Key Stats for Carvana Stock

- 52-Week Range: $54 to $97

- Current Price: $67

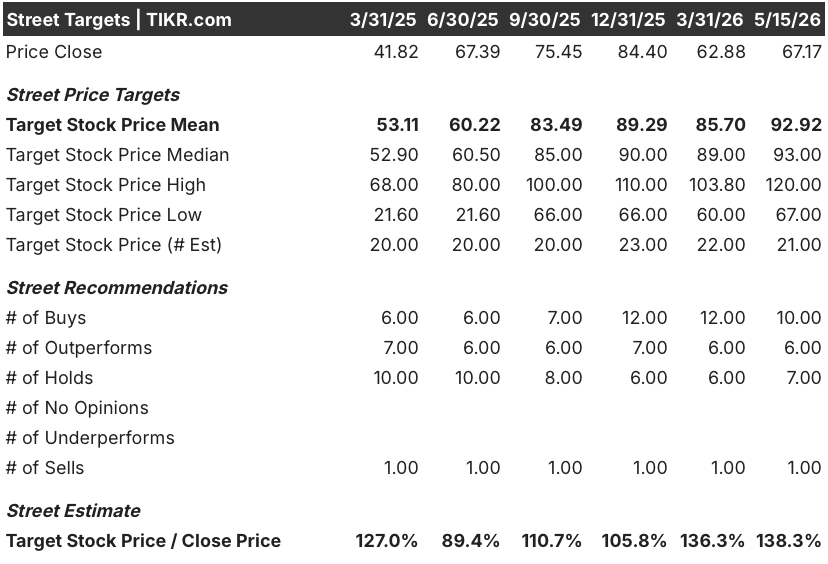

- Street Mean Target: $93

- Street High Target: $120

- Analyst Consensus: 10 Buys / 6 Outperforms / 7 Holds / 0 Underperforms / 1 Sell

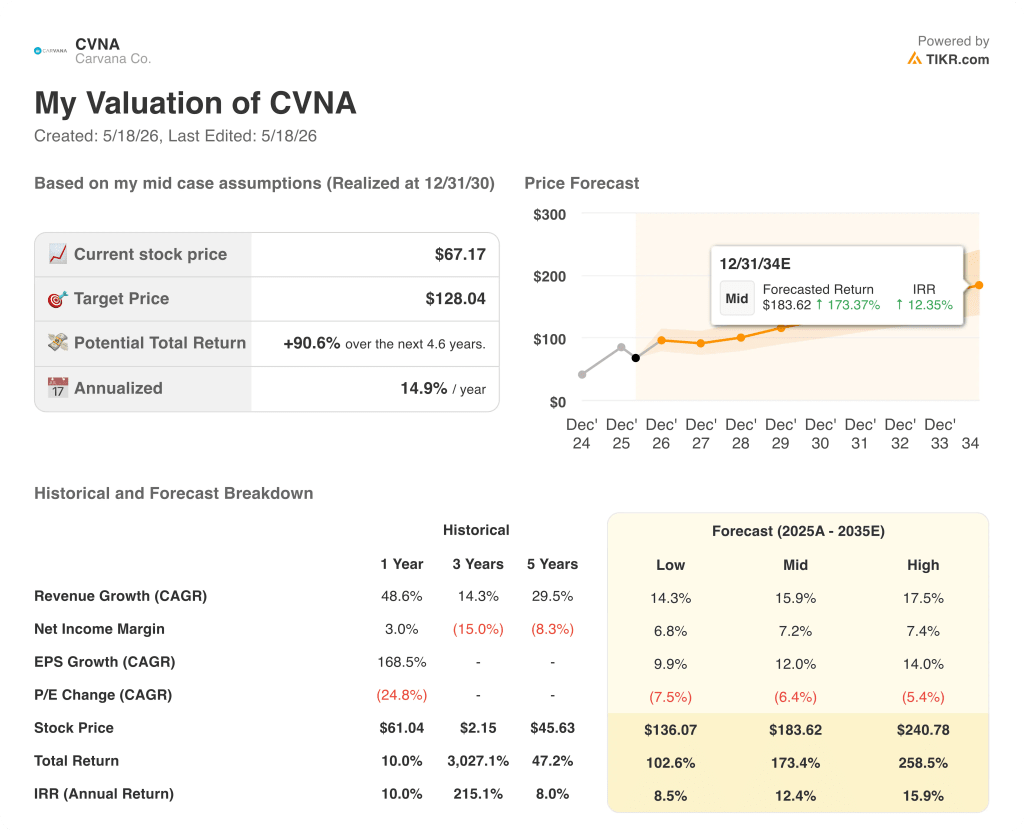

- TIKR Model Target (Dec. 2030): $128

Carvana Closes Q1 With a Sixth Straight 40% Growth Quarter as the Recon Team Fixes Its One Stumble

Carvana Co. (CVNA), the online used-car retailer best known for its tower-sized vehicle vending machines, delivered a sixth consecutive quarter of at least 40% year-over-year retail unit growth after Q1 2026 earnings on April 29.

The headline number was 187,393 retail units sold, a 40% increase from the year-ago period and a new company record.

Revenue climbed 52% to $6.43 billion, topping the consensus estimate of $6.08 billion by more than $350 million.

Adjusted EBITDA reached $672 million, also a new record, beating the $648.86 million consensus, with adjusted EBITDA margin at 10.4%.

Net income came in at $405 million, up from $373 million in Q1 2025, despite a $42 million headwind from changes in fair value of warrants.

The one operational story the quarter demanded was reconditioning: Carvana had flagged elevated recon costs in Q4 2025, and Q1 confirmed the team had corrected course, with CEO Ernie Garcia noting on the earnings call, “So far in April, we are operating just shy of our all-time best in labor efficiency throughout the network.”

Garcia was direct about what drove the fix: new AI-integrated planning tools that help managers optimize staffing across production lines, built and deployed in weeks by a product team that spent time on the floor at facilities with the steepest performance gaps.

For Q2, Carvana guided for sequential records in both retail units sold and adjusted EBITDA, assuming a stable operating environment.

The 5-for-1 stock split approved at the May 5 annual meeting took effect May 8, resetting the share price to a more accessible level while leaving the underlying business thesis unchanged.

Wall Street’s Take on CVNA Stock

The thesis on Carvana stock entering Q1 was simple: the company had demonstrated it could grow at 40% while generating meaningful EBITDA, but a stumble in reconditioning efficiency during Q4 2025 gave bears a foothold, with the concern being that scaling at this speed was producing operational slippage that could erode the margin story.

Q1 answered that directly.

Revenue grew 52% year-over-year to $6.43 billion against a consensus of $6.08 billion, and adjusted EBITDA grew 37.7% to $672 million against a consensus of $648.86 million, making the case that the Q4 recon issue was a correctable operational bump rather than a structural flaw in the model.

The Street responded with conviction: 17 of 26 analysts rate CVNA a buy or strong buy, 8 rate it hold, and 1 recommends sell, with a Wall Street mean price target of around $93 at current levels, implying around 38% upside from the May 15 close of $67.

Looking forward, consensus projects Q2 2026 revenue of around $6.84 billion, a 41% year-over-year increase, and full-year 2026 EBITDA expected to grow around 27% to $760 million for Q2 alone.

The bull case is built on three compounding drivers: a structurally supportive used-car demand environment where average new vehicle prices hover near $50,000, a vertically integrated model whose economics improve at scale, and a long-stated target of 3 million cars per year at 13.5% adjusted EBITDA margin by 2030 to 2035 that becomes more credible each time a 40% growth quarter lands.

The bear case centers on the gross profit per unit trajectory: non-GAAP retail GPU declined year-over-year in Q1 due to higher reconditioning costs and lower shipping fees, and management guided for further year-over-year GPU pressure in Q2 from roughly $100 to $200 of impact from narrower industry-wide wholesale-to-retail spreads.

Garcia addressed the spread compression directly on the call, characterizing it as transitory: “The wholesale market is ahead of the retail market, and so that led to the call out.”

What Does the Valuation Model Say?

TIKR’s base case values Carvana at $128 per share by December 2030, anchored to a revenue CAGR of around 16% from 2025 through 2035 and a net income margin assumption of 7%, consistent with the company’s own long-term framework of scaling toward 13.5% adjusted EBITDA margins as fixed costs lever against a growing unit base.

At $67 against a TIKR mid-case target of $128, with a near 91% total return potential and an annualized IRR of around 15%, Carvana stock is undervalued relative to the growth and margin trajectory the model prices in.

The central tension is not whether Carvana can grow: it is whether the path to 13.5% adjusted EBITDA margin runs through one more year of GPU headwinds or whether the recon fix accelerates the timeline.

Bull Case

- Six consecutive 40% unit growth quarters, with Q2 guided to a new sequential record, establishing a baseline that makes the 3 million car per year target structurally credible

- TIKR’s high case values CVNA at around $241 per share through 2035, implying around 259% total return from current levels, on a revenue CAGR of around 17.5% and net income margins of 7.4%

- Recon labor efficiency is back to the company’s all-time best as of April, with new centralized planning tools rolling out across the facility network over the coming months

- ADESA Clear, the company’s digital wholesale auction platform, is now operating at what management described as “best-in-class” quality, creating a sourcing advantage that compounds as the retail base scales

- Annualized IRR of around 16% in the high case, against a current price that already reflects a 31% discount to the 52-week high of $97.38

Bear Case

- Non-GAAP retail GPU declined year-over-year in Q1, and management guided Q2 GPU down an additional $100 to $200 from narrower wholesale-to-retail spreads, putting near-term margin pressure on a business where GPU is the primary lever to 13.5% adjusted EBITDA margins

- TIKR’s low case values CVNA at around $136 per share, implying around 103% total return but an annualized IRR of around 8.5%, meaningfully below the hurdle rate for some investors

- The 5-year historical net income margin has averaged negative 8.3%, meaning the transition to sustained profitability at 7.2% net margins in the mid case is a forecast, not a demonstrated track record

- A single bear analyst remains in coverage, and BofA downgraded CVNA to neutral in April citing macro risks to the lower- and middle-income consumer from elevated gas prices and tighter credit conditions

- Insider selling has been consistent across the CFO, COO, and VP of Accounting through April and May 2026, which does not invalidate the thesis but is worth monitoring for pattern changes

Is Carvana stock undervalued right now?

TIKR’s base case values Carvana at $128 per share, implying around 91% total return from the current price of $67.17 and an annualized IRR of around 15%.

With 16 analysts rating CVNA a buy or outperform and a Wall Street mean target of around $93, consensus supports that view.

The key variable is GPU: if wholesale-to-retail spreads normalize as management expects, the Q2 beat likely lifts targets further.

What do analysts say about CVNA stock?

As of May 15, 2026, 10 analysts rate CVNA a buy, 6 rate it outperform, 7 rate it hold, and 1 recommends sell, with a Wall Street mean target of around $93. Implied upside from the current price of $67 is approximately 38%.

The post-Q1 cluster of target hikes from BTIG and J.P. Morgan reflects growing conviction that the Q4 reconditioning stumble was a one-quarter event, not a structural problem.

What is the outlook for CVNA stock in 2026?

Carvana guided Q2 2026 for sequential records in both retail units sold and adjusted EBITDA, extending six straight quarters of at least 40% unit growth. Consensus projects full-year 2026 revenue approaching $27 billion.

The primary variable is whether wholesale-to-retail spread compression, which management flagged as a $100 to $200 GPU headwind for Q2, proves transitory as Garcia indicated, or persists into the second half.

Should You Invest in Carvana Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Carvana Co. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carvana Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CVNA stock on TIKR for Free →