Key Stats

- 52-Week Range: $100 to $240

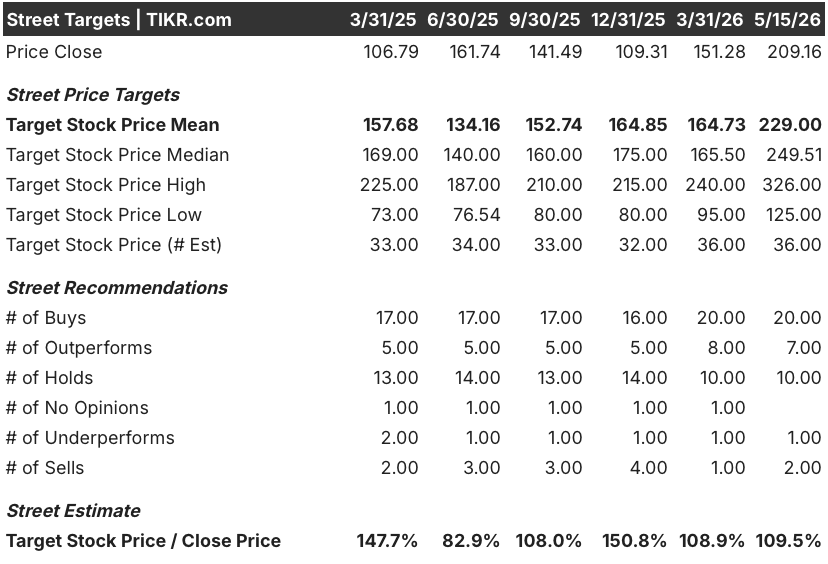

- Current Price: $209

- Street Mean Target: $229

- Street High Target: $326

- Analyst Consensus: 20 Buys, 7 Outperforms, 10 Holds, 1 Underperform, 2 Sells

- TIKR Model Target (Dec. 2030): $1,175

Arm Stock Closes a Record Fiscal Year and Bets $100 Billion on the Agentic CPU

Arm Holdings (ARM) designs the computing architecture that powers virtually every smartphone on earth, and following fiscal 2026 earnings it delivered a pivotal strategic shift: the British chip designer is now selling its own silicon directly into the AI data center for the first time in its history.

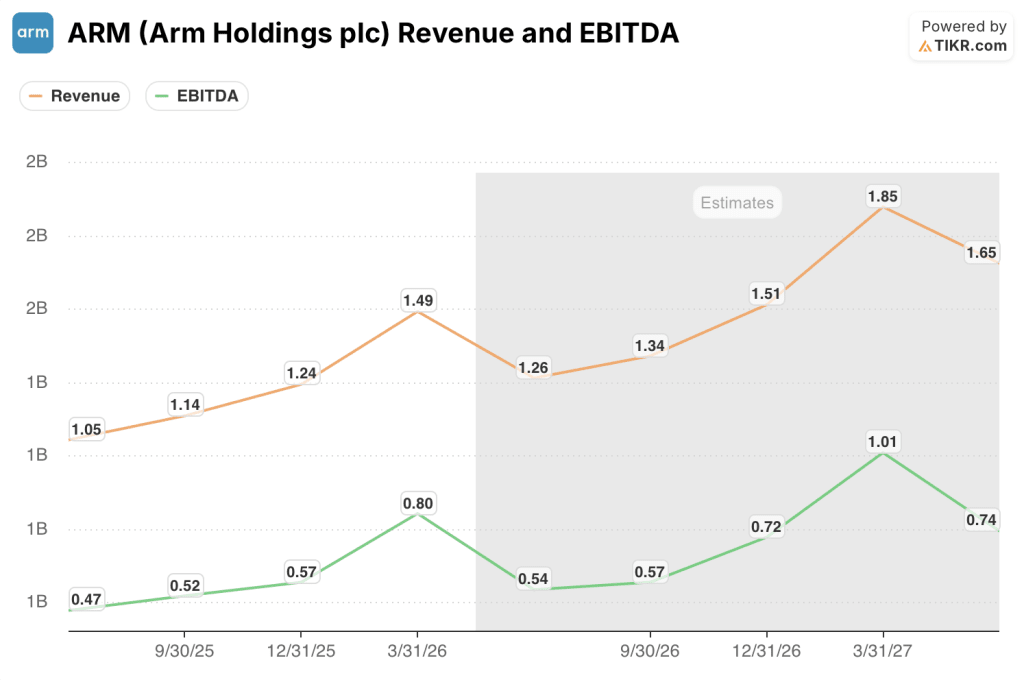

Full-year revenue hit a record $4.92 billion, up 23% year-over-year, the company’s third consecutive fiscal year of 20%-plus growth since its 2023 IPO.

The standout development was the Arm AGI CPU, a data center chip announced at the company’s March Arm Everywhere investor event and purpose-built for agentic AI workloads, with Meta as lead co-development partner and OpenAI, Cloudflare, SAP, and SK Telecom committed as customers.

By the time of the Q4 2026 earnings call, CEO Rene Haas disclosed that customer demand for the AGI CPU had exceeded $2 billion across fiscal 2027 and 2028, more than double the $1 billion figure stated at launch just six weeks earlier.

That demand acceleration matters because Arm’s thesis rests on a specific structural argument: as AI transitions from prompt-and-response to continuous agentic workloads, the number of CPU cores required per data center gigawatt grows roughly 4x, creating what Arm estimates as a $100 billion CPU TAM by 2030.

Q4 fiscal 2026 results corroborated the direction. Royalty revenue grew 11% year-over-year to $671 million, while licensing and other revenue rose 29% to $819 million, with data center royalty revenue more than doubling year-over-year for the period.

“We are very bullish about this data center demand,” Haas said in a Reuters interview following the earnings release, adding that the current quarter includes “a pretty healthy uptick in terms of royalties associated with the data center.”

Q1 fiscal 2027 guidance calls for revenue of around $1.26 billion, up roughly 20% year-over-year, with non-GAAP EPS of around $0.40, ahead of the Wall Street consensus estimate of $0.36 at the time of the print.

One new headwind entered the picture on May 15: Bloomberg News reported that the U.S. Federal Trade Commission has notified Arm of an antitrust investigation into its semiconductor licensing practices, examining whether the company is attempting to illegally monopolize portions of the chip market. Arm declined to comment on any investigation; the FTC did not respond to requests for comment.

Wall Street’s Take on ARM Stock

The investment thesis on Arm Holdings stock right now is not primarily about what the company earns today. It is about whether a royalty-and-licensing business that has compounded at 20%-plus for three consecutive years can layer a $15 billion silicon revenue stream on top of an IP business projected to double, without the transition disrupting the relationships that underwrite the entire royalty model.

That tension is visible in the consensus.

Revenue consensus for the quarter ending June 2026 sits at $1.26 billion, up 20% year-over-year, with the Street projecting 21.8% revenue growth for the December 2026 quarter and accelerating to almost 24% for the March 2027 quarter.

Meanwhile, the EBITDA picture supports the growth narrative. Consensus EBITDA for the June 2026 quarter is around $540 million, implying margins near 43%, then expanding to approximately $1.01 billion by March 2027 as operating leverage builds into the back half of the fiscal year.

The analyst table reflects a market that is mostly, but not unanimously, sold. As of May 15, 20 analysts rate Arm Holdings stock a Buy, 7 rate it Outperform, 10 Hold, 1 Underperform, and 2 Sell, across 36 estimates. The mean price target is $229, implying roughly 9% upside from the May 15 close of $209.16, while the high-end target of $326 reflects a small camp betting on full AGI CPU execution.

The compressed implied upside from the mean target tells the story of a stock the market has re-rated aggressively into the thesis. Arm Holdings stock traded at $109 at the end of December 2025 and is now above $209, a move driven almost entirely by the March AGI CPU announcement and the Q4 earnings confirmation of $2 billion in committed demand.

The debate inside analyst models centers on gross margin trajectory for the silicon business. CFO Jason Child said on the May 6 earnings call that first-generation AGI CPU gross margins are roughly 30%, well below the 98% non-GAAP gross margin Arm earns on its IP. At scale, the chip business is expected to approach approximately 35% operating margins by fiscal 2031, according to guidance provided at the Arm Everywhere event, while the IP business is targeted at around 65%. The blended picture only holds together if silicon revenue reaches the $15 billion target.

The bear argument is structural and straightforward: Arm is moving into direct competition with licensees who currently underwrite the royalty stream, and the FTC investigation, while early-stage, introduces a regulatory variable that has no resolution timeline.

The bull argument is equally straightforward: every major hyperscaler is already adopting Arm-based CPUs, data center royalties are doubling year-on-year with no sign of deceleration, and the AGI CPU fills a gap that customers have explicitly told management exists.

What Does the Valuation Model Say?

TIKR’s base case model prices Arm Holdings at around $1,175 per share realized by March 2031, anchored to a revenue CAGR of roughly 51% and a net income margin assumption of 44%, with the primary driver being AGI CPU silicon revenue reaching Arm’s stated $15 billion target alongside an IP business doubling to $10 billion.

At roughly 461% total potential return from the current price of $209 over approximately five years, the mid-case implies an IRR of around 42% annually, a figure that demands nearly flawless execution on both growth vectors simultaneously.

Against that backdrop, Arm Holdings stock appears fairly valued to moderately undervalued today: the current market price bakes in a serious probability of AGI CPU success, but prices it at a discount to the full mid-case, suggesting the Street still assigns meaningful probability to a miss.

The question is not whether Arm’s architecture dominates the AI data center. The evidence says it does. The question is how fast silicon revenue scales against a 30% gross margin structure while the FTC investigation and licensee relationships remain unresolved.

Base Case (AGI CPU Scales Toward Plan):

- TIKR’s mid-case model projects revenue growing at roughly 51% CAGR through fiscal 2031, reaching approximately $25 billion in total revenue across IP and silicon

- Data center royalty revenue is already more than doubling year-on-year, with Arm’s ~50% hyperscaler market share across AWS, Google, Microsoft, and NVIDIA providing a durable royalty floor beneath the silicon ramp

- $2 billion of committed AGI CPU demand across fiscal 2027 and 2028 locked before the first production revenue hits; Haas confirmed production on track for Q4 fiscal 2027

- Meta’s Prometheus cluster (targeting more than 1 gigawatt) and Hyperion (targeting 5 gigawatts) represent multi-year demand anchors for Arm AGI CPU as the primary orchestration CPU

- Management guided non-GAAP EPS of around $9 by fiscal 2031, against the current consensus of around $0.77 for fiscal 2027, implying more than 10x EPS growth in five years if the silicon business reaches scale

Downside Risk (Execution or Regulatory Disruption):

- FTC investigation into licensing practices introduces headline risk; if the agency requires licensing concessions, the royalty rate structure that drives base-case margins could compress materially

- First-generation AGI CPU gross margins near 30% mean the silicon business is dilutive to total company margins until it reaches significant scale; any revenue shortfall in fiscal 2027 or 2028 creates near-term EPS pressure

- Arm is supplying only $1 billion of the $2 billion demand backlog while supply chain capacity for the second billion remains unsecured; Haas acknowledged on the May 6 call that teams are “working around the clock” on wafer and memory sourcing

- Intel and AMD possess deep enterprise relationships and $10-plus billion R&D budgets; a successful competitive response to the AGI CPU in fiscal 2028 or 2029 could cap silicon market share below the $15 billion target

- At 165x fiscal 2027 consensus normalized EPS, a single guidance miss compresses the multiple before the silicon business is large enough to reanchor the valuation

Is Arm Holdings stock a buy right now?

Arm Holdings stock carries 20 Buy ratings, 7 Outperforms, 10 Holds, 1 Underperform, and 2 Sells from 36 analysts, with a mean price target of $229, implying roughly 9% upside from the May 15 close.

TIKR’s base case model projects a price target of around $1,175 by fiscal 2031, reflecting 51% revenue CAGR if AGI CPU revenue reaches $15 billion.

The key variable is whether the supply chain can service the more than $2 billion in committed customer demand on schedule.

What is the price target for ARM stock?

The Wall Street mean price target for ARM stock stands at $229 as of May 15, with a high-end target of $326 among 36 analyst estimates.

The Street low is $125. TIKR’s base-case model, built around AGI CPU revenue ramping to $15 billion and IP revenue doubling to $10 billion by fiscal 2031, implies a price target of around $1,175 per share over approximately five years, representing roughly 461% total potential return from current levels.

Should You Invest in Arm Holdings plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Arm Holdings stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arm Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ARM stock on TIKR for Free →