Key Stats for Occidental Petroleum Stock

- 52-Week Range: $39 to $67

- Current Price: $60

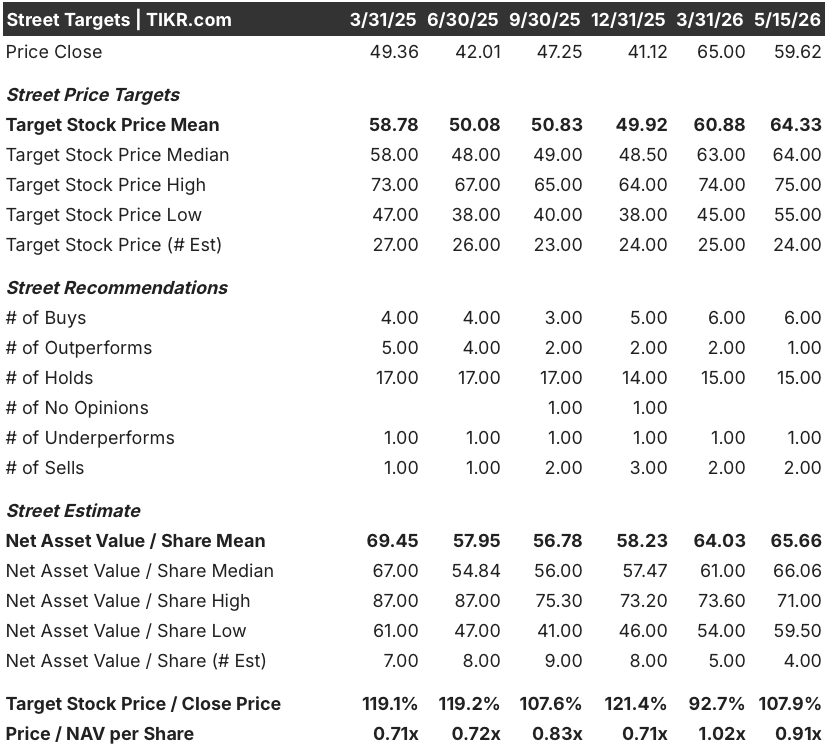

- Street Mean Target: $64

- Street High Target: $75

- Analyst Consensus: 6 Buys / 1 Outperform / 15 Holds / 1 Underperform / 2 Sells

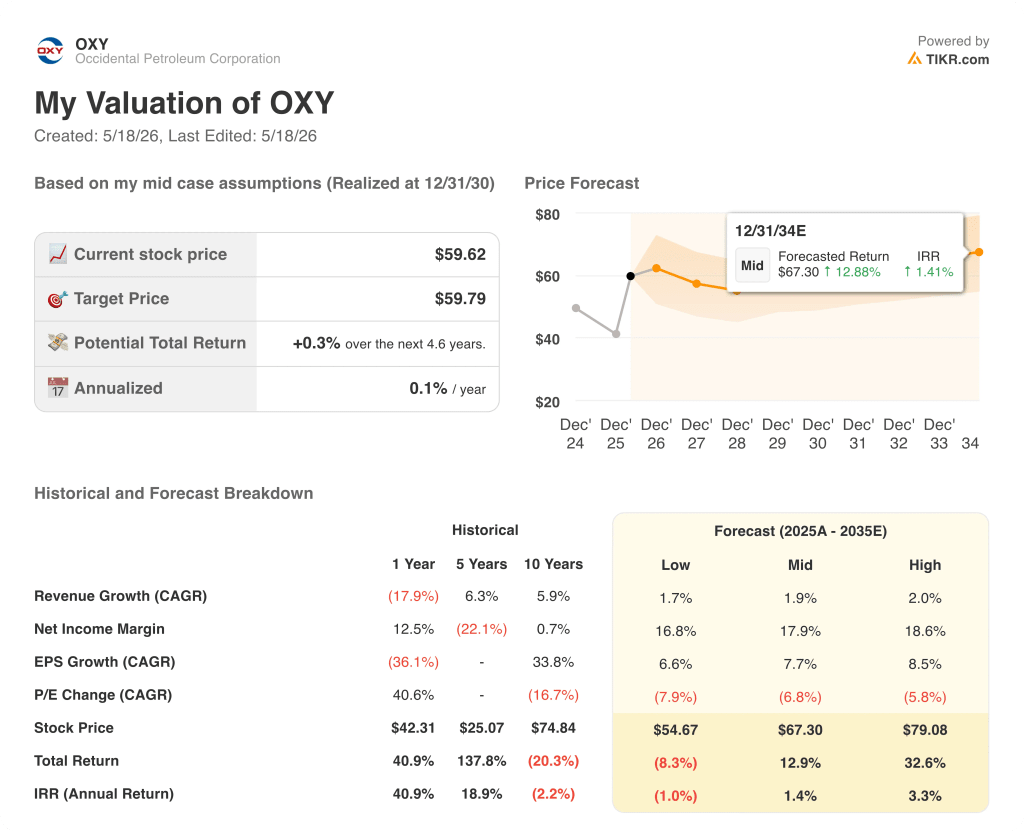

- TIKR Model Target (Dec. 2030): $60

Occidental Petroleum Beats Q1 by 80% and Cuts Debt to $13.3 Billion as the Iran War Reshapes Global Oil

Occidental Petroleum (OXY), one of the largest U.S. shale producers with a 1.4-million-barrel-per-day production base, delivered a first-quarter 2026 adjusted EPS of $1.06 against a Street estimate of just $0.59, a beat of more than 80%.

The catalyst was a combination of operational outperformance and a fundamentally tighter global oil market driven by the U.S.-Israel war on Iran, which has effectively closed the Strait of Hormuz to commercial traffic and removed a significant share of Middle Eastern supply from world markets.

Production averaged 1.426 million barrels of oil equivalent per day in Q1, exceeding the high end of guidance by 21,000 BOE per day, with the beat driven by top-tier new well performance across the Permian and Rockies and a record topside uptime of 98% in the Gulf of America.

Free cash flow before working capital came in at approximately $1.7 billion for the quarter, up roughly 607% year over year from just $240 million in the prior-year period, a result CFO Sunil Mathew attributed to both higher commodity prices and continued cost efficiency gains.

Mathew stated on the Q1 2026 earnings call that “even with oil prices roughly in line with the first quarter of 2025, we generated approximately 52% higher free cash flow from continuing operations, demonstrating our continued focus on cost and operational efficiency.”

Debt reduction has been the defining operational priority since the Anadarko acquisition, and OXY has now cut principal debt from roughly $20.8 billion at the end of Q3 2025 to $13.3 billion today, reducing its annualized interest burden by approximately $550 million versus 2025 levels.

One leadership change sits underneath all of this: longtime CEO Vicki Hollub announced her retirement effective June 1, with COO Richard Jackson set to succeed her as President and CEO, bringing a deep operational background in U.S. unconventional and EOR production and a stated focus on near-term free cash flow growth and further deleveraging.

Wall Street’s Take on OXY Stock

The investment thesis on Occidental Petroleum stock centers not on EPS optionality but on free cash flow generation across the commodity cycle, and Q1 2026 made the strongest single-quarter case in years.

Free cash flow before working capital hit $1.697 billion in Q1 2026 against a Street estimate of $1.409 billion, a beat of roughly 20%, with consensus projecting FCF of around $2.4 billion for Q2 2026, up approximately 147% year over year.

For the full year, consensus FCF is expected to reach near $7 billion across the four quarters of 2026, driven by Brent crude above $100 and Occidental Petroleum’s operating cost efficiency program targeting $500 million in additional oil and gas savings this year.

The 24 analysts covering Occidental Petroleum stock are currently split 6 Buys, 1 Outperform, 15 Holds, 1 Underperform, and 2 Sells, with a Wall Street mean price target of $64.33, implying roughly 8% upside from the current price of $59.62.

The dominant Hold positioning reflects a genuine uncertainty, not skepticism about the asset base: the Iran war has created extreme oil price volatility, and analysts can credibly model OXY stock anywhere from $55 to $75 depending on whether the Strait of Hormuz reopens this year or remains constrained through 2027.

Melius Research analyst James West captured this dynamic cleanly, noting that “the realignment has now positioned the company for success in the future, which is not yet reflected in the shares,” a view that supports the case for mean target convergence if the macro stabilizes.

The specific variable to watch is the debt reduction path: Occidental Petroleum stock’s valuation case strengthens materially once principal debt reaches the $10 billion target, at which point interest savings of roughly $845 million per year become reallocable to dividend growth or share repurchases, and the preferred equity redemption in August 2029 moves within financial reach.

What Does the Valuation Model Say?

TIKR’s base case values Occidental Petroleum at $60per share through December 2030, anchored to a mid-case revenue CAGR of around 2% and a net income margin of roughly 18%, assumptions grounded in the company’s 30-year domestic resource runway and ongoing cost efficiency program targeting $2 billion in cumulative savings since 2023.

At the current price of $60, the mid-case implies essentially no premium to the TIKR model’s base target, yet the high-case scenario reaches $79 per share on a 3% IRR, meaning the stock’s current price reflects a base case in full, with oil price upside entirely unpriced.

Occidental Petroleum stock appears fairly valued at the mid-case but meaningfully undervalued if the Iran supply disruption persists.

The central tension is whether the debt-reduction timeline holds under commodity price volatility: if Brent crude stays above $100 through year-end, OXY reaches its $10 billion principal debt target in 2026 and unlocks the dividend growth and buyback optionality that currently sits behind the balance sheet priority. If prices fall sharply on a peace deal, the timeline extends and the rerating thesis is delayed.

Bull Case

- TIKR’s high-case scenario targets $79 per share, implying roughly 33% total return, driven by a net income margin of 18.6% and EPS CAGR of around 9%

- Q1 2026 FCF of $1.697 billion already exceeds the full Q1 2025 FCF of $240 million by more than 6x, demonstrating what higher prices do to the free cash flow profile at current operating costs

- The $10 billion debt target, when reached, reduces annual interest expense by roughly $845 million versus 2025, freeing cash flow for dividend growth or share repurchases without additional revenue growth

- The Bandit discovery in the Gulf of America, announced in April, is the third deepwater exploration success in three years, expanding the low-decline asset base that underpins the sustaining capital reduction plan

- Management confirmed a target of more than $1.2 billion in incremental free cash flow in 2026 relative to 2025 before higher oil prices are factored in, establishing a rising FCF floor independent of commodity upside

Bear Case

- TIKR’s low-case scenario yields only $54.67 per share, an 8.3% total loss, built on a 1.7% revenue CAGR and EPS CAGR of around 7%, reflecting the risk that oil prices normalize faster than the balance sheet deleverages

- OXY hedged 100,000 barrels per day from March through December 2026 with a WTI ceiling of roughly $76, capping realized price upside precisely when spot prices moved highest; the company has since stopped adding new hedges

- International production guidance was cut to 218,000-228,000 BOE per day for 2026 from a prior 230,000-240,000, reflecting ongoing Al Hosn constraints in the UAE and Middle East disruptions that management does not expect to fully normalize until H2 2026

- The Wall Street mean target of $64.33 implies only 8% upside, a tepid return profile that explains why 15 of 24 analysts rate OXY stock a Hold rather than committing to a more constructive view

- The preferred equity redemption trigger in August 2029 creates a fixed capital allocation priority that limits shareholder return flexibility for the next three years regardless of oil prices

Is Occidental Petroleum stock a buy right now?

Occidental Petroleum stock sits near the TIKR base-case valuation of $60 with roughly 8% upside to the Wall Street mean target of $64.

The bull case, which targets around $79 per share, requires sustained Brent crude above $100 and continued progress on the $10 billion debt target.

With 6 Buys and 15 Holds among 24 analysts, consensus reflects optionality rather than conviction, and the clearest buy signal would be confirmation of the $10 billion debt milestone.

How did Occidental Petroleum perform in Q1 2026 earnings?

Occidental Petroleum’s Q1 2026 adjusted EPS came in at $1.06, beating the Street estimate of $0.59 by more than 80%. Production averaged 1.426 million BOE per day, exceeding the high end of guidance.

Free cash flow before working capital reached $1.697 billion, up more than 600% year over year, as higher oil prices and cost efficiency gains combined to produce the strongest quarterly cash flow result in recent history.

What is the price target for OXY stock?

The Wall Street mean price target for OXY stock is $64, implying roughly 8% upside from the current price of $60.

The Street high target sits at $75 and the low at $55.

TIKR’s base case reaches $60, while the high scenario prices OXY at around $79, a total return of roughly 33%, contingent on a sustained high oil price environment and successful completion of the balance sheet deleveraging plan.

Should You Invest in Occidental Petroleum Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Occidental Petroleum Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Occidental Petroleum Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze OXY stock on TIKR for Free →