Key Stats for Bloom Energy Stock

- Past week’s performance: -2.9%

- 52-week range: $139 to $445

- Valuation model target price: $270

- Implied upside: 36.7% over 2.8 years

Value your favorite stocks like Bloom Energy with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Bloom Energy Corporation (BE) stock fell about 5.7% this week, even though the company stayed in the news for reasons that were not clearly negative on their own. Reuters reported on March 27 that Bloom appointed Simon Edwards as CFO, effective April 13, and the company said his background includes leadership roles at Groq, Conga, ServiceMax, and GE.

That kind of hire usually signals operational focus. Still, the stock was already trading with high expectations after its huge run into 2026, so investors appeared to use the update to reset sentiment rather than add risk.

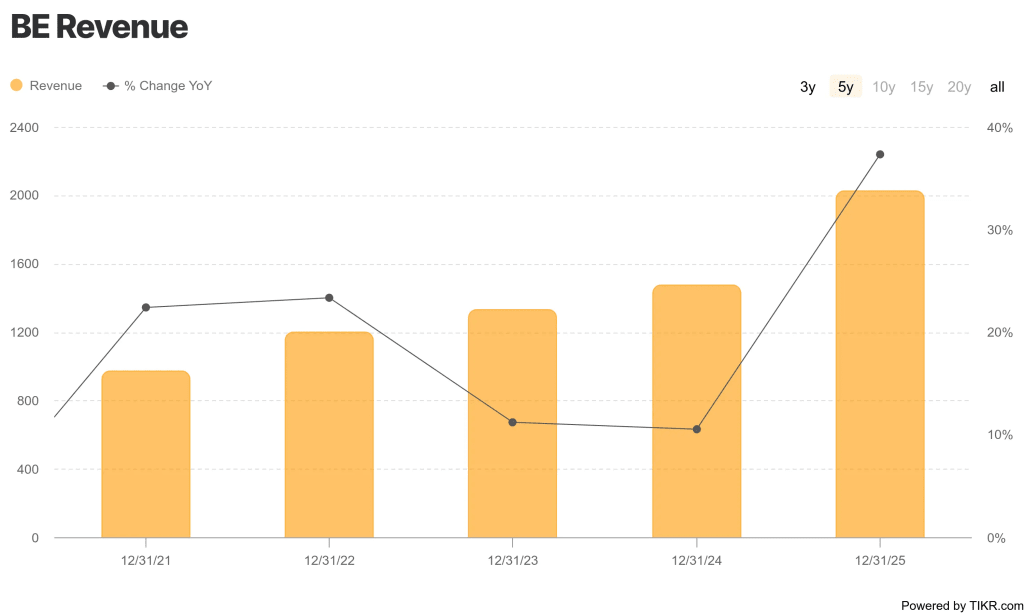

The company also filed its annual materials last week, and Reuters noted that its full-year 2025 revenue increased to $2.02 billion, while the company scheduled the annual meeting for May 21. That filing did not change the main story, but it kept attention on a stock that has become tied to power demand from AI data centers.

That AI power narrative has been central since February. Bloom reported record 2025 revenue, and Reuters said the stock jumped after management forecast 2026 revenue of $3.1 billion to $3.3 billion, above analyst estimates.

Management also said the current backlog was about $20 billion, including roughly $6 billion of product backlog, which helped explain why the stock rerated so sharply earlier this year.

But this week’s pullback also fits a valuation-sensitive setup. Reuters reported Citi initiated coverage with a neutral rating and a $162 target in late February, and Reuters also highlighted several March insider sales, including transactions by Chief Legal Officer Shawn Soderberg.

See analysts’ growth forecasts and price targets for Bloom Energy (It’s free) >>>

Is Bloom Energy Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 37.3%

- Operating Margins: 7%

- Exit P/E Multiple: 95.6x

Based on these inputs, the model estimates a target price of $168.63, implying 26.6% total upside from the current share price and a 8.9% annualized return over the next 2.8 years.

Those assumptions line up with a business that is growing quickly, but they also show why the stock has become harder to underwrite after its surge. Revenue rose 37.3% to $2.02 billion in 2025, while gross profit climbed 48.3% to $600.1 million and gross margin improved to 29.6% from 27.5% a year earlier.

The valuation question is whether that improvement can keep compounding fast enough to justify today’s multiples. Bloom trades at about 18.75x LTM EV/revenue and 11.92x NTM EV/revenue, while the model still assumes a 95.6x exit P/E multiple. That is a demanding setup, especially because the model’s 8.9% annualized return is solid but not especially high for a stock with this level of volatility.

The business does have balance-sheet support behind the growth story. Bloom ended 2025 with about $2.45 billion of cash and cash equivalents, and net debt fell to about $541.7 million even after total debt increased. That matters because the company is selling capital-intensive power systems, so liquidity and financing flexibility help it serve large customers while scaling backlog into revenue.

There is also a meaningful difference between Bloom’s recent operating progress and the market’s long-term expectations. Free cash flow turned positive again at $57.2 million in 2025, marking a second straight year of positive free cash flow, but margins are still relatively thin for the valuation investors now assign to the company.

What’s Driving the Bloom Energy Stock Going Forward?

The next major catalyst is first-quarter results, with Bloom expected to report Q1 2026 results on April 30. Investors will be watching whether demand tied to AI data centers is still converting into orders, deployments, and margins at the pace implied by the company’s 2026 outlook.

Management commentary suggests the demand story is still centered on power availability. At the February earnings release, CEO KR Sridhar said, “Bring-your-own-power has shifted from a slogan to a business necessity for AI hyperscalers and manufacturing facilities,” and he called the shift “secular and growing.”

Bloom reinforced that same message at CERAWeek, where the company said it was meeting demand for reliable 24/7 power as energy security, AI infrastructure, and decarbonization converge.

The broader industry backdrop also matters. In January, Bloom released its 2026 Data Center Power Report, which said hyperscalers and colocation providers expect roughly one-third of data centers in 2030 to use 100% onsite power, up from the previous survey.

That does not guarantee Bloom wins all of that demand, but it does support why investors have treated the company as an AI infrastructure power name rather than just an electrical equipment stock.

Leadership execution and investor communication will matter too. The new CFO officially starts on April 13, and Bloom is also scheduled to present at Becker’s Annual Meeting and the S&P Global Power Markets Conference that same day, before the May 21 shareholder meeting.

So the next move in the stock will likely depend on whether management can show that backlog, AI-driven demand, and better margins are turning into repeatable results rather than just a strong 2025 inflection.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Bloom Energy?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Bloom Energy stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!