Key Stats for Vulcan Materials Stock

- Past-Week Performance: +1.2%

- 52-Week Range: $218.9 to $331.1

- Current Price: $261.5

What Happened?

Vulcan Materials (VMC), the largest U.S. producer of construction aggregates including crushed stone, sand, and gravel used across every major construction category, set a $20-per-ton cash gross profit target at its March 12 Investor Day, nearly doubling the $11.33 it delivered in 2025 on 227 million tons.

On February 17, Vulcan posted Q4 adjusted EPS of $1.70 against a $2.11 LSEG consensus estimate, sending shares down 7.8% premarket to $302, as weak single-family residential construction, an unusually wet Southern California winter, and timing-related repair and insurance costs compressed quarterly adjusted EBITDA to $518 million versus a $604 million estimate.

Aggregates pricing, the segment’s central unit-economics driver and the metric most directly tied to long-term per-ton profitability, grew 5% on a mix-adjusted basis in Q4, but reported pricing trailed that figure by roughly 300 basis points as heavy base-stone shipments to fast-moving data center projects temporarily dragged the realized average selling price below cleaned, sized stone levels.

CEO Ronnie Pruitt stated at the March 12 Investor Day that “we now believe we have a line of sight to deliver $20 per ton of cash gross profit on those same 260 million to 270 million tons,” grounding the target in the same volume frame Vulcan originally set for its prior $11-to-$12 goal, which it achieved on far fewer tons.

Vulcan’s $4.5 billion to $5.0 billion long-term EBITDA target, supported by a pipeline of 17 active greenfield projects, a 6% quarterly dividend increase to $0.52 per share announced February 13, and a 1.8x net leverage ratio that management explicitly characterized as M&A-ready, positions the company to compound aggregates unit profitability even before any volume recovery in single-family residential construction materializes.

Wall Street’s Take on VMC Stock

The Q4 EPS miss obscures what the full-year data actually confirms: Vulcan’s aggregates cash gross profit per ton, the unit economics metric that directly drives earnings, grew 7% in 2025 and has now compounded at 13% annually for three consecutive years.

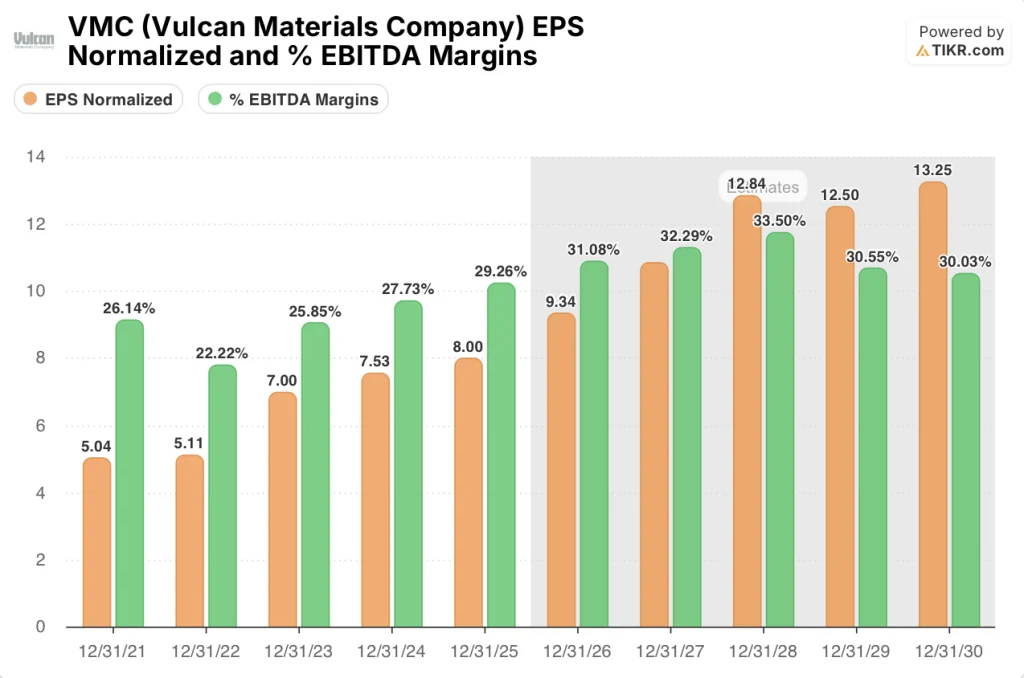

Normalized EPS reached $8.00 in 2025 as Vulcan held aggregates unit cash cost growth below 2% while pushing freight-adjusted selling prices 5% higher on a mix-adjusted basis; as TIKR estimates, that price-cost spread widens further under guided 4% to 6% 2026 price increases and continued Process Intelligence cost discipline, driving EPS to $9.34 in 2026 and $10.85 in 2027 and expanding EBITDA margin from 29.3% to 32.3%.

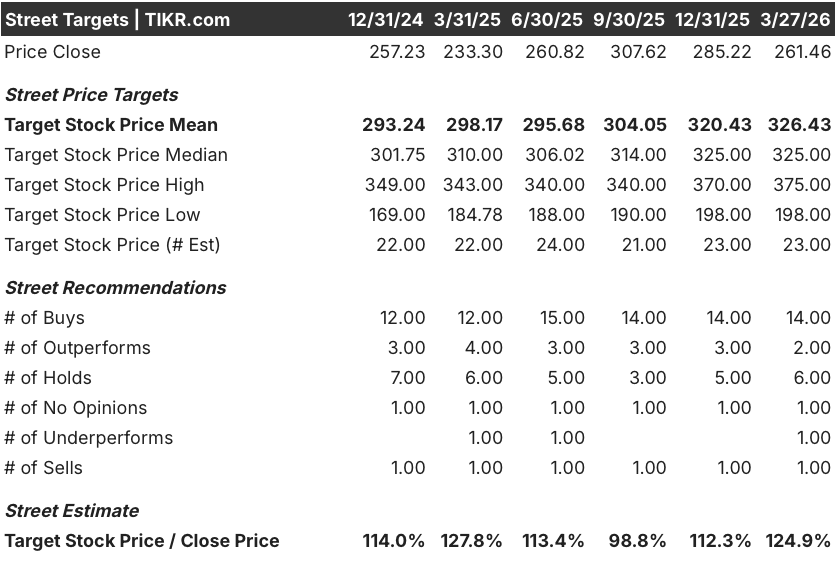

Fourteen buys, two outperforms, six holds, one underperform, and one sell across 23 analysts produce a mean price target of $326.43, implying 24.9% upside from $261.46, with the Street anchoring on sustained aggregates pricing power and the IIJA infrastructure spending tail through 2027.

The spread between the $375.00 high target and the $198.00 low target reflects a genuine binary: the high assumes residential construction recovery and midyear price increases materialize, while the low prices in prolonged single-family weakness and further data center base-stone mix drag.

What Does the Valuation Model Say?

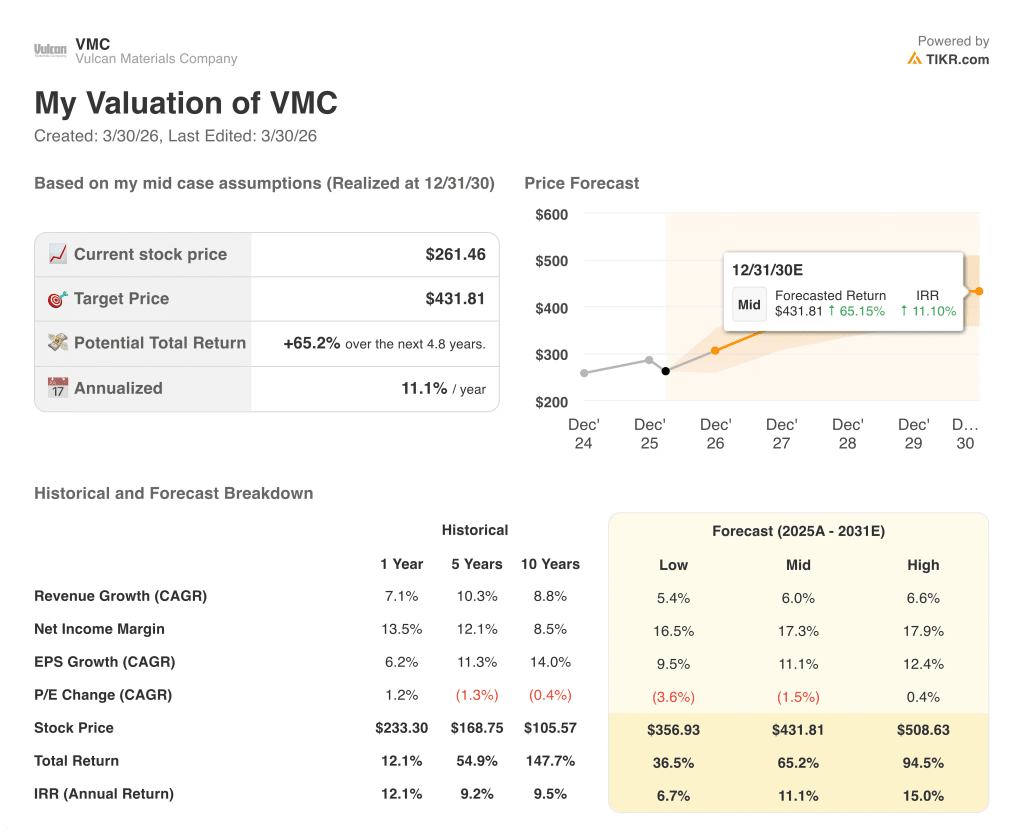

The TIKR mid-case model targets $431.81 by December 2030, a 65.2% total return at an 11.1% IRR, built on a 6.0% revenue CAGR and net income margin expansion from 13.4% in 2024 to 17.3%, justified by Vulcan’s documented ability to achieve its $11-to-$12 per-ton target on 227 million tons rather than the 260 to 270 million originally required.

The market is pricing VMC at $261.46 as if the Q4 timing costs and weather drag are structural, but Process Intelligence sites posted less than 1% production cost growth in 2025 against a 2.6% increase at non-PI plants.

The $1.14B in 2025 free cash flow, as TIKR estimates growing to $1.44B by 2027, justifies the TIKR $431.81 target, as Vulcan’s 1.8x net leverage and active M&A pipeline give it compounding optionality the current price does not reflect.

CEO Ronnie Pruitt’s March 12 confirmation that large-project bookings now convert to shipments in two to three months rather than the historical six signals accelerating revenue recognition that the Q4 results have not yet captured.

Residential construction remaining depressed through 2026 breaks the TIKR model’s low single-digit volume growth assumption; without that floor, per-ton cost efficiencies lose their operating leverage tailwind and EBITDA margin expansion stalls below 31%.

Q1 2026 results are the first confirmation point: aggregates shipment volume growth within the guided 1% to 3% range, and any midyear price increase announcement, directly validate whether the per-ton compounding thesis is tracking on schedule.

Should You Invest in Vulcan Materials Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VMC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vulcan Materials Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VMC stock on TIKR for Free →