Key Stats for Nucor Stock

- Past-Week Performance: +3%

- 52-Week Range: $97.6 to $196.9

- Current Price: $163.4

What Happened?

Nucor (NUE), the largest steel producer in the Western Hemisphere, delivered a guidance raise that snaps a year of margin pressure, guiding Q1 2026 EPS to $2.70–$2.80 against a Q4 2025 adjusted EPS of $1.73, with shares trading at $163.37 against a 52-week high of $196.90.

On March 19, Wells Fargo raised its Nucor price target to $194 from $184 and lifted its 2026 hot-rolled coil forecast to $950 per short ton, citing a self-sufficient domestic steel market shielded by 50% Section 232 tariffs that management expects to compress foreign import share to roughly 14% of U.S. finished steel consumption.

Steel Mills backlogs, the order book for Nucor’s primary steelmaking segment that drives the bulk of pretax earnings, entered 2026 up 40% year-over-year, with the structural group alone carrying a backlog more than 15% above its own Q1 2025 record, underpinning a 5% full-year shipment growth target.

Leon Topalian, Chair and CEO, stated on the Q4 2025 earnings call that “we entered the year with historically strong backlogs, up nearly 40% year-over-year in the steel mills segment and 15% in steel products,” connecting directly to the company’s February 20 approval of a fresh $4 billion share repurchase program replacing its prior exhausted authorization.

Nucor’s $2.5 billion estimated 2026 capital plan, down meaningfully from $3.4 billion spent in 2025, shifts the company from construction mode to cash generation, with the West Virginia sheet mill targeting automotive and appliance markets set to come online by year-end and incremental EBITDA from four recently completed projects expected to contribute roughly $500 million above 2025 levels.

Wall Street’s Take on NUE Stock

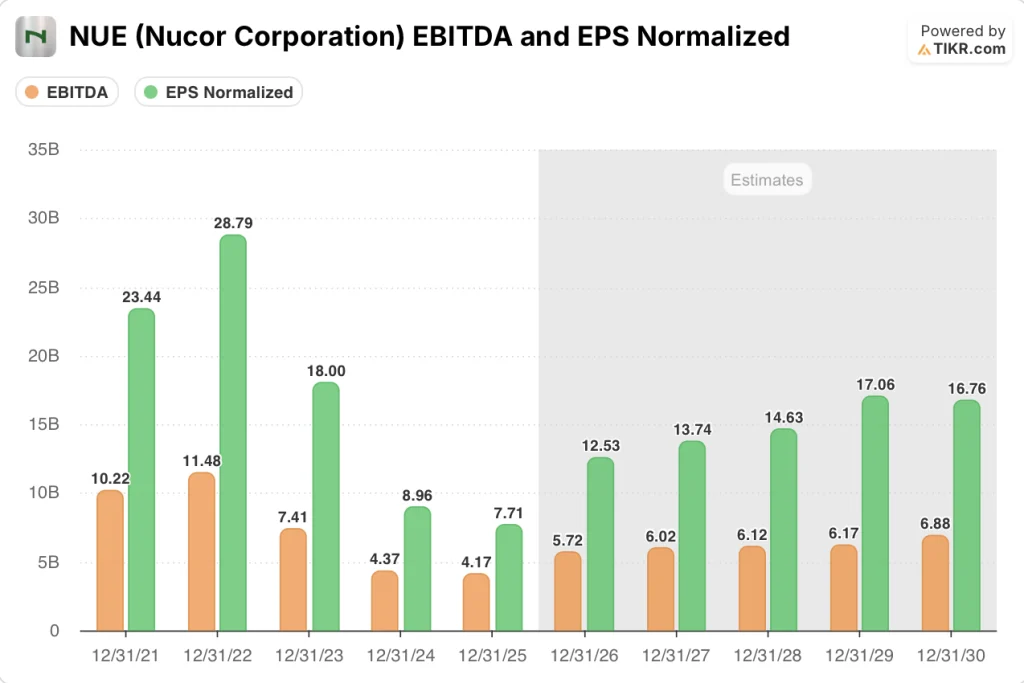

The Q1 2026 EPS guidance of $2.7–$2.8, a 57% sequential jump from Q4 2025’s adjusted $1.73, signals that Nucor’s three-year capital build is finally converting into earnings, with EBITDA margins as TIKR estimates expanding from 12.8% in 2025 to 15.8% in 2026.

That margin recovery is powered by two concurrent forces: as TIKR estimates, normalized EPS surges 62.6% from $7.71 in 2025 to $12.53 in 2026, driven by $500 million in incremental EBITDA from the four completed projects and Steel Mills pricing recovery flowing through from November’s price increases.

Fourteen of 15 analysts covering NUE rate it a buy or outperform, with a mean price target of $187.92 implying 15.0% upside from $163.37, as the Street prices in the CapEx step-down and backlog strength but has yet to fully credit the free cash flow inflection.

The analyst target range spans $162 to $206, where the low end reflects tariff rollback risk if the Trump administration exempts products from Section 232 coverage, and the high end assumes the West Virginia sheet mill ramps into automotive markets on schedule by year-end.

What Does the Valuation Model Say?

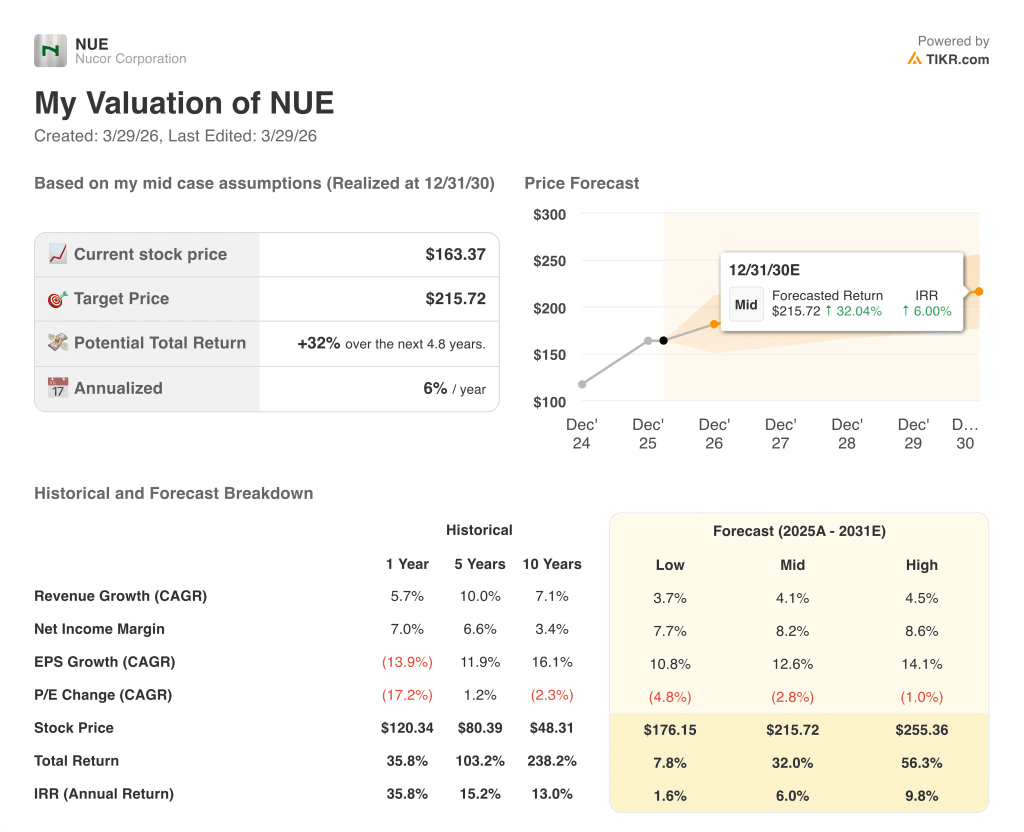

The TIKR mid-case model prices NUE at $215.72, implying 32.0% total return over 4.8 years at a 6.0% IRR, anchored by a 4.1% revenue CAGR and net income margin expansion from 5.5% in 2025 to 8.2% by 2030, justified by the CapEx drop from $3.4 billion to $2.5 billion releasing capital that was suppressing reported earnings.

The market is treating NUE as a commodity cyclical at 0.80x NAV per share, while the company trades through a structural free cash flow inflection that peer Steel Dynamics has not matched in backlog scale or project pipeline depth.

As TIKR estimates, free cash flow swings from negative $190 million in 2025 to $1.91 billion in 2026 and $3.27 billion by 2027, directly funding the new $4 billion buyback authorization and justifying the TIKR $215.72 target.

CEO Leon Topalian’s confirmation of record Steel Mills backlogs up 40% year-over-year, paired with the structural group’s backlog running 15% above its own prior record, confirms Nucor’s pricing power is demand-driven, not tariff-dependent.

The key risk is a partial Section 232 tariff exemption: the February 13 Financial Times report sent NUE down nearly 3% in a single session, and any formal rollback would compress the $950 per short ton HRC forecast Wells Fargo embedded in its $194 price target.

Q1 2026 earnings, expected around late April, will confirm whether the $2.70–$2.80 EPS guidance holds and whether Steel Mills volume growth tracks the 5% full-year shipment target management set on the January 27 call.

Should You Invest in Nucor Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NUE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Nucor Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NUE stock on TIKR for Free →