Key Stats

- Current price: ~$23 (May 15, 2026 close: $22.92, up 13%)

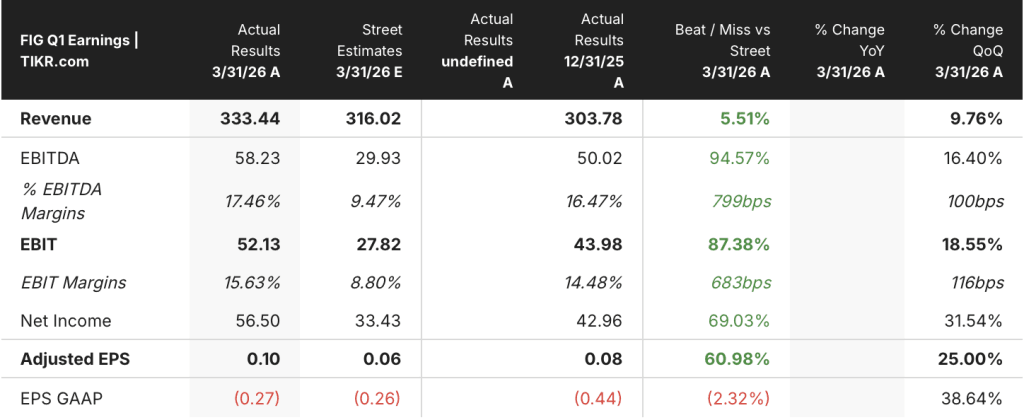

- Q1 2026 revenue: $333M, +46% YoY

- Q1 2026 adjusted EPS: $0.10

- Q1 2026 non-GAAP operating margin: 16%

- Q2 2026 revenue guidance: $348M to $350M (~40% YoY growth at midpoint)

- Full-year 2026 revenue guidance: $1.422B to $1.428B (~35% YoY growth at midpoint); raised $55M from prior outlook

- Full-year 2026 non-GAAP operating income guidance: $125M to $135M (~9% margin at midpoint); raised $25M from prior outlook

- TIKR model price target: $65.10

- Implied upside: ~184%

Figma Stock Surges 13% as Revenue Growth Reaccelerates to 46%

Figma stock (FIG) jumped more than 13% after the company reported Q1 2026 revenue of $333M, up 46% year-over-year and above the high end of its own guidance.

That acceleration marks the second consecutive quarter of improving year-over-year growth, following 40% in Q4 2025 and 38% in Q3 2025.

The outperformance was broad-based: seat expansion across entire organizations, AI product adoption, and international business, which grew 48% year-over-year according to CFO Praveer Melwani on the Q1 2026 earnings call.

Net dollar retention rate for paid customers spending more than $10,000 in ARR reached 139%, up 3 percentage points from the prior quarter and the highest level in over two years, according to Melwani on the Q1 2026 earnings call.

Paid customers spending more than $100,000 in ARR grew 48% year-over-year in Q1, a 2-point acceleration from Q4, according to Melwani on the Q1 2026 earnings call.

The overall customer base grew to approximately 690,000 paid customers from approximately 450,000 in Q1 of last year, a 54% increase year-over-year, according to Melwani on the Q1 2026 earnings call.

AI credit monetization was a material development this quarter: Figma began enforcing credit limits on March 18, and as of end of April, over 75% of Org and Enterprise users who were previously over their credit limit continued consuming credits, according to Melwani on the Q1 2026 earnings call.

Make adoption among the largest customers also strengthened: approximately 60% of customers with more than $100,000 in ARR used Make weekly in Q1, up from over 50% in Q4, according to Melwani on the Q1 2026 earnings call.

MCP weekly active users in Figma Design grew 5x quarter-over-quarter, according to CEO Dylan Field on the Q1 2026 earnings call.

Among customers with more than $100,000 in ARR, those using Figma’s MCP grew full seats approximately 70% faster over the quarter than customers not using the MCP server, according to Melwani on the Q1 2026 earnings call.

On the enterprise side, one of the world’s largest hyperscalers consolidated fragmented Figma usage into a single agreement with over 35,000 paid seats, one of the largest deals in Figma’s history, according to Melwani on the Q1 2026 earnings call.

Figma raised its full-year 2026 revenue guidance to $1.422B to $1.428B, implying ~35% growth at the midpoint and a raise of $55M from its prior outlook.

Full-year non-GAAP operating income guidance was raised to $125M to $135M, up $25M from prior guidance, implying approximately 9% operating margin at the midpoint, according to Melwani on the Q1 2026 earnings call.

Figma Stock: What the Income Statement Shows

Figma’s income statement tells an acceleration story interrupted by GAAP accounting noise, with the non-GAAP picture the more relevant lens for the current growth phase.

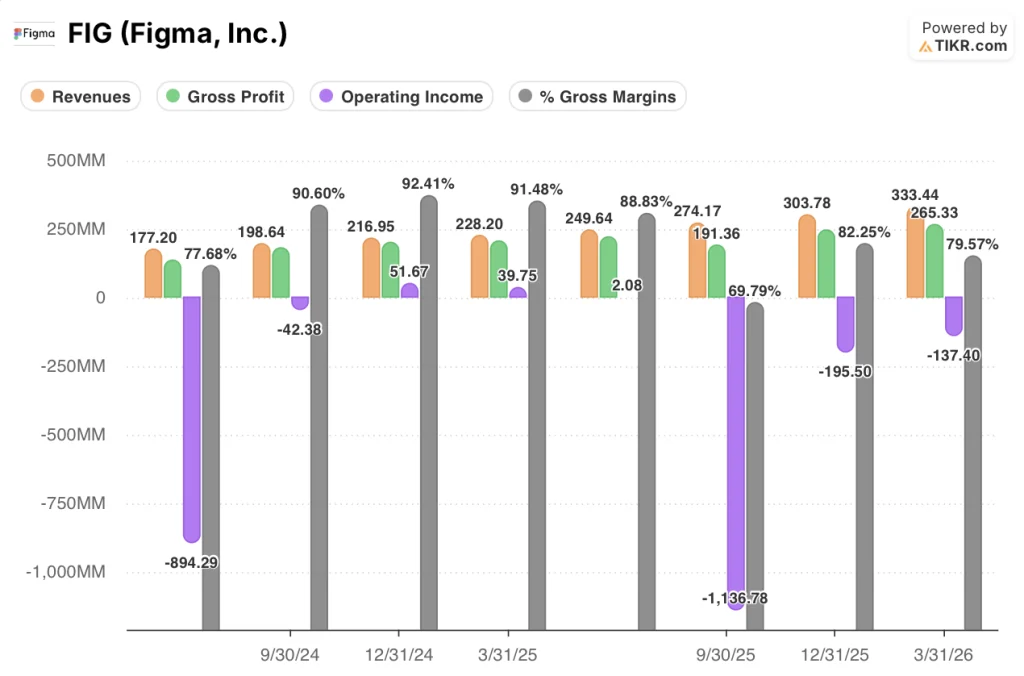

Revenue has moved in a consistent upward arc across the past eight quarters: from $177M in Q2 2024 to $333M in Q1 2026, with no quarter of sequential decline.

Q1 2026 revenue of $333M represents 9.76% sequential growth from $304M in Q4 2025.

Gross profit as reported in the income statement was $265M in Q1 2026, with a GAAP gross margin of 79.6%, down from 92.4% in Q4 2024 and 91.5% in Q1 2025.

Melwani attributed the gross margin compression to broader and deeper adoption of AI features, with users accessing higher capability models, according to his remarks on the Q1 2026 earnings call; he flagged routing queries across models and investing in first-party models trained on Figma’s design corpus as levers to manage inference costs as adoption scales.

Non-GAAP gross margin was 82% in Q1 2026, and non-GAAP operating margin was 16%, representing $52M in non-GAAP operating income, according to Melwani on the Q1 2026 earnings call.

GAAP operating income was ($137M) in Q1 2026, reflecting stock-based compensation and one-time items; this is the primary driver of the divergence between GAAP and non-GAAP profitability.

What Does the Valuation Model Say?

The TIKR model puts a price target of $65.10 on Figma stock, implying approximately 184% upside from the May 15 close of $22.92.

The mid-case assumptions driving that target include a revenue CAGR of 16% from 2025 to 2035 and a net income margin of 13%.

Q1’s 46% revenue growth lands well above the model’s mid-case CAGR, which means either the model is conservative on the growth trajectory or the growth pace decelerates materially in the years ahead.

Full-year guidance of ~35% growth already implies a step-down from Q1’s pace, which is the honest constraint on how much the Q1 beat alone re-rates the long-term picture.

The investment case for Figma stock is stronger after this print: reaccelerating growth, AI monetization beginning to show conversion rates, and raised guidance all tighten the probability distribution around the bull case.

Figma delivered an exceptional Q1, but AI credit monetization began only six weeks before the quarter closed, and whether it sustains is the load-bearing assumption for every growth scenario from here.

What Has to Go Right

- AI credit monetization must sustain at the conversion rates seen in April, where 75% of previously over-limit Org and Enterprise users continued consuming credits after enforcement began on March 18

- Full-seat upgrades driven by MCP and Make access must continue: customers using MCP grew full seats 70% faster than non-MCP customers during Q1, and Pro team conversions were up over 150% year-over-year

- Revenue growth must hold near the guided ~40% for Q2, and the full-year guide of ~35% must prove conservative, as it did in Q1 when Figma came in above the high end of guidance

- Gross margin must stabilize: non-GAAP gross margin was 82% in Q1, and Figma’s ability to route queries across models and deploy first-party design-corpus models will determine whether AI infrastructure costs compress margins further

What Could Still Go Wrong

- Q1’s 46% growth included only two weeks of credit monetization revenue (enforcement began March 18); Q2 is the first full quarter, and the ramp may disappoint if enterprise contracting cycles slow credit add-on purchases

- Non-GAAP operating margin guidance of approximately 9% for the full year implies material compression from Q1’s 16%, reflecting Config event costs in Q2 and continued investment in AI infrastructure

- GAAP operating loss of ($137M) in Q1 2026 and stock-based compensation as a percentage of revenue remain elevated, and Figma stock trades at a significant premium to the model’s 13% net income margin assumption

- Competitive surface area is expanding: Field named Anthropic specifically as a company capable of pairing first-party models with its own products, and new entrants from LLM providers are increasing the pace of product change Figma must match

Should You Invest in Figma, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Figma, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Figma, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FIG stock on TIKR for Free →