Key Stats for Amgen Stock

- 52-Week Range: $268 to $391

- Current Price: $326

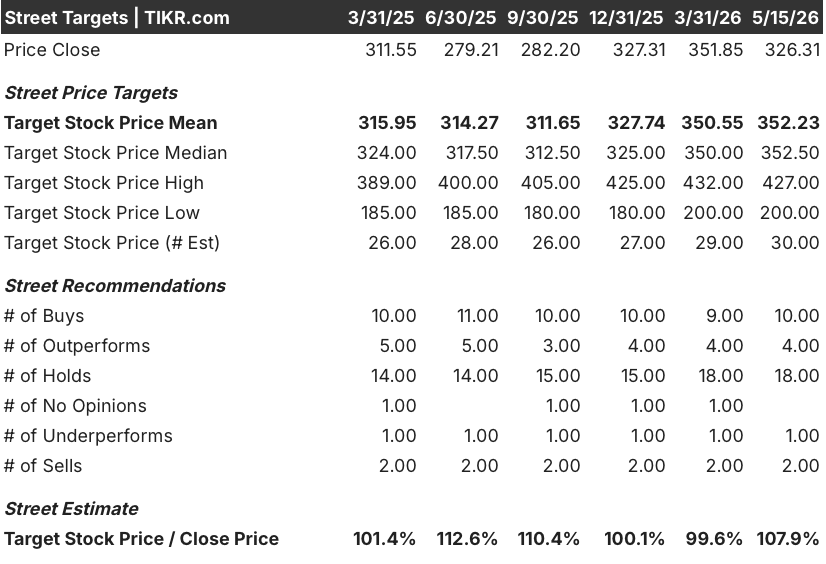

- Street Mean Target: $352

- Street High Target: $427

- Analyst Consensus: 10 Buys / 4 Outperforms / 18 Holds / 1 Underperform / 2 Sells

- TIKR Model Target (Dec. 2030): $462

Amgen Beats Q1 Estimates but Tavneos Fallout and a $10.7 Billion IRS Cloud Keep Investors on Edge

Amgen Inc. (AMGN) is one of the world’s largest biotechnology companies, generating over $37 billion in annual revenue by selling treatments for cardiovascular disease, rare autoimmune conditions, bone loss, and cancer, and following Q1 2026 earnings reported April 30, the stock faces a sharp tension between genuine operational strength and two compounding overhangs that the market has not yet resolved.

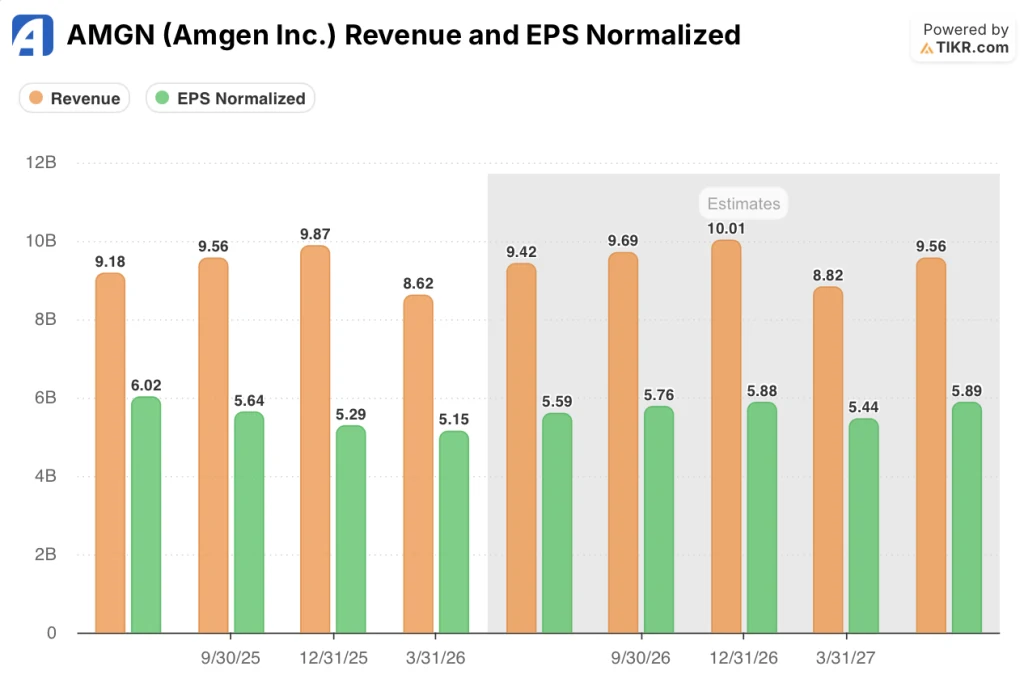

Q1 revenue rose 6% year-over-year to $8.6 billion, matching consensus, while adjusted EPS climbed 5% to $5.15, beating the $4.76 analyst estimate by a meaningful margin.

The growth came from the right places: Repatha, the cholesterol drug anchoring Amgen’s cardiovascular franchise, surged 34% to $876 million, driven by guidelines updates that now recommend earlier PCSK9 intervention and new-to-brand prescriptions up 44% year-over-year in the quarter.

Rare disease was equally strong, with the portfolio growing 25% to $1.2 billion; UPLIZNA, which treats neuromyelitis optica and generalized myasthenia gravis, grew 188% year-over-year to $262 million as the company expanded into new indications.

The cleaner story was interrupted by two developments that hit AMGN stock hard in the days around earnings.

The FDA proposed withdrawing approval of Tavneos, Amgen’s ANCA-associated vasculitis drug, citing a lack of proven effectiveness and alleged false statements in the original application; Amgen declined to pull the drug voluntarily, and the dispute now moves toward formal proceedings, creating an unresolved regulatory liability around a drug generating $119 million per quarter and growing 32% year-over-year.

Separately, Amgen disclosed on its earnings call that the IRS issued a draft notice of proposed adjustment for tax years 2016 to 2018, asserting significant profit allocation adjustments related to its Puerto Rico operations, similar in structure to the existing 2010 to 2015 dispute where a potential $10.7 billion liability remains unresolved pending a tax court ruling expected no earlier than the second half of 2026.

CEO Robert Bradway addressed the matter directly in Q1 2026 earnings call and describied the IRS position as without merit and noting that Amgen has invested nearly $2 billion in its U.S. manufacturing network over the past year, including $950 million in Puerto Rico alone, specifically to demonstrate the operational substance of those facilities.

Against that backdrop, Amgen raised its full-year 2026 revenue guidance to $37.1 billion to $38.5 billion and non-GAAP EPS guidance to $21.70 to $23.10, reflecting confidence that its six key growth drivers, which together delivered 24% aggregate growth and generated 70% of product sales in Q1, can absorb the continued erosion of legacy products losing patent exclusivity.

Wall Street’s Take on AMGN Stock

The central question Wall Street is working through right now is not whether Amgen’s core business is growing — it clearly is — but whether two compounding liabilities, the Tavneos regulatory dispute and the IRS tax litigation, represent manageable friction or structural damage to the thesis.

Consensus projects Amgen revenue of around $9.42 billion for Q2 2026, growing roughly 3% year-over-year, and full-year 2026 revenue of around $38 billion, consistent with guidance; the deceleration from Q1’s 6% growth rate reflects the accelerating biosimilar competition hitting Prolia and XGEVA, which together fell 32% to $1.1 billion in Q1, directly offsetting gains elsewhere.

Additionally, consensus EPS estimates climb from Q1’s $5.15 actual to $5.59 in Q2 2026, $5.76 in Q3, and $5.88 in Q4, a steady recovery that reflects the growth drivers outpacing legacy erosion as the year progresses.

30 analysts cover AMGN stock, with a breakdown of 10 Buys, 4 Outperforms, 18 Holds, 1 Underperform, and 2 Sells; the mean price target of $352 implies around 8% upside from the current price of $326.31, and the 18 Holds reflect a Street that sees the business as sound but views the IRS overhang as a reason to wait rather than act.

Raymond James analyst Christopher Raymond was explicit on the IRS risk on May 2, noting that if Amgen loses the 2010 to 2015 tax court case or settles, a second multibillion-dollar liability for 2016 to 2018 would likely follow, and that any payout at scale could materially reduce the company’s capacity for acquisitions and business development.

The bull case on the Street runs through MariTide, Amgen’s monthly or less-frequent GLP-1/GIP antagonist in Phase 3 development for obesity, where management disclosed new switch studies evaluating transitions from weekly semaglutide and tirzepatide to every-8-week or quarterly MariTide dosing; the enrolling Phase 3 trials are running ahead of expectations, and the CFO put the frequency contrast simply at the BofA Healthcare Conference: “Think 52, 12, 6, 4 — which one of those do you want if you’re getting poked?”

The bear case is straightforward: at 14.39x NTM P/E, Amgen stock is approximately in line with its historical mean of 14.17x, and if the IRS prevails in either or both tax disputes, the resulting cash drain could compress dividends, halt buybacks, and limit the business development that many bulls are implicitly pricing into the long-term thesis.

Priced at 14.39x forward earnings versus a historical mean of 14.17x, with EPS expected to grow around 5% while two open-ended legal liabilities threaten the balance sheet, Amgen stock appears fairly valued: the earnings multiple is not pricing in either a worst-case tax outcome or full MariTide success, leaving the stock appropriately calibrated to wait for resolution on both.

Amgen’s Q1 Income Statement Shows Operating Leverage Running Hot

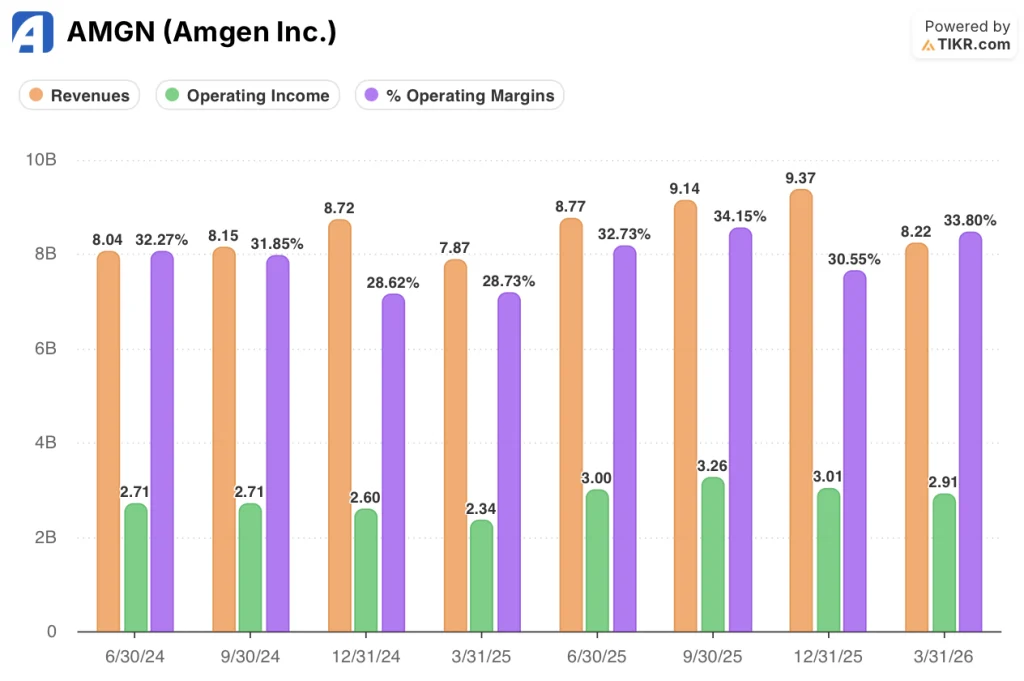

Amgen’s Q1 2026 product revenue of $8.22 billion grew 5.8% year-over-year, and operating income grew 24.4% year-over-year to $2.91 billion, expanding operating margins to 33.8% from the prior-year quarter, as revenue growth in the high-single digits absorbed a smaller proportional increase in operating expenses despite a 16% year-over-year rise in non-GAAP R&D spending.

The margin expansion is largely driven by the revenue mix shift toward higher-margin specialty products: Repatha at $876 million, EVENITY at $562 million, TEZSPIRE at $343 million, and TEPEZZA at $490 million collectively carry better economics than the Prolia and XGEVA base that is eroding.

The trajectory over the past eight quarters shows consistency in that operating margins have ranged between 28.6% and 34.2%, with the current quarter’s 33.8% sitting near the high end of that band, suggesting Amgen is executing the patent cliff transition without sacrificing profitability.

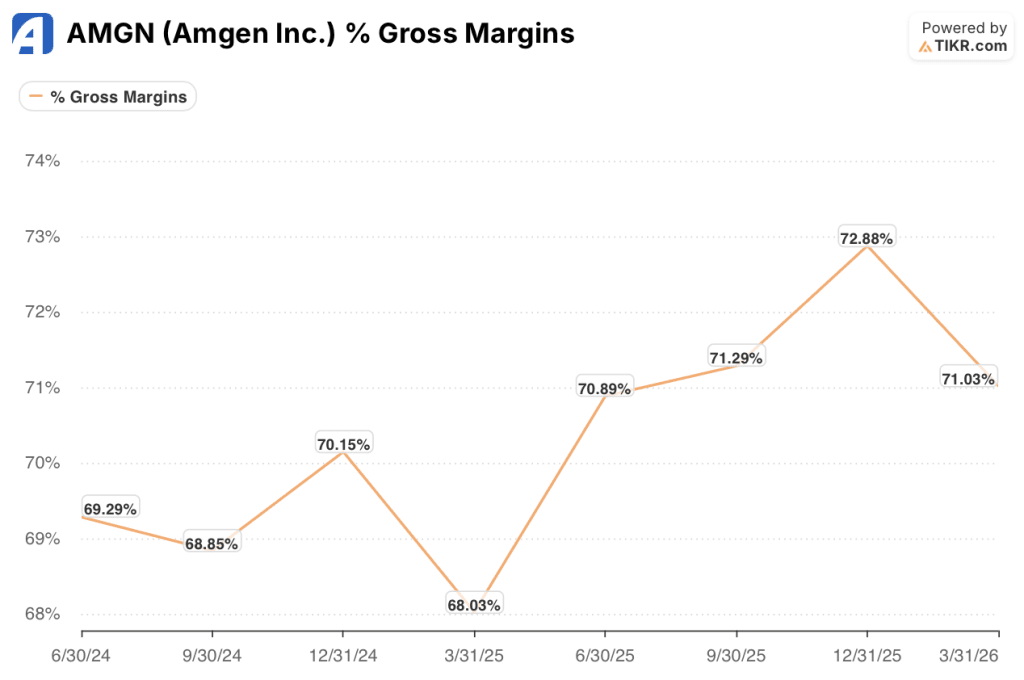

The one income statement tension worth naming: gross margins of 71% in Q1 2026 remain robust, but CFO Peter Griffith specifically flagged that higher profit share and royalty expenses, plus sales mix changes, will continue to weigh on cost of sales in future quarters, creating a ceiling on how far gross margin can expand even as product mix improves.

What Does the Valuation Model Say?

TIKR’s base case values Amgen at $462 per share by December 2030, anchored to mid-case assumptions of around 3% revenue CAGR, a 34.6% net income margin, and around 4% EPS CAGR through 2035, with a slight P/E compression of around 0.8% annually reflecting the market’s skepticism toward a business still navigating two open-ended legal liabilities.

At 14.39x NTM P/E against a historical mean of 14.17x with around 5% consensus EPS growth on the horizon, Amgen stock is fairly valued: the current multiple is effectively pricing in steady-state execution without a resolution catalyst in either direction, which is precisely where the risk/reward sits today.

The argument for this stock hinges on one question: does MariTide get to market and at what scale?

Base Case: MariTide Reaches Market and the IRS Resolves at Manageable Cost

- Repatha’s 34% Q1 growth, reinforced by VESALIUS-CV guidelines and the expansion into high-risk primary prevention with new-to-brand prescriptions up 44% year-over-year, sustains the cardiometabolic revenue floor

- MariTide’s Phase 3 enrollment ahead of expectations and strong Phase 2 maintenance data (greater than 90% patient retention in the long-term extension) support a launch scenario that opens the obesity market, projected to exceed $100 billion annually

- A favorable 2010 to 2015 tax court ruling would remove the dominant balance sheet overhang and likely re-rate the stock toward the 16x to 17x range the multiple touched at prior cycle peaks

- Six key growth drivers growing at 24% aggregate in Q1 2026 provide enough momentum to offset the Prolia/XGEVA erosion and sustain EPS growth through the patent cliff

Downside Risk: IRS Adverse Ruling Compresses Capital Allocation

- A $10.7 billion adverse 2010 to 2015 ruling, followed by a likely additional multibillion-dollar 2016 to 2018 liability, would consume a meaningful portion of Amgen’s free cash flow and constrain the $3 billion buyback program and $2.52 per share quarterly dividend

- Tavneos, currently generating $119 million per quarter and growing 32% year-over-year, faces forced withdrawal if the FDA commissioner orders removal, creating a direct revenue gap with no near-term replacement

- MariTide’s late-2020s launch window competes against Novo Nordisk’s Ozempic/Wegovy franchise, Eli Lilly’s Zepbound, and a pipeline of oral GLP-1s, with differentiation resting entirely on dosing convenience rather than superior efficacy data not yet generated

- Around 60% of the current analyst coverage is Holds or worse, reflecting a base case that is adequately priced but not compelling enough to act on until at least one of the binary catalysts resolves

Is Amgen stock fairly valued right now?

At 14.39x NTM P/E against a historical mean of 14.17x with around 5% consensus EPS growth expected, Amgen stock is fairly valued at current levels.

TIKR’s base case targets around $462 per share by 2030, implying around 42% total return, but the path to outperformance requires a favorable IRS ruling or MariTide approval, neither of which has a confirmed timeline.

Should You Invest in Amgen Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amgen Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amgen Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMGN stock on TIKR for Free →