Key Stats for Alphabet Stock

- Current Price: $396.78

- Target Price (Mid): ~$616

- Street Target: ~$428

- Potential Total Return: ~55%

- Annualized IRR: ~10% / year

- Earnings Reaction: +9.96% (April 30, 2026)

- Max Drawdown: (20.42%) (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet Inc. (GOOGL) jumped 9.96% on April 30 after a Q1 2026 report that confirmed the AI spending is paying off. But investors who stopped paying attention after the earnings call missed an equally important conversation.

On May 14, YouTube CEO Neal Mohan appeared at MoffettNathanson’s Media, Internet & Communications Conference and walked Wall Street through how a $60 billion platform plans to grow further. He covered subscription strategy, Shorts monetization, living room dominance, and AI tooling, none of which appeared in the earnings release. Alphabet’s investor relations materials cover the financials. What Mohan added at MoffettNathanson was the product roadmap behind them.

The Subscription Flywheel Is Moving Faster Than the Revenue Line Suggests

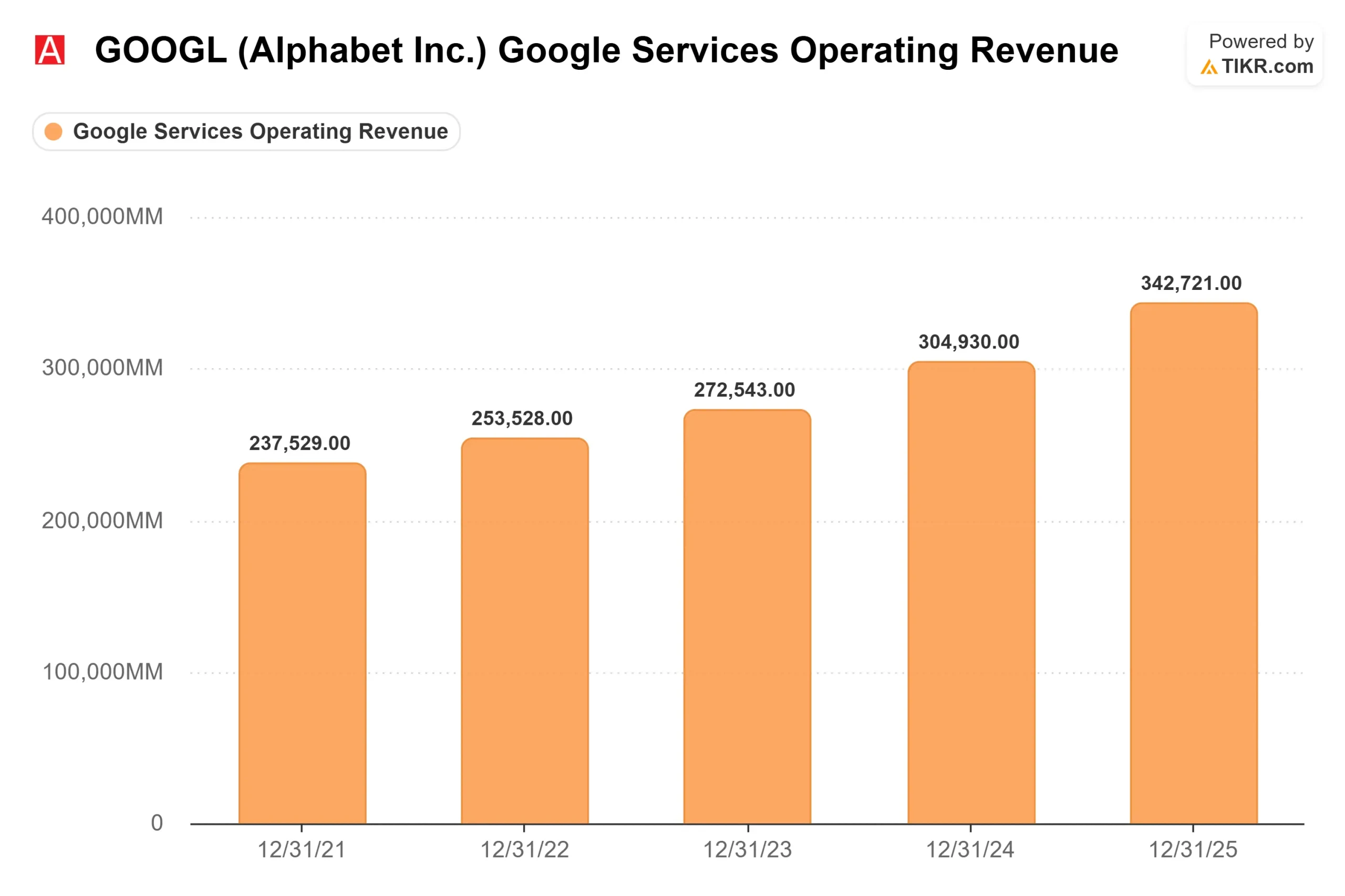

YouTube crossed $60 billion in combined advertising and subscription revenue for full-year 2025, per Alphabet’s Q4 2025 earnings release, the first time the company disclosed the platform’s total revenue as a standalone figure. That put YouTube ahead of Netflix, which reported $45.18 billion for the same period.

The more important detail is the mix. One-third of YouTube’s revenue now comes from subscriptions, including YouTube Premium, YouTube Music, and YouTube TV. That slice is growing at roughly twice the pace of advertising, per Mohan’s conference remarks.

“YouTube Music and Premium has, as of last year, over 125 million subscribers,” Mohan said. “This last quarter was when we added the most non-trial subscribers ever in the history of Premium globally, but also in the U.S.” Total paid subscriptions across YouTube and Google One reached 350 million by Q1 2026, up from 325 million at year-end, per Alphabet’s Q1 2026 earnings release.

Two levers are driving that. First, tiering: YouTube TV launched 10 genre-specific plans, and YouTube Premium added a lower-cost Premium Lite option. Mohan called both moves “TAM expanding,” designed to bring in subscribers who wouldn’t pay the flagship price, not cannibalize existing ones. Second, pricing: YouTube raised U.S. Premium pricing for the first time in three years in May 2026. Despite the increase, Q1 was the strongest subscriber quarter on record. Both levers running simultaneously is the flywheel working as designed.

See historical and forward estimates for Alphabet stock (It’s free!) >>>

Living Room and Shorts Change the Ad Math

YouTube’s advertising revenue grew 11% to $9.9 billion in Q1 2026, per Alphabet’s Q1 release. The structural ad story runs deeper than the quarterly rate.

More than 50% of YouTube’s U.S. watch time now happens on TV screens, with 200 million hours watched in the U.S. living room daily, per Mohan. Connected TV commands higher ad rates than mobile, and YouTube’s living room penetration gives it pricing power that purely mobile-first platforms cannot match.

Shorts is the second structural shift. Mohan confirmed that Shorts has reached revenue-per-watch-hour parity with long-form YouTube in the U.S. and several other markets, and has exceeded parity in some. Because Shorts previously monetized at a discount, rapid Shorts growth diluted YouTube’s blended revenue per view. Parity removes that drag. Over 500,000 creators have tagged their videos with product links, turning Shorts into a shopping conversion channel on top of its ad contribution, per Mohan.

Mohan also described YouTube’s full-funnel advantage directly. He cited a Coach campaign that drove a 60% increase in brand awareness and a 6x lift in purchase consideration, simultaneously an outcome neither pure performance networks nor traditional linear TV can deliver alone.

The Creator Moat Nobody Models

The most durable competitive advantage Mohan described is economic, not technological.

“In the last 4 years, up to last year, we paid out over $100 billion to the creator economy,” Mohan said. “We have 3 million creators in our YouTube Partner Program that monetize every single day.” A creator earning a full income on YouTube has no rational reason to rebuild their audience elsewhere, even if a competitor offers a short-term payout incentive.

Non-endemic creators, athletes, celebrities, and traditional media figures are now migrating toward YouTube rather than away from it. At the same time, YouTubers are expanding off-platform using the audience YouTube built for them. Mohan cited MrBeast’s stated “YouTube first” rule as the operating principle behind that dynamic. The platform that pays creators best and distributes their content most widely retains them. YouTube currently does both.

This is the structural difference from Netflix, which pays for every hour of content it serves. YouTube’s content costs are distributed across 3 million monetizing partners who create voluntarily.

AI Is Already in the Product

YouTube’s AI integration is visible in current metrics, not future promises.

Mohan cited the Ask feature, a Gemini-powered interface that lets viewers interact directly with video content below the player. “Just in April, that had 75 million users using it on a regular basis,” he said. AI dubbing, AI-powered creation tools, and Ask Studio, which gives creators natural-language access to channel analytics, are all live. The timing adds a near-term catalyst. Google I/O, Alphabet’s annual developer conference, runs May 19 and 20. Google pre-announced the Googlebook laptop on May 12 ahead of the event, signaling a heavy Gemini focus. Mohan noted YouTube works “very closely with DeepMind on a daily basis,” meaning platform-level AI upgrades tend to arrive faster than they do at competitors.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $396.78

- Target Price (Mid): ~$616

- Potential Total Return: ~55%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

The TIKR mid-case model uses around 15% revenue CAGR through 12/31/30 and a net income margin of around 34%, arriving at a target of around $616. The two revenue drivers are Google Cloud, where Alphabet’s reported $460-plus billion backlog per its Q1 2026 earnings release provides a compounding revenue base, and Google Services, where subscription mix shift and Shorts parity expand revenue per viewer without proportional content cost increases. The margin driver is operating leverage: Google Cloud’s operating income grew from losses in 2022 to $13.9 billion in 2025, per TIKR’s Segments data, and further expansion is expected as infrastructure utilization rises.

The Street is more conservative. The mean analyst price target is $427.89 per TIKR’s Street Targets data, implying around 8% upside from current levels. Of the analysts tracked by TIKR, 44 rate GOOGL a Buy and 13 Outperform, with none issuing a Sell.

On valuation multiples, GOOGL trades at 19.77x NTM EV/EBITDA and 31.65x NTM P/E per TIKR. Among Interactive Media and Services peers on TIKR’s Competitors page, Reddit (RDDT) trades at 18.18x NTM EV/EBITDA and Pinterest (PINS) at 7.55x NTM EV/EBITDA, both at fractions of Alphabet’s scale and margin profile. The premium is warranted; whether it expands depends on execution.

The primary risk is regulatory. The DOJ’s ongoing antitrust proceedings around Google’s advertising technology remain unresolved. A forced divestiture of AdX Alphabet’s digital advertising marketplace would remove material revenue from the model’s base. Free cash flow also compresses sharply in 2026 per TIKR’s forward estimates before recovering as infrastructure matures, which is a timing risk, not a structural one.

Conclusion

The bull case on GOOGL no longer needs defending after Q1 2026. What Mohan’s MoffettNathanson session added is the forward layer: subscriptions tiering at both ends of the price spectrum, Shorts reaching monetization parity with long-form, and AI tooling already generating 75 million monthly users on a single feature.

The next checkpoint is Q2 2026 earnings, expected in late July. Management flagged that Cloud revenue would have been higher if Alphabet could meet demand. If Cloud holds above 50% growth in Q2, the capex-compression bear case loses its main justification. If it decelerates materially, the question of whether $180 to $190 billion in annual capex is ahead of demand becomes the trade. That number Cloud’s Q2 growth rate is the one to watch.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!