Key Stats for Deere Stock

- Past-Week Performance: +1.2%

- 52-Week Range: $404.4 to $674.2

- Current Price: $566.6

What Happened?

Deere & Company (DE), the world’s largest farm-equipment maker, raised its fiscal 2026 net income guidance to $4.5 billion to $5.0 billion on February 19 after Q1 revenue surged 13% to $9.6 billion, beating the IBES estimate of $7.7 billion, while the stock trades at $566.64 against a 52-week high of $674.19.

Q1 diluted EPS of $2.42 beat the IBES estimate of $2.05, driven by Construction and Forestry net sales jumping 34% to $2.67 billion as the segment, which sells excavators, road-building equipment, and compact machinery, saw its order bank rise over 50% in a single quarter to its highest level since May 2024.

Small Agriculture and Turf, the segment covering compact tractors, turf equipment, and dairy-and-livestock machinery that generates higher-margin replacement demand, delivered a 58% year-over-year jump in operating profit to $196 million on a 9.0% margin, while Construction and Forestry operating profit more than doubled, offsetting a 4.4% margin in Production and Precision Agriculture weighed down by $1.2 billion in full-year tariff costs.

On the same day Deere reported earnings, the company also completed its acquisition of Tenna, a fleet management platform that automates contractor workflows and provides near real-time equipment insights, adding a brand-agnostic digital layer to the Construction and Forestry segment alongside Virtual Superintendent, acquired roughly one year prior, as Deere builds out a three-layer strategy covering machines, job-site tasks, and full-fleet optimization.

Moreover, Joshua Jepsen, Chief Financial Officer, stated on the Q1 2026 earnings call that “our financial strength has allowed us to maintain high levels of investment throughout the cycle, which positions us well for future growth, particularly as the cycle inflects,” tying directly to the construction order bank surge and the upcoming CONEXPO launch of Deere’s first fully designed and Kernersville, North Carolina-built 20-ton excavator.

Deere’s commitment to invest $20 billion in U.S. manufacturing over the next decade, the Kernersville excavator campus opening, nearly $750 million returned to shareholders in Q1 alone through dividends and share repurchases, and 500 million engaged precision agriculture acres growing over 10% year-over-year together position the company to capture outsized incremental margins as the agricultural cycle inflects from its 2026 trough.

Wall Street’s Take on DE Stock

The February 19 guidance raise to $4.5 billion to $5.0 billion in net income, powered by Construction and Forestry’s 34% revenue surge and a 50%-plus order bank expansion, confirms the cycle bottom management called on the Q1 2026 earnings call.

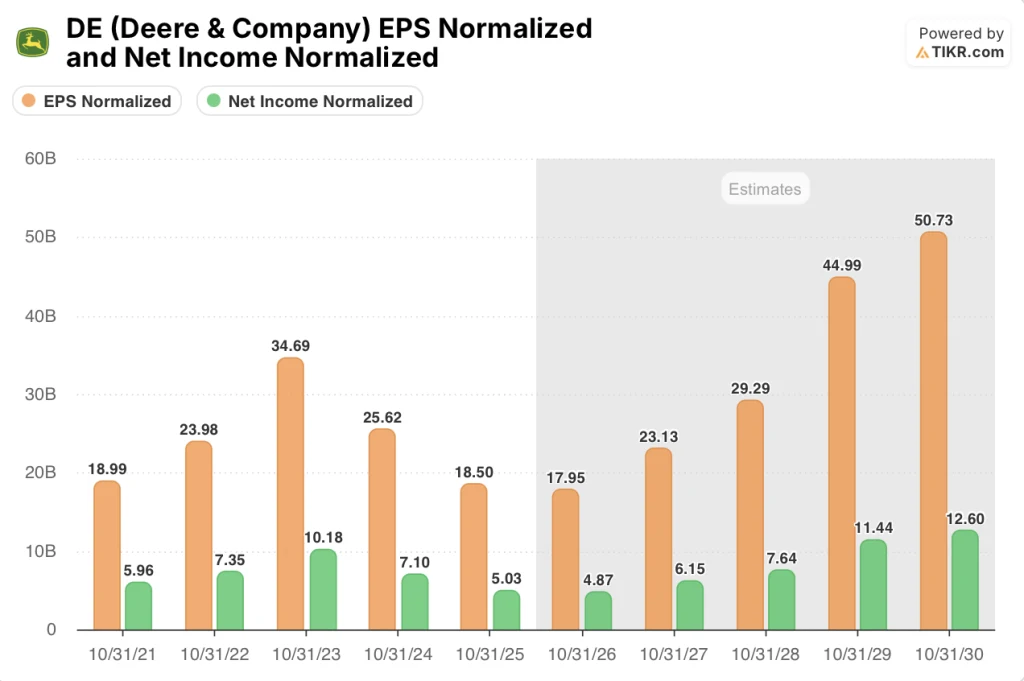

Normalized EPS troughed at an estimated $17.95 in FY2026 after falling from $34.69 in FY2023, and as TIKR estimates, EPS recovers to $23.13 in FY2027 and $44.99 by FY2029, a recovery trajectory supported by lean field inventory, strengthening order books through Q4, and the biofuel mandate tailwind management flagged on the February 19 call.

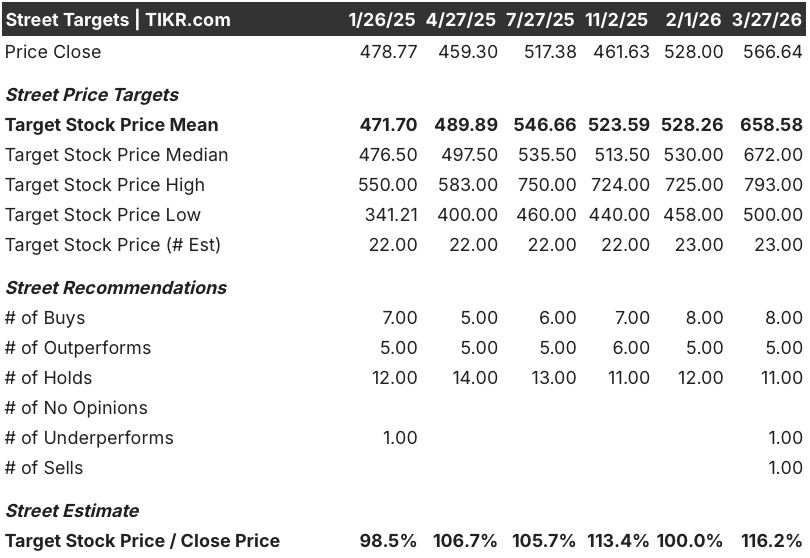

Thirteen of 23 analysts covering DE rate it a buy or outperform, with a mean street price target of $658.58 implying 16.2% upside from the current $566.64, reflecting broad conviction that the order book surge in Construction and Forestry and the SAT segment’s 58% operating profit jump signal an earnings inflection, not a one-quarter anomaly.

The street target range spans $500.00 on the low end to $793.00 on the high end, where bears anchor to the $1.2 billion tariff drag and still-depressed large ag fundamentals, while bulls point to the C&F order bank at its highest since May 2024 and the upcoming CONEXPO excavator launch as the share-gain catalyst.

What Does the Valuation Model Say?

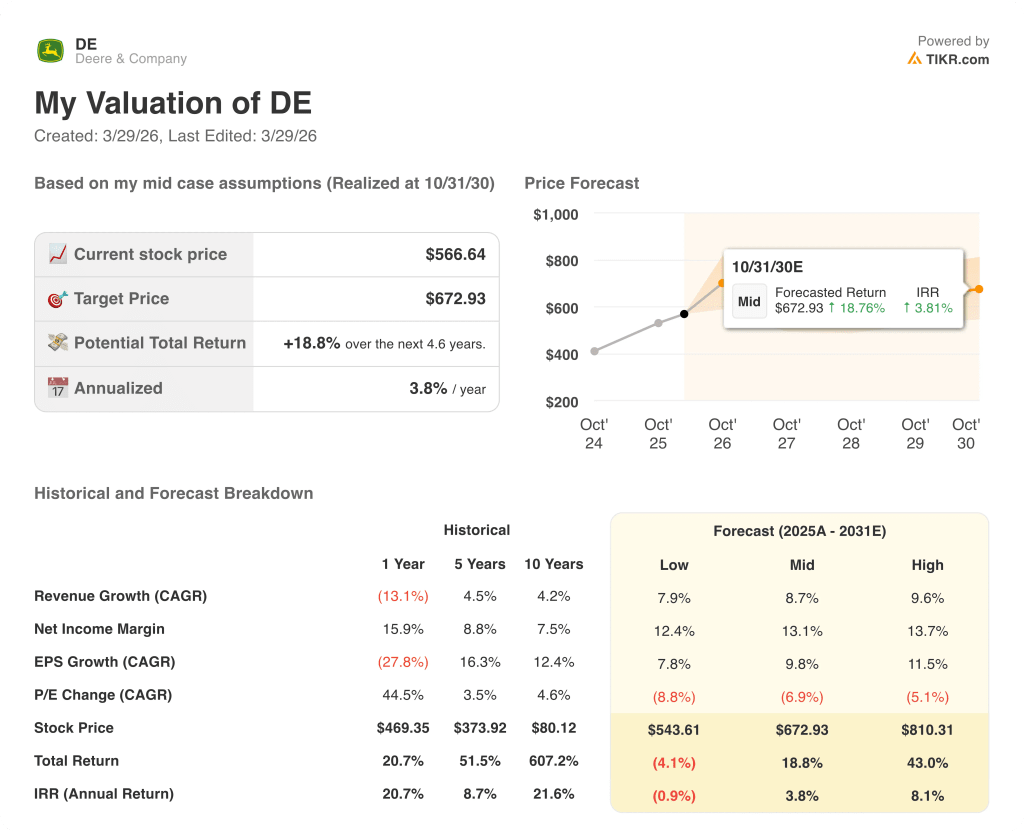

The TIKR mid-case model prices DE at $672.93 by October 2030, built on an 8.7% revenue CAGR, a net income margin recovery to 13.1% from the current 11.8% trough, and a 9.8% EPS CAGR, all of which the February 19 guidance raise, the SAT margin expansion to 9.0%, and the C&F operating profit doubling make credible rather than aspirational.

The market prices DE as if the trough is ahead; the 50%-plus C&F order bank surge and combine EOP finishing better than the 15%-to-20% industry decline range confirm it has already arrived.

The TIKR model’s $672.93 target rests on the earnings recovery materializing from FY2027 onward, and the Q1 order book visibility into Q4, with large tractor build rates already stepping up in the back half, provides the earliest concrete confirmation that FY2027’s estimated $23.13 EPS is tracking.

CFO Joshua Jepsen’s point on the February 19 call that factories are running lean and strong incrementals should follow as demand returns signals management sees the same EPS inflection the TIKR model prices in from FY2027.

A sustained deterioration in North American large ag fundamentals, particularly if grain prices fail to recover and the USDA’s forecasted 0.7% net farm income decline deepens, breaks the FY2027 EPS recovery assumption and collapses the model’s $672.93 target.

Q2 fiscal 2026 results will reveal whether North American large ag production ramp-up held and whether the C&F order bank translated into realized revenue; watch for PPA operating margin clearing 11% as the earliest signal the cycle has turned.

Should You Invest in Deere & Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Deere & Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DE stock on TIKR for Free →