Key Stats for Energy Transfer Stock

- 52-Week Range: $16 to $21

- Current Price: $20

- Street Mean Target: $23

- Street High Target: $26

- Analysts Consensus: 13 Buys, 5 Outperforms, 3 Holds, and 1 No Opinion

- TIKR Model Target (Dec. 2030): $28

Energy Transfer Raises Full-Year EBITDA Guidance by $750 Million After a Record-Breaking Q1

Energy Transfer LP (ET) is one of the largest midstream energy infrastructure companies in the United States, operating pipelines, processing plants, fractionation facilities, and export terminals across more than 40 states, and following Q1 2026 earnings reported May 5, the partnership delivered adjusted EBITDA of approximately $4.9 billion, up from approximately $4.1 billion in Q1 2025.

That $4.9 billion quarter was not built on commodity luck alone.

Energy Transfer posted record midstream gathering volumes, record NGL fractionation volumes, record NGL export volumes, and record crude oil transportation volumes simultaneously in a single quarter — a breadth of operational outperformance that is difficult to manufacture and harder to dismiss.

The headline number that moved guidance came directly from management: the partnership beat its internal plan by approximately $500 million in Q1 and captured its full-year optimization target in a single quarter, which forced a meaningful upward revision to full-year 2026 EBITDA guidance to a range of approximately $18.2 billion to $18.6 billion, up from the prior range of approximately $17.45 billion to $17.85 billion.

Co-CEO Tom Long was direct on the Q1 2026 call: “We are optimistic that some of the benefits we saw in the first quarter will carry over throughout the rest of the year, putting us in a position to achieve or exceed the high end of our guidance range.”

The NGL and refined products segment drove the single largest upside, posting approximately $1.2 billion in adjusted EBITDA versus approximately $978 million a year earlier, with record performance at Mont Belvieu fractionators and record export volumes from the Nederland terminal contributing alongside a $50 million lift from new chilling capacity placed into service in 2025.

Beyond the quarter, Energy Transfer stock is positioned at the center of a structural demand shift that management spent considerable time articulating: rising global demand for U.S.-sourced LNG, NGLs, and crude oil accelerated by Middle East conflict dynamics, with COO Mackie McCrea noting that “there’s a very clear redirection to the U.S. for all products.”

The project backlog supporting that positioning is substantial: the Hugh Brinson Pipeline (Phase 1 expected in service Q4 2026), the Desert Southwest Pipeline (targeting Q4 2029 service), two new Florida Gas Transmission expansion projects backed by 15- to 25-year agreements, new natural gas supply agreements to serve power plants and data centers in Oklahoma, Arkansas, and Texas, and the Springerville Lateral off the Transwestern Pipeline, a $600 million, 20-year-backed project targeting Q4 2029 service.

Wall Street’s Take on ET Stock

The central question Energy Transfer stock forces investors to answer is whether the Q1 outperformance represents a durable step-up in earning power or a favorable quarter inflated by optimization gains that will mean-revert.

The data leans clearly toward durability.

Of the approximately $500 million beat versus internal plan, management identified roughly $300 million as one-time in character — but then immediately noted that in 5 of the last 8 years, Energy Transfer has generated large optimization and spread-capture benefits that exceeded its base business plan, making “one-time” a label that requires scrutiny when applied to this specific partnership.

The EBITDA consensus reflects growing Street conviction: Energy Transfer’s consensus EBITDA estimate for the June 2026 quarter stands at approximately $4.45 billion, with the September 2026 quarter at approximately $4.47 billion, implying roughly 15% YoY growth in each period as the volume ramp from new projects compounds on top of a strengthened base business.

Revenue growth confirms the scale of the underlying commercial acceleration: Energy Transfer posted $27,771 million in Q1 2026 revenue against a Street estimate of $27,297.88 million, a 1.73% beat on the top line, with revenue up 32.12% year over year from Q1 2025’s $21,020 million.

With 13 Buy ratings, 5 Outperforms, and only 3 Holds across 22 analysts as of May 15, the consensus skew is decisively bullish: the mean price target of $23.32 implies around 16% upside from the current price of $20.15, with the street high at $26.00.

The Mispricing: with Energy Transfer EBITDA estimated to grow around 15% year over year through mid-2026 while the unit price sits roughly 2.5% below its 52-week high of $20.67, Energy Transfer stock appears undervalued relative to the forward earnings trajectory — a partnership delivering record operational performance trading at what the Street’s 22-analyst consensus prices as a double-digit upside situation.

The specific catalyst to watch is Hugh Brinson Phase 1: management indicated gas could begin flowing as early as Q3 2026 ahead of the formal Phase 1 in-service date, and once the 1.5 Bcf per day pipeline is fully operational, it becomes what Long described as “a major U.S. header system” with significant backhaul volume upside layered on top of existing contracted flows.

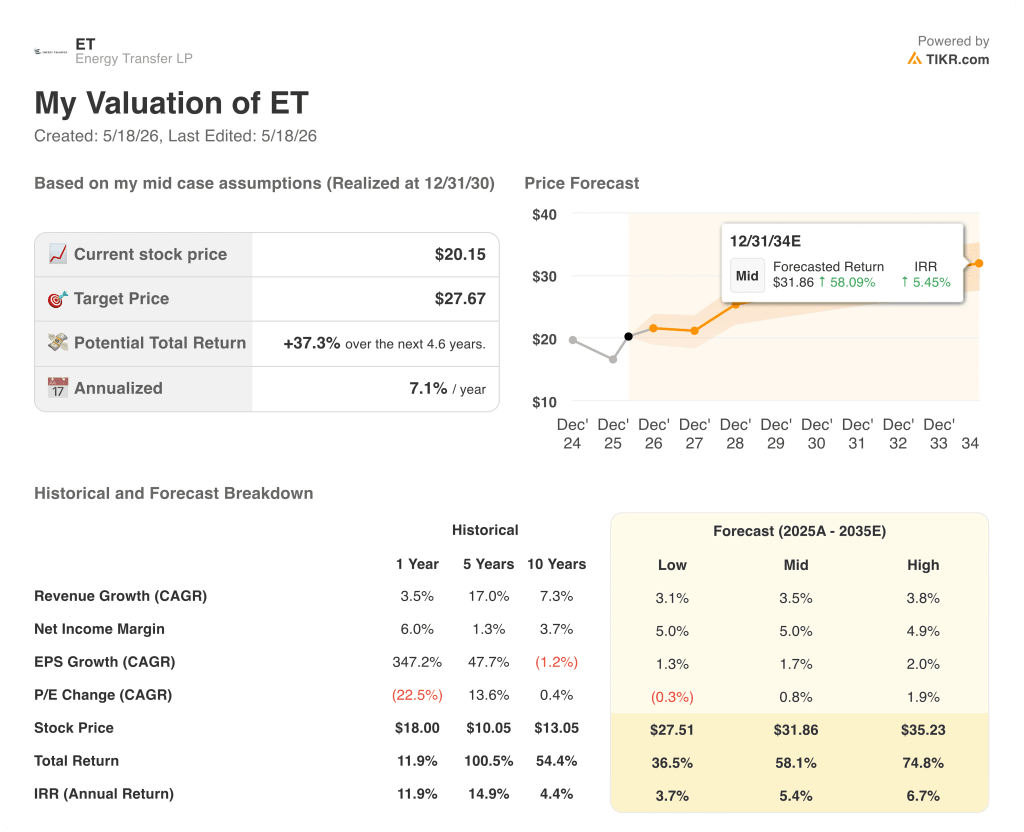

What Does the Valuation Model Say?

TIKR’s base case values Energy Transfer at $27.67 per unit, assuming a revenue CAGR of around 3.5% through 2030 alongside a sustained net income margin of 5%, inputs anchored to the partnership’s expanding project backlog and the multi-year data center and power generation demand cycle now fully underway.

At $20 against a TIKR mid-case target of $28 and a full return scenario (including distributions) of around 58% through December 2034, Energy Transfer stock appears undervalued at a unit price that has not yet reflected the compounding effect of four new long-term contracted pipeline projects coming into service between Q4 2026 and Q4 2029.

The argument hinges on execution across a heavily front-loaded capital program: Energy Transfer raised 2026 organic growth CapEx guidance to approximately $5.5 billion to $5.9 billion, excluding SUN and USAC, and the returns on that spend — mid-teen targeted IRRs on long-term contracted assets — only materialize if projects arrive on time and fully ramped.

Bull Case (What Has to Continue Going Right)

- Hugh Brinson Phase 1 delivers first gas in Q3 2026 ahead of schedule, adding contracted 1.5 Bcf per day and unlocking significant backhaul volume upside that management described as still growing.

- NGL export expansion at Nederland proceeds to FID within months, extending the ethane contract book to 2041 and adding capacity to capture elevated international LPG spreads.

- Data center and power generation contracts in Oklahoma, Texas, and Arkansas (currently totaling around 300 million cubic feet per day of new supply connections) continue to add volume without meaningful incremental capital, given ET’s existing intrastate footprint.

- Permian Basin processing expansion (Mustang Draw I commissioning May 2026, Mustang Draw II targeting Q4 2026) adds 550 MMcf per day of combined throughput capacity into a basin where bottlenecks are expected to clear by early 2027.

- Full-year 2026 EBITDA reaches or exceeds the high end of the $18.2 billion to $18.6 billion guidance range as Middle East-driven demand elevation proves more persistent than the conservative base-case price deck assumes.

Bear Case (What Could Go Wrong)

- Approximately $300 million of Q1’s $500 million beat does not repeat in subsequent quarters, creating a difficult YoY comparison in Q1 2027 and a potential guidance reset if commodity spreads normalize faster than management expects.

- Capital intensity rises further: at $5.5 billion to $5.9 billion in 2026 growth CapEx already above the prior $5 billion to $5.5 billion range, any additional project additions or cost overruns would pressure distributable cash flow coverage, particularly given the leverage target of 4x to 4.5x EBITDA.

- NGL pipeline recontracting becomes more competitive as new capacity announced by competitors enters service over the next 12 to 24 months, compressing volume and rate assumptions in the NGL segment beyond the current base case.

- Desert Southwest regulatory timeline (FERC certificate application filing targeted Q4 2026, in-service Q4 2029) slips, delaying one of the partnership’s most significant long-duration growth assets and pushing EBITDA contribution further into the forecast horizon.

Is Energy Transfer stock a buy right now?

With 13 Buy ratings and 5 Outperform ratings across 22 analysts, the Street’s answer is a clear yes.

The mean price target of around $23 implies around 16% upside from $20, and TIKR’s mid-case values ET at $28, implying total returns of around 58% through 2034 including distributions.

The key variable is Hugh Brinson Phase 1 delivery: if gas flows begin in Q3 2026 as management indicated, the earnings ramp compresses that upside window meaningfully.

Should You Invest in Energy Transfer LP?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Energy Transfer LP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Energy Transfer LP alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ET stock on TIKR for Free →