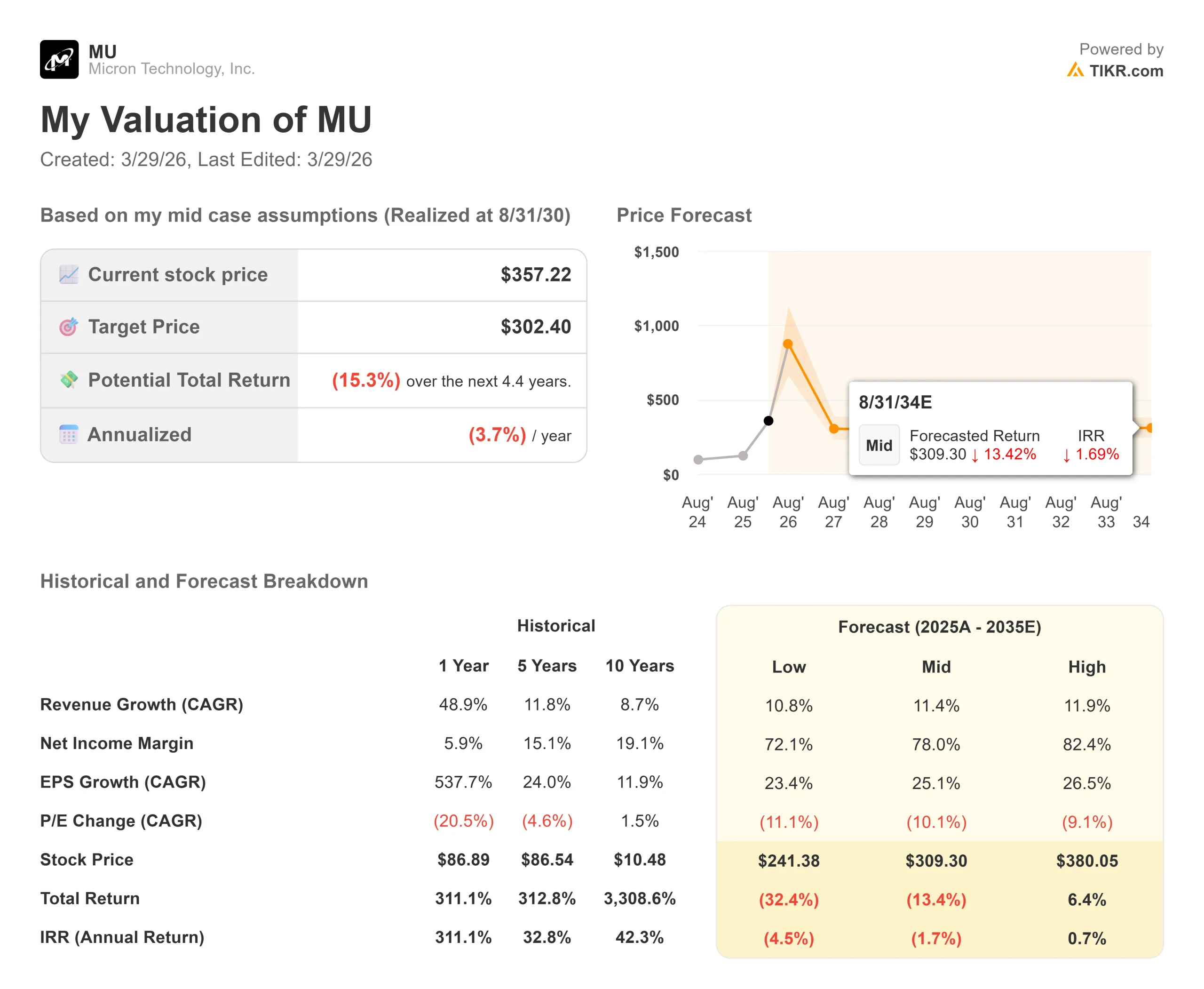

Key Stats for Micron Stock

- Current Price: $357.22

- Target Price (Mid): $302.40

- Street Target (Mean): $527.60

- Potential Total Return (Mid): (15.3%)

- Annualized IRR (Mid): (3.70%) / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

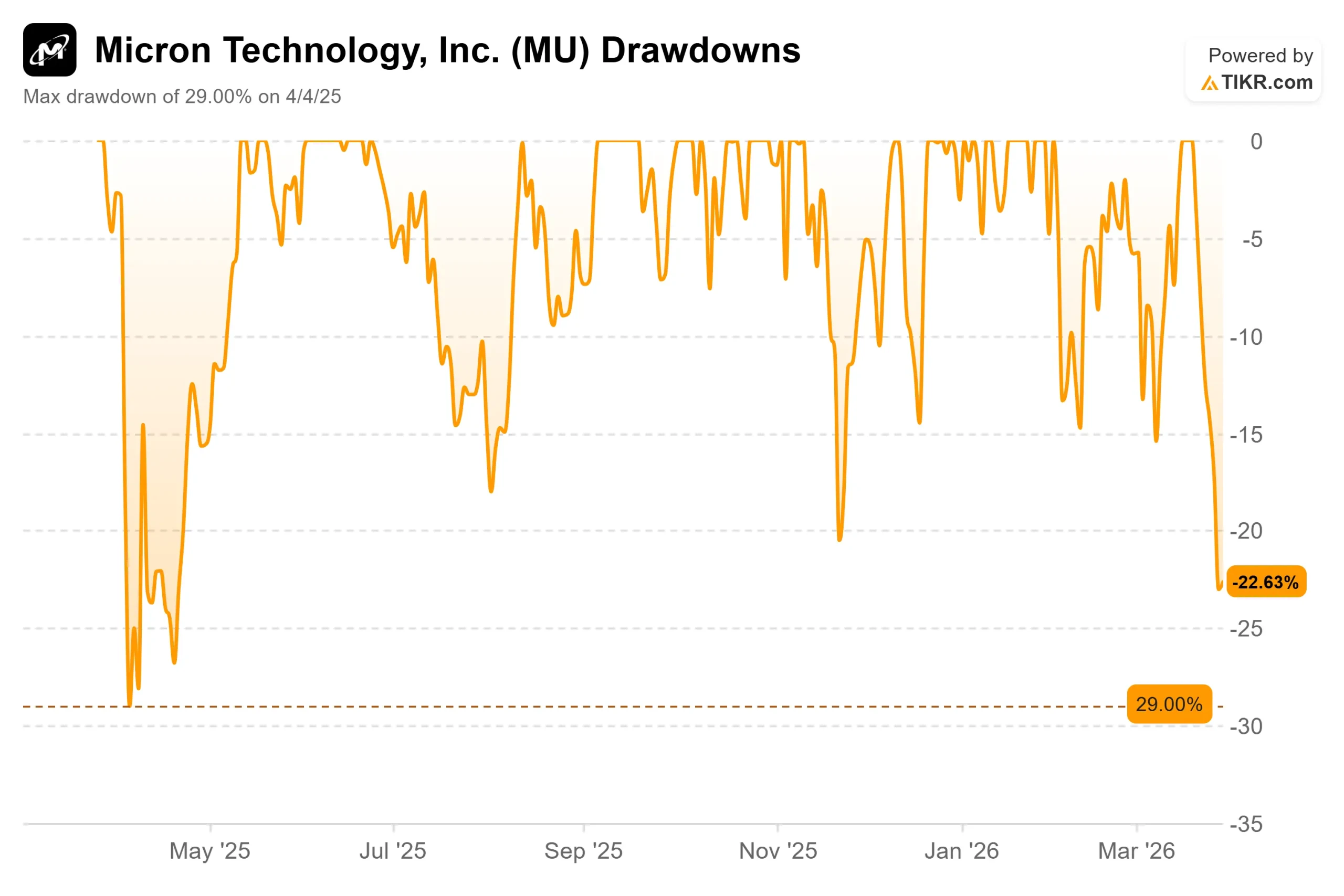

Micron Technology (MU) has done something almost no company manages: post the best quarter in its history and spend the next two weeks falling.

Bulls see a structurally undersupplied AI memory market trading at a fraction of its earnings power. Bears see a $25 billion capital expenditure bet facing a software threat that could rewrite the demand math.

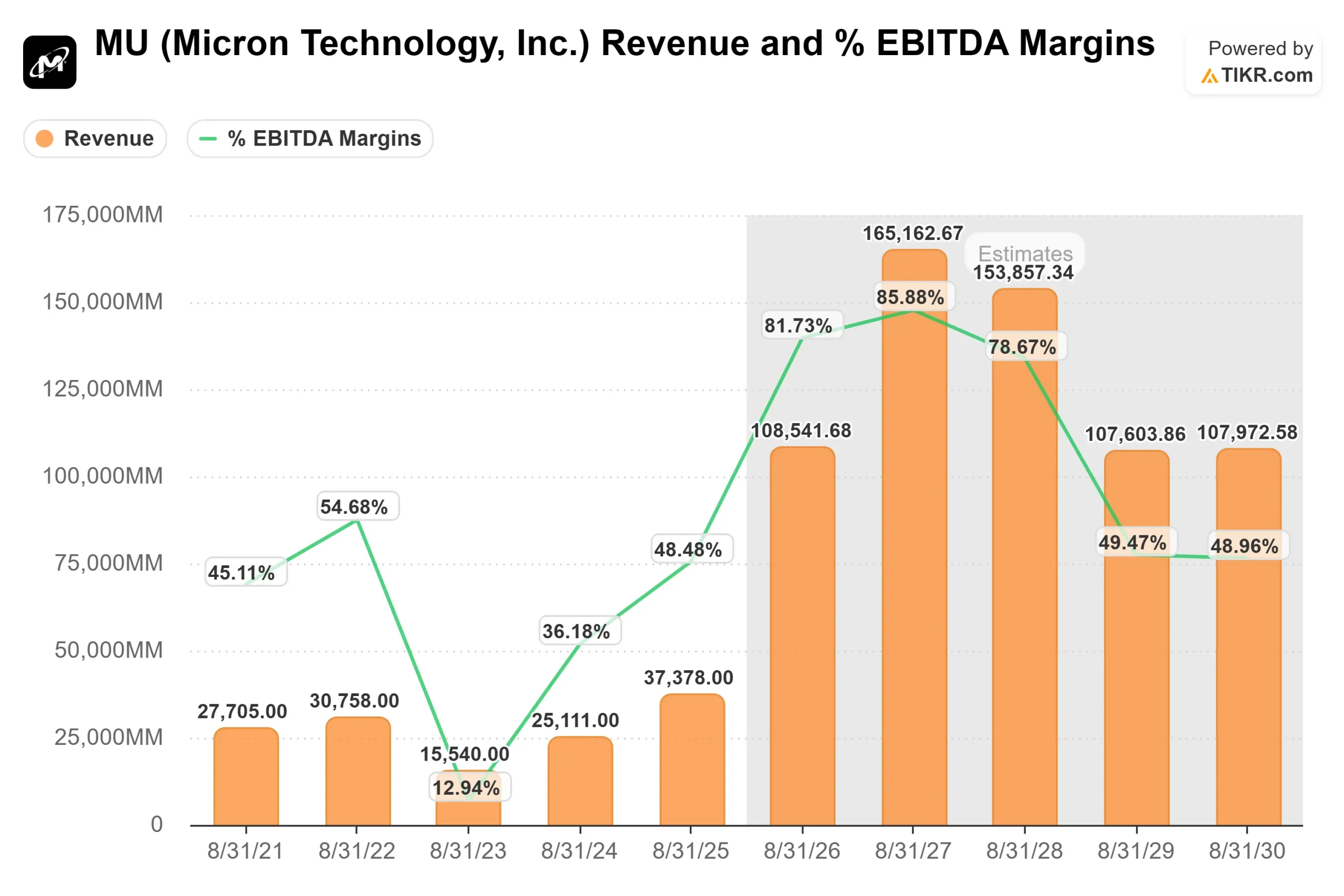

On March 18, Micron reported fiscal Q2 2026 results that crushed Wall Street.

Revenue reached $23.86 billion, nearly tripling year-over-year, and beat the LSEG consensus of $20.07 billion. Non-GAAP EPS of $12.20 surpassed the Street’s $9.31 estimate.

Despite those numbers, the stock fell (3.78%) on the day. The bar had been set so high that historic execution left investors asking what comes next.

That question became urgent on March 24, when Google Research published TurboQuant, a compression algorithm that reduces the key-value (KV) cache memory footprint of large language models by at least six times without any measurable loss in model accuracy.

The KV cache is the high-speed memory store that allows an AI model to retrieve past calculations without reprocessing them.

Memory stocks sold off immediately. Over six sessions, MU fell more than 20% from its post-earnings highs, its steepest multi-session drop since April 2025’s tariff shock.

On the Q2 call, CFO Mark Murphy stated plainly that “demand far exceeds supply” and confirmed supply constraints would persist “beyond 2026.”

The selloff is forcing investors to pressure-test whether that holds if software can do the work that hardware was expected to absorb.

See historical and forward estimates for Micron stock (It’s free!) >>>

Is Micron Undervalued Today?

At $357.22, Micron trades at 3.95x next-twelve-months (NTM) price-to-earnings, compressed even by memory sector standards.

The mean analyst price target sits at $527.60, with 38 of 45 covering analysts rating MU a Buy or Outperform. That consensus was built before TurboQuant entered the conversation.

The valuation case rests on supply constraints that management says are structural.

On the Q2 call, Chief Business Officer Sumit Sadana described Micron as “the first company in the world to have a Gen6 SSD in the market,” with demand that the company is “not able to completely even come close to meeting.”

He described data center NAND as significantly undersupplied, driven by KV cache workloads and ongoing HDD shortages. EVP of Global Operations Manish Bhatia added that HBM4 is tracking a faster yield ramp than the previous HBM3E generation.

On peers, SK Hynix trades at a NTM P/E of 4.64x against Micron’s 3.95x, a modest premium for similar AI memory exposure. Kioxia trades at an NTM EV/EBITDA of 2.75x versus Micron’s 2.85x. Against the broader semiconductor sector, where the peer-group NTM P/E mean sits at 32.58x per TIKR, Micron’s multiple reflects the market’s persistent reluctance to pay a premium for memory cyclicality, even in a structurally different cycle.

TurboQuant is, as of this writing, a laboratory result.

It will be formally presented at the International Conference on Learning Representations (ICLR) in April 2026 and has not been deployed at a production scale.

BofA Securities semiconductor analyst Vivek Arya noted in a March 26 research note that comparable compression techniques have existed since 2024 and 2025, without altering hardware procurement at scale.

He also cited Google’s own CY2026 capital expenditure of approximately $180 billion, up roughly 100% year-over-year, as evidence that the company publishing TurboQuant does not itself believe its hardware needs are shrinking.

Morgan Stanley pushed back on the selling, arguing that TurboQuant could expand AI deployment broadly and increase total memory consumption over time. Wells Fargo TMT analyst Andrew Rocha acknowledged the threat more directly, writing that TurboQuant “is directly attacking the cost curve here,” but stopped short of a bearish conclusion given that broad adoption has not yet occurred.

The harder question is whether the credible existence of a software path to lower memory intensity matters more than whether adoption actually happens.

Micron’s capex commitment of over $25 billion in FY2026 is not a hedge.

Bhatia confirmed on the call that capacity from the Singapore fab, Idaho facility, and Tongluo P5 site in Taiwan will not contribute meaningful supply until fiscal 2028. If demand softens before that capacity comes online, the spend faces a different pricing environment than it was sized for.

See how Micron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

Key Stats:

- Current Price: $357.22

- Target Price (Mid): $302.40

- Potential Total Return (Mid): (15.3%)

- Annualized IRR (Mid): (3.70%) / year

See analysts’ growth forecasts and price targets for Micron stock (It’s free!) >>>

The TIKR mid-case model (as of March 29, 2026) projects a target of $302.40 by August 31, 2030, a total return of (15.3%) and an annualized IRR of (3.70%) per year. The high case, using an 11.9% revenue CAGR and 82.4% net income margin, produces only $380.05, a 6.4% total return and a 0.7% IRR over more than four years. Neither scenario compensates investors meaningfully for the risk profile of a capital-intensive, cyclical business.

The two revenue growth drivers in the mid case are AI data center memory demand and NAND data center SSD adoption, built on an 11.4% revenue CAGR. The margin driver is the structural shift toward HBM and high-value data center DRAM, where LTM gross margin currently sits at 58.4%. The primary risk is P/E multiple compression at a (10.1%) CAGR through 2030, the market’s historical reflex when memory cycles mature. If earnings disappoint alongside multiple compression, the low case produces a target of $241.38, a (32.4%) total return, and an IRR of (4.5%) per year.

At $357.22, MU offers limited upside even in the optimistic scenario and meaningful downside if the demand narrative softens.

Conclusion: Watch data center NAND revenue at Micron’s fiscal Q3 2026 report, expected around June 24, 2026. If that segment continues accelerating, it directly rebuts the TurboQuant demand destruction thesis. If it stalls, the narrative gains credibility quickly.

Micron’s AI memory thesis is not broken. Supply constraints are real, the product portfolio is differentiated, and Q2 confirmed the cycle is running hard. But at $357.22, the TIKR mid-case model implies a negative return through 2030. TurboQuant may prove to be an overreaction. The valuation was already asking for conviction before Google published a word of research.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Micron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!