less attention than it deserved: a top-20 pharmaceutical company standardizing its RTSM (randomization and trial supply management, the software that manages drug shipments and patient assignments at clinical trial sites) at the enterprise level. RTSM has historically been procured study-by-study. An enterprise standardization changes the revenue model entirely. Gassner called it “a milestone deal for Veeva and for the industry.”

The safety segment is accelerating alongside it. Gassner confirmed another top-20 safety win in Q4 and the first top-20 customer going live on Safety Signal and Workbench, which the company internally calls the “safety surge.” CFO Brian Van Wagener explained that the shift toward RTSM, EDC (electronic data capture, the platform sponsors and CROs use to collect and manage clinical trial data), and safety as primary growth drivers creates a near-term mix effect on reported subscription growth. That explains the FY2027 subscription guidance of around 13%, not a deterioration in underlying demand.

On AI, Gassner was direct. Veeva is an enabling and launch partner for Anthropic’s Claude for Life Sciences, as confirmed during the Q4 call. He positioned Veeva alongside SAP and Workday as core systems of record that AI agents build on rather than replace. The deeper point: a pharmaceutical company that deploys Veeva’s safety AI and later adds clinical data management gets interoperability with the safety module essentially out of the box. Every additional Veeva product raises the switching cost of the entire stack. That compounding stickiness is the economic moat the bear case consistently underweights.

See how Veeva performs against its peers in TIKR (It’s free!) >>>

What the Valuation Actually Shows

Veeva’s NTM EV/EBITDA sits at 13.16x as of May 4, 2026. That compares to roughly 25x at the start of fiscal 2026 and nearly 29x in mid-2025, a compression of close to 47%, against a business that beat revenue estimates five quarters running.

From the TIKR Competitors page, Certara (CERT) trades at 8.09x NTM EV/EBITDA and Simulations Plus (SLP) at 11.72x. Both are niche life sciences software companies with market caps of $949 million and $306 million, respectively, far smaller than Veeva’s $27.8 billion. Veeva’s premium to this peer group, at 13.16x, has narrowed to its tightest level in years, pulling it toward companies that lack Veeva’s scale, margins, and platform breadth.

The 28-analyst price target consensus sits at a mean of $264.46. Across 31 analyst recommendations, the breakdown is 14 Buys, 8 Outperforms, 7 Holds, 1 Sell, and 1 No Opinion. The LTM free cash flow figure from TIKR is $1,048.07 million. A company generating over a billion dollars annually in free cash flow, guiding to $3.585–$3.600 billion in FY2027 revenue, and trading at 13x forward EBITDA is priced for managed decline. The quarterly results and the transcript argue against that reading.

TIKR Advanced Model Analysis

- Current Price: $168.92

- Target Price (Mid): ~$321

- Potential Total Return: ~88%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Veeva stock (It’s free!) >>>

The mid-case model uses a 13% revenue CAGR and a net income margin of around 41%. The two primary revenue drivers are continued R&D Cloud expansion across RTSM, EDC, and safety, and the Crossix healthcare data analytics platform that drove much of FY2026’s outperformance. The margin driver is structural: as Vault CRM migrations eliminate Salesforce royalty payments from Veeva’s cost base, those dollars flow directly to Veeva. Van Wagener confirmed this on the call: “Once everybody is off, then those payments will stop.”

The primary risk is Crossix. It laps a breakout FY2026 year from Q1 FY2027 onward, and a sharp deceleration in commercial subscription growth would pressure the 13% revenue CAGR. The low-case scenario from the TIKR model projects around $393 per share. The high case reaches approximately $704.

Conclusion

Watch subscription revenue growth rate at Q1 FY2027 earnings, expected in early June 2026. Management guided FY2027 subscription growth at approximately 13%. If Q1 holds at or above that level while Crossix laps its tough comparable without a material miss, the structural slowdown narrative breaks, and the case for multiple re-rating strengthens. Veeva is generating over a billion dollars in annual free cash flow, beating guidance for five straight quarters, and entering the S&P 500 with 140 live Vault CRM customers. At 13x NTM EV/EBITDA, the market is pricing it like a business in decline.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Veeva?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Veeva, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Veeva alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!