Key Stats for DUOL Stock

- Past week’s performance: -0.5%

- 52-week range: $35 to $76

- Valuation model target price: $84

- Implied upside: 29.6% over 2.8 years

Value your favorite stocks like DAL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Delta Air Lines, Inc. (DAL) stock has been choppy because investors are balancing better demand against higher external risk. On March 17, the company raised its March-quarter revenue growth outlook to 7% to 9% from 5% to 7% because demand accelerated in March. Delta also said it still expected March-quarter earnings within its initial range, which signaled that travel demand stayed healthy even as fuel costs rose.

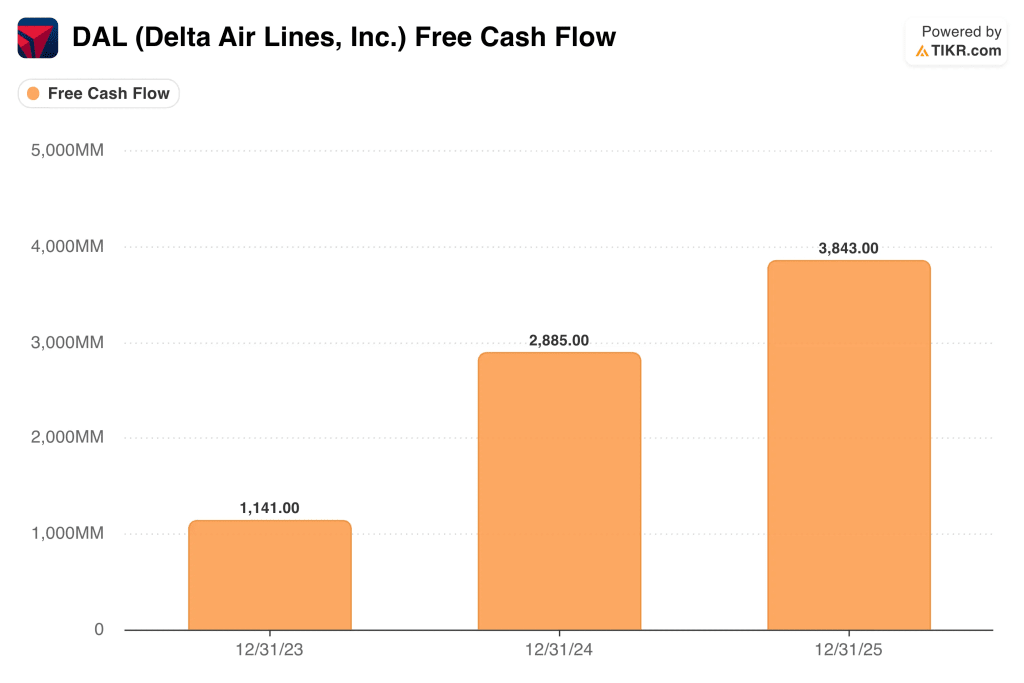

That was the bullish part of the story, and management had already framed 2026 similarly in January. CEO Ed Bastian said, “2026 is off to a strong start with top-line growth accelerating on consumer and corporate demand.” In the same release, Delta guided for full-year 2026 EPS of $6.50 to $7.50 and free cash flow of $3 billion to $4 billion.

But the market is also pricing in cost pressure and operational risk. Reuters reported that jet fuel prices surged as conflict-driven supply fears widened the gap between crude and jet fuel, and Delta said fuel costs rose about $400 million in March alone. Reuters also reported Delta extended the pause on New York-JFK to Tel Aviv service, and later extended the broader JFK and Atlanta-Tel Aviv pause through Sept. 5.

Operational headlines added more noise during the week. Delta resumed operations at LaGuardia after a disruption tied to an airport collision, but the delays and cancellations still kept airlines in focus. So the stock’s recent move looks less like a change in demand and more like investors weighing stronger revenue against higher fuel, geopolitical, and execution risks.

See analysts’ growth forecasts and price targets for DAL (It’s free) >>>

Is DAL Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.1%

- Operating Margins: 10.6%

- Exit P/E Multiple: 9.1x

Based on these inputs, the model estimates a target price of $84, implying 29.6% total upside from the current share price and a 9.8% annualized return over the next 2.8 years.

Delta does not look expensive on current earnings multiples, but the model also does not point to an especially high-return setup. The stock trades at about 8.5x LTM earnings and 0.9x LTM revenue, while the model assumes a 9.1x exit P/E. That tells you the market is already valuing Delta more like a cyclical industrial business than a high-multiple growth stock.

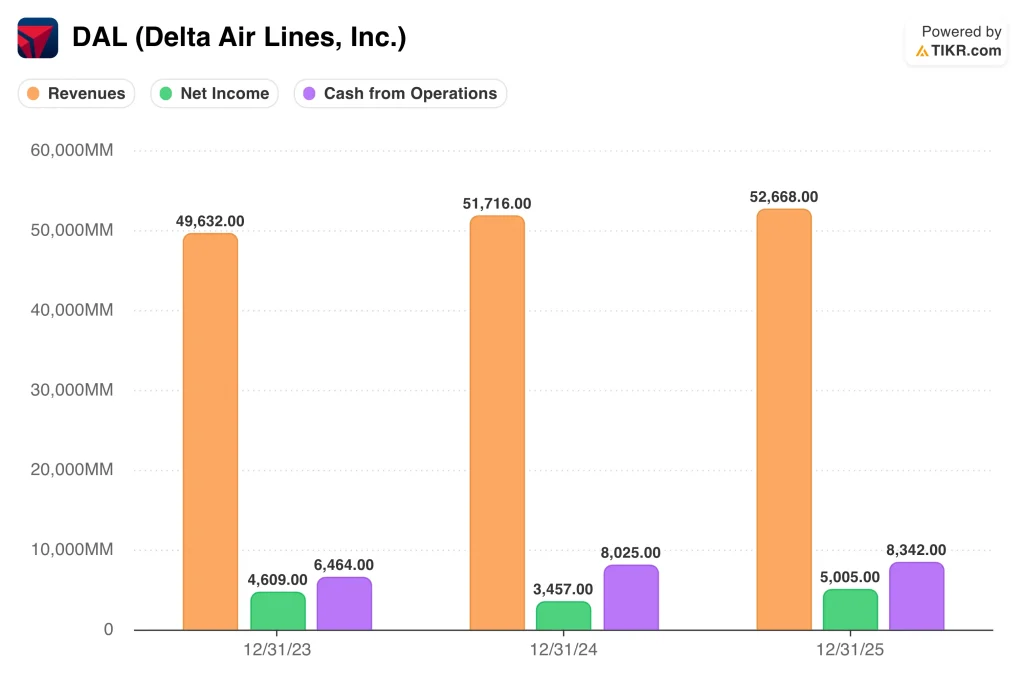

The business has improved a lot since the pandemic, and the numbers show why. Full-year revenue reached $63.4 billion in 2025, net income rose to $5.0 billion, and operating cash flow was $8.3 billion. Delta also reduced adjusted net debt to about $14.3 billion at year-end, down $3.7 billion from the prior year.

Still, margins remain sensitive to fuel and operations. LTM EBIT margin is 8.9%, and the valuation model only assumes operating margins of 10.6% through 2028, so a lot depends on disciplined capacity, premium demand, and cost control. That setup can support fair value, but it also explains why the stock can stall when oil rises, or headlines disrupt travel.

Delta also compares reasonably well with peers on balance-sheet progress and revenue diversity. President Glen Hauenstein said premium, cargo, MRO, and loyalty streams helped diversified revenue reach 60% of total revenue in 2025. That matters because those businesses can make earnings less dependent on base-ticket pricing alone.

What’s Driving the DAL Stock Going Forward?

The next big catalyst is Delta’s Q1 2026 earnings report on April 8. Investors will want to see whether the higher March demand trend held through quarter-end and whether management changes its full-year view. Because the stock is already discounting a decent recovery, even small changes in revenue or margin outlook could move shares.

Fuel is still the biggest swing factor. Reuters reported that Delta’s refinery hedge has become more valuable in a jet-fuel squeeze, and that advantage can help relative performance when refining margins spike. But even with that hedge, Delta still faced a large March fuel-cost increase, so investors are watching whether fares and premium demand can offset it.

International and premium demand also matter because they are key profit drivers. In January, Delta said premium revenue grew 7% in 2025, cargo grew 9%, MRO grew 25%, and loyalty revenue improved 6%. If those higher-margin streams keep growing, they can support earnings even if the domestic environment gets noisier.

Finally, investors will watch for more updates on network stability and geopolitics. Tel Aviv route suspensions, airport disruptions, and broader conflict-related travel uncertainty can all affect sentiment even when underlying bookings remain solid. So the next move in Delta stock likely depends on whether stronger demand keeps overpowering fuel and headline risk.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Delta Air Lines, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DAL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DAL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Delta Air Lines stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!