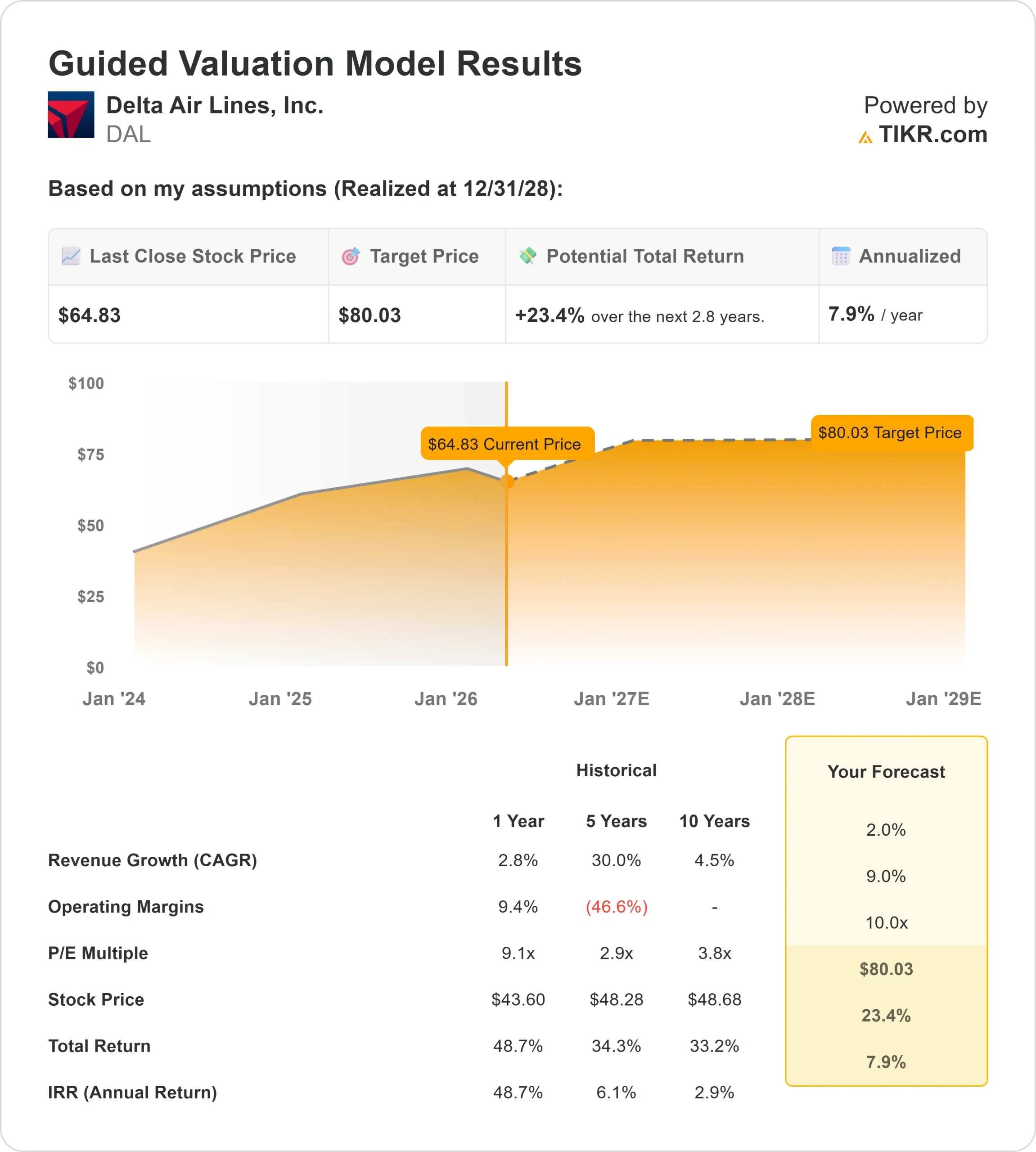

Key Stats for DAL Stock

- Past-6-Month Performance: 13%

- 52-Week Range: $35 to $76

- Valuation Model Target Price: $80

- Implied Upside: 23%

Analyze your favorite stocks like Delta Air Lines with TIKR (It’s free) >>>

What Happened?

Delta Air Lines stock is at the center of a key debate in 2026 around whether strong travel demand can translate into durable profits as costs rise, with the company standing out due to its premium-focused model and generally stronger margins than competitors like United Airlines and American Airlines, which rely more heavily on price-sensitive travelers and have faced more pressure on profitability.

Delta Air Lines stock is up about 13% over the past 6 months, recently trading near $65 per share, primarily because strong travel demand and pricing power in higher-margin segments have supported revenue growth and investor confidence.

Premium revenue streams, including business travel and credit card partnerships, generate more profit per customer, allowing Delta to better offset rising costs compared to peers, even as jet fuel costs have nearly doubled this year and added about $400 million in incremental costs in March alone.

Delta highlighted continued strength in bookings, with 8 of its 10 highest sales days occurring this quarter and sales rising 25% year over year over the past week, supported by broad-based demand across corporate, international, and premium travel.

CEO Ed Bastian said at the JPMorgan Industrials Conference, “over the last week, our sales are up 25% on a year-over-year basis,” reinforcing that demand remains strong even as the company faces operational disruptions from winter weather that reduced capacity by about 2 points.

Analyst and institutional activity reinforced a constructive but balanced outlook. UBS raised its price target from $83 to $84 and maintained a buy rating, implying roughly 29% upside, while firms like Wealth Enhancement Advisory Services increased its stake by 12.6% to 223,170 shares and Nordea Investment Management raised its position by 86.1%, even as Skandia reduced its stake by 67.3% and Regent Peak cut its position by 47.1%, alongside insider selling of about 620,550 shares worth roughly $44 million over the past 90 days, leaving institutional ownership near 70%.

Value Delta Air Lines instantly (Free with TIKR) >>>

Is DAL Undervalued?

Under valuation assumptions, the stock is modeled using:

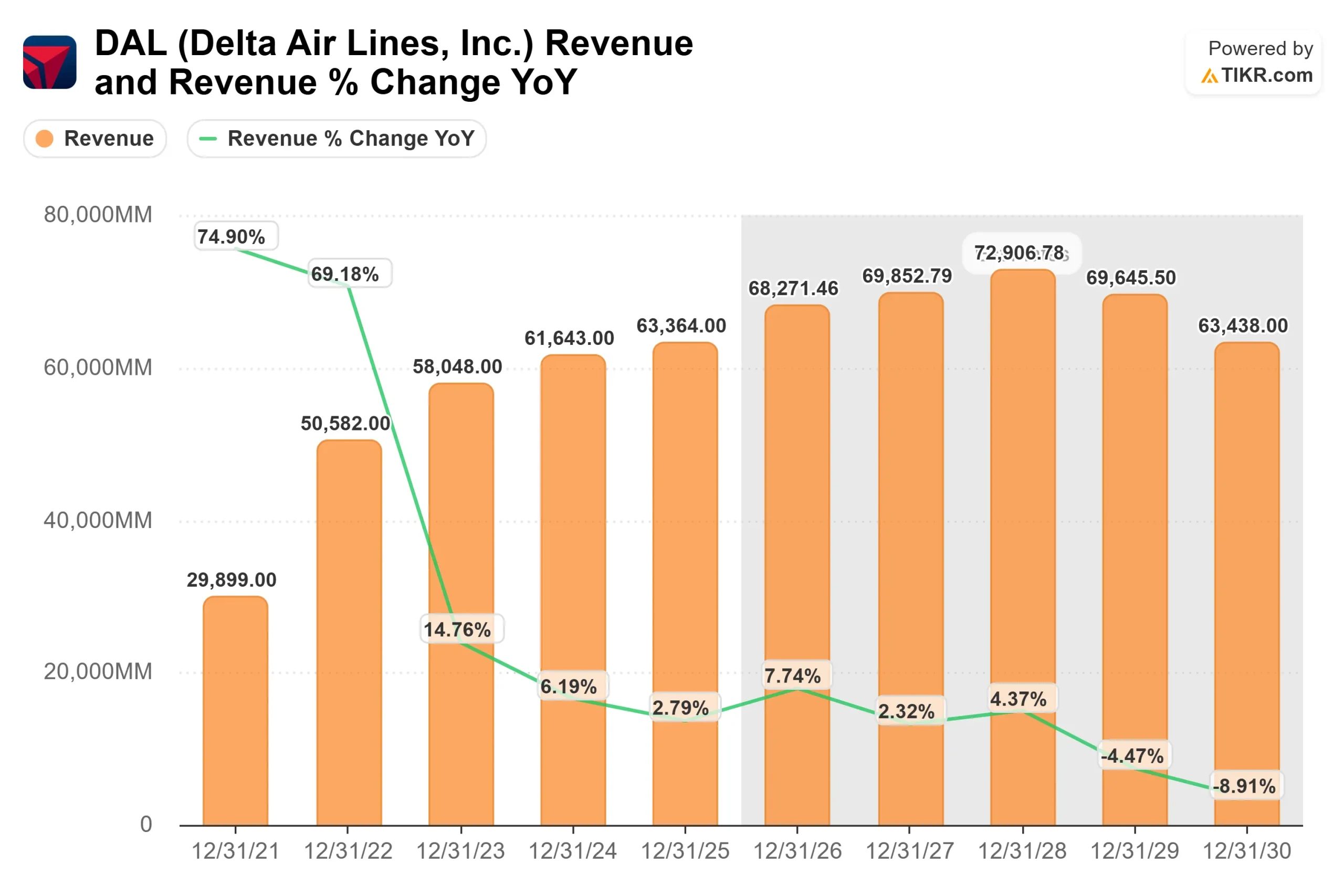

- Revenue Growth (CAGR): 2%

- Operating Margins: 9%

- Exit P/E Multiple: 10x

Delta’s growth outlook reflects a more mature airline industry, where demand remains stable but no longer benefits from the sharp post-pandemic rebound, keeping revenue growth in the low-single-digit range.

See analysts’ growth forecasts and price targets for Delta Air Lines (It’s free) >>>

Margins are the key driver, as Delta’s premium strategy, which includes higher-paying business travelers, loyalty partnerships like American Express, and international routes, supports profitability through higher-margin revenue and more stable demand, supported by premium mix and pricing discipline.

This matters because airlines with pricing power and premium exposure tend to recover fuel cost increases faster, while weaker carriers often struggle to maintain margins during cost spikes.

Based on these inputs, the model estimates a target price of about $80, implying roughly 23% total upside over the next 2.8 years, suggesting the stock appears undervalued at current levels.

Over the next year, performance will likely be driven by continued strength in premium travel demand, recovery in corporate bookings, and the company’s ability to maintain pricing power without heavy discounting.

At the same time, cost discipline, particularly around fuel and labor, will determine whether margins can expand further.

At current levels, Delta Air Lines appears undervalued, with future performance driven by premium revenue growth, pricing power, and margin stability rather than rapid revenue expansion.

How Much Upside Does AEP Stock Have From Here?

Investors can estimate Delta Air Lines’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Delta Air Lines in under 60 seconds with TIKR (It’s free) >>>