Key Stats for Epam Stock

- Past-Week Performance: -1.6%

- 52-Week Range: $125.6 to $222.5

- Current Price: $135.2

What Happened?

EPAM Systems (EPAM) delivered more than $105 million in pure AI-native revenues in Q4 alone, a figure that signals a structural identity shift for the Newtown, Pennsylvania-based IT services provider, even as its stock trades at $135.19, near a 52-week low of $125.57.

On February 19, CEO Balazs Fejes and CFO Jason Peterson reported Q4 revenue of $1.41 billion, beating the $1.39 billion consensus, with non-GAAP EPS of $3.26 clearing the $3.16 estimate, while full-year 2026 organic constant currency guidance of 3% to 6% disappointed investors who had expected acceleration beyond 2025’s 4.9% pace.

The result that makes the thesis undeniable is EPAM’s free cash flow trajectory: Q4 operating cash flow surged to $283 million from $130 million in the prior-year period, and full-year 2025 free cash flow reached $613 million at a 94.7% adjusted net income conversion rate, a level of capital generation that funded $661 million in buybacks during 2025 and underwrites the $300 million accelerated share repurchase announced March 5 with Morgan Stanley.

Last January, EPAM announced a strategic partnership with Cursor, a leading AI-native coding platform, to build and deploy AI-native engineering teams for global enterprises, adding a go-to-market channel that directly targets the enterprise AI transformation spending wave EPAM’s own pipeline data confirms is accelerating.

Jason Peterson, Chief Financial Officer, stated on the Q4 2025 earnings call that “with the share price where it is today, you’ll continue to see us reasonably active in terms of share repurchases, particularly in the first half of 2026,” a comment that preceded the March 5 ASR announcement and leaves $452.5 million remaining under the existing $1 billion authorization.

EPAM’s target to scale AI-native revenues past $600 million in 2026, combined with a three-year commitment to reach 16% plus non-GAAP operating margins by 2028 and generate more than $1.8 billion in cumulative free cash flow, frames a recovery arc that the current valuation, near the 52-week low, has not yet begun to price.

Wall Street’s Take on EPAM Stock

The Q4 revenue beat and the $300 million accelerated share repurchase together confirm that EPAM’s management is treating the post-guidance selloff as a mispricing, not a fundamental deterioration, and that inflection directly reshapes the FY2026 earnings trajectory.

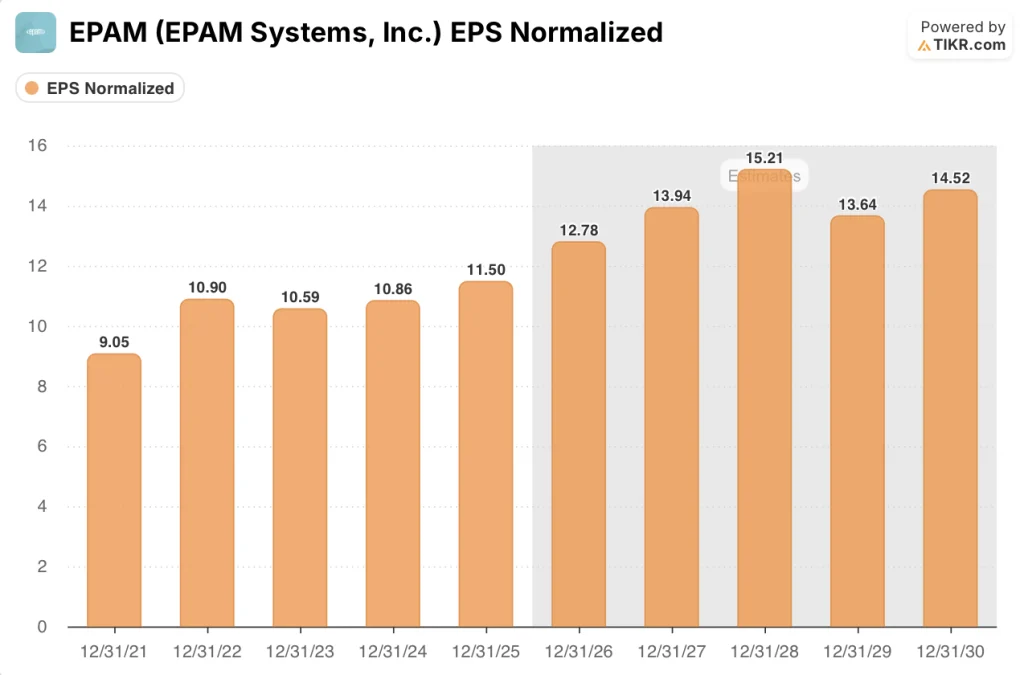

Meanwhile, TIKR estimates normalized EPS rising from $11.50 in FY2025 to $12.78 in FY2026E and $15.21 in FY2028E, a compounding growth path anchored by AI-native revenue scaling past $600 million and the gross margin expansion Peterson explicitly committed to on the Q4 call.

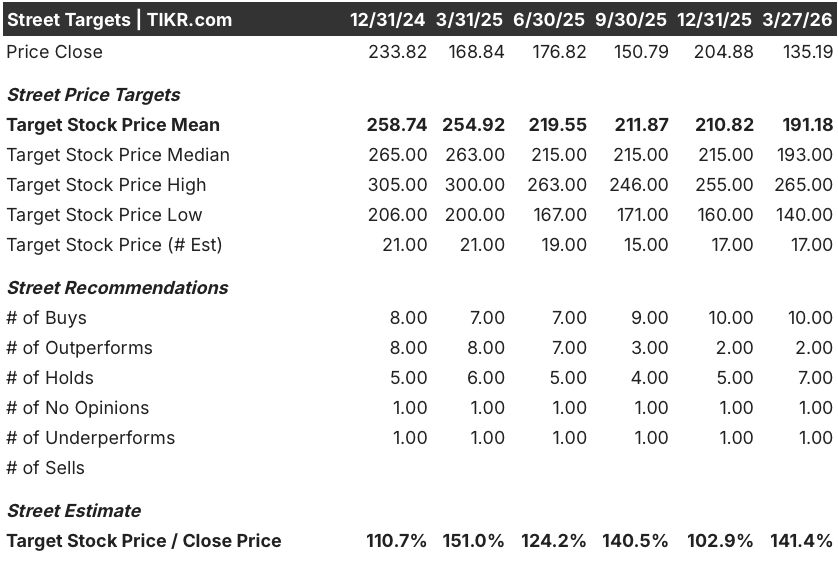

Twelve of 17 analysts currently rate EPAM a buy or outperform, with a mean price target of $191.18 implying 41.4% upside from the March 27 close of $135.19, and the high target of $265.00 reflects conviction that AI-native and foundational services displace the NEORIS headwind within two quarters.

The $140.00 low target reflects the bear case that the NEORIS revenue drag and a still-sluggish enterprise decision-making environment compress organic growth below the 3% floor of FY2026 guidance, while the $265.00 high requires the $600 million AI-native target to land on schedule and margin expansion to track Peterson’s 50 to 70 basis point annual gross margin improvement roadmap.

What Does the Valuation Model Say?

The TIKR mid-case price target of $190.94, reached by December 2030, assumes 6.5% revenue CAGR from FY2025 through FY2031E and EBITDA margins expanding from 16.2% in FY2025 to 19.8% by FY2030E, driven by the pyramid restructuring, India profitability gains, and AI productivity sharing management outlined at the March 12 Investor Day.

The market is pricing EPAM at roughly 10.6x FY2026E normalized EPS of $12.78, a discount that ignores $613 million in FY2025 free cash flow and a $1.8 billion cumulative FCF commitment through FY2028.

TIKR’s $190.94 target requires 6.5% revenue CAGR, a level management’s own 4.5% to 7.5% FY2026 reported revenue guidance brackets from below, with the Cursor partnership and AI-native pipeline providing the upside driver.

Moreover, Peterson’s confirmation of low single-digit bill rate increases from European and North American clients entering FY2026 directly contradicts the market’s implicit assumption that AI is compressing EPAM’s pricing power.

The risk is NEORIS: if Mexico’s largest client deteriorates beyond the guided mid-single-digit sequential decline, the negative 100 basis point FY2026 organic growth headwind widens and breaks the EBITDA margin expansion assumption entirely.

Q1 2026 results, due in approximately six weeks, will confirm whether the NEORIS stabilization Peterson described holds; watch for organic constant currency growth at or above the 3% midpoint and non-GAAP operating margin within the guided 13.5% to 14.5% range.

Should You Invest in EPAM Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EPAM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track EPAM Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EPAM stock on TIKR for Free →