Key Stats for Arista Networks Stock

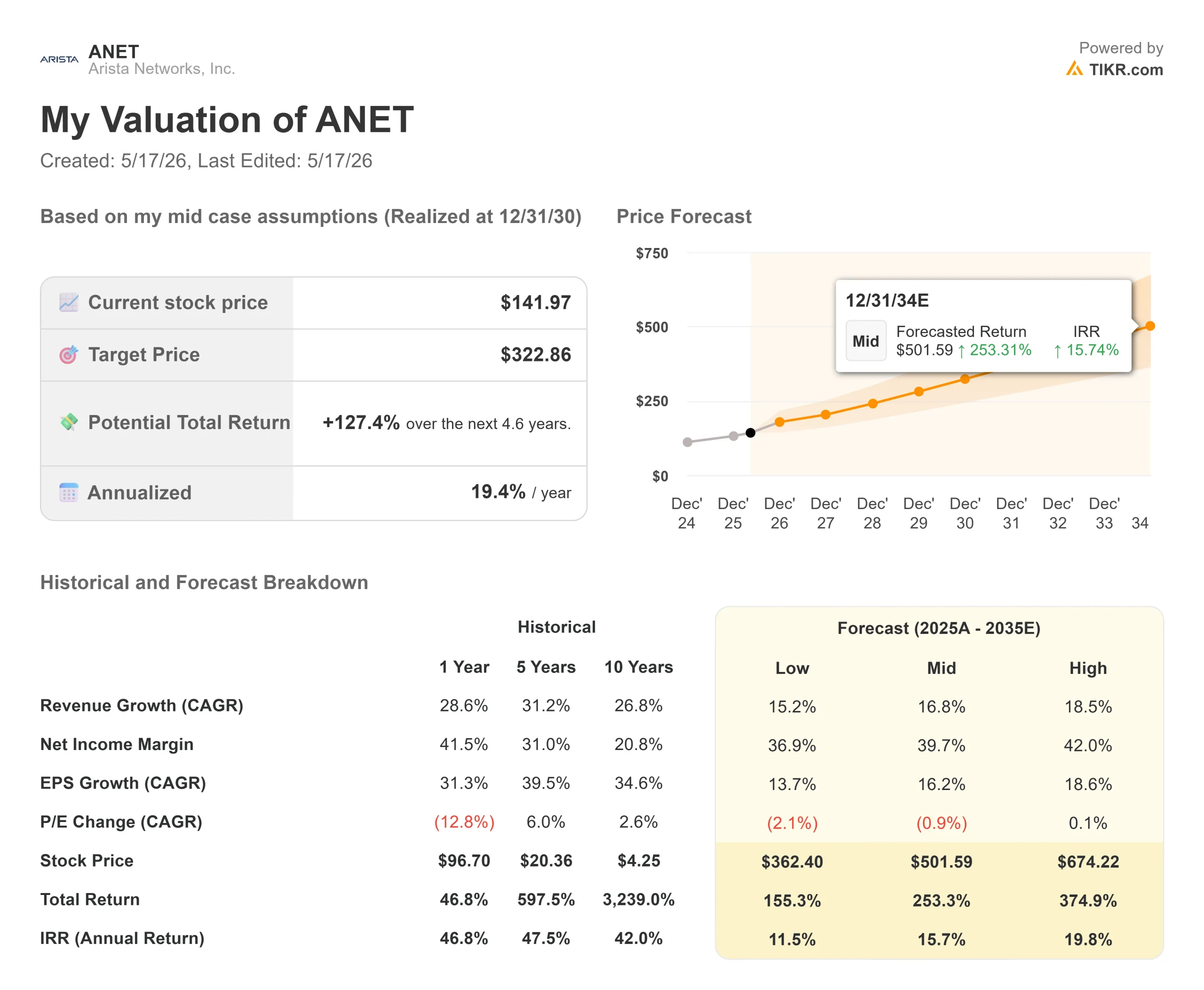

- Current Price: $141.97

- Target Price (Mid): ~$323

- Street Target: ~$188

- Potential Total Return: ~127%

- Annualized IRR: ~19% / year

- Earnings Reaction: -13.61% (5/5/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Arista Networks (ANET), the company building the Ethernet backbone behind the AI infrastructure build-out, handed investors one of the stranger two-week stretches in its recent history. On May 5, it reported Q1 2026 revenue of $2.709 billion, up 35.1% year-over-year, beat non-GAAP EPS estimates, and raised its full-year guide to $11.5 billion. The stock fell 13.61% the next day.

Then, on May 14, CFO Chantelle Breithaupt appeared at Needham’s 21st Annual Technology, Media & Consumer Conference and delivered a calm rebuttal of everything the sell-off implied. The question investors are sitting with is simple: Did the market get this one wrong?

The frustration was understandable. Arista had rallied more than 34% in the month before earnings, building in expectations that a roughly in-line Q2 guide could not clear. Supply chain warnings about component shortages through 2026 added pressure, as did a non-GAAP gross margin of 62.4% running below prior-year levels. What the Needham conference added was context that those headline numbers do not show.

What the Market Priced In, and What It Missed

The most important reframe from Needham was deferred revenue. Arista’s total deferred revenue reached $6.2 billion as of March 31, 2026, up roughly 100% year-over-year per the Q1 2026 10-Q. This is a contracted AI demand that customers have formally accepted but that Arista cannot yet recognize as revenue, because hyperscale deployments require physical rack space, GPU installations, and power infrastructure to be complete first.

Breithaupt made this explicit at Needham: “Most of what’s sitting in deferred is AI use case and product. And so you have to look at both combined to look at the AI demand that we’re seeing across the board.” Using that combined view, she framed growth at 54% year-over-year, management’s own non-GAAP characterization, not a reported figure, but one that speaks directly to the gap between what Arista is booking and what it can currently ship.

The gap exists because of purchase commitments. Arista’s commitments jumped from $6.8 billion at Q4-end to $8.9 billion after Q1, locking in chip supply through TSMC on a 52-week lead time. SVP John McCool was direct: “We are very comfortable with the guide on both margin and revenue.” That $8.9 billion is not speculative inventory. It is a contractual supply secured against demand that already exists in the order book.

Breithaupt also addressed the guidance conservatism directly. Arista raised its full-year outlook twice in the past two quarters. “I would choose that one,” she said when the moderator described the approach as beat-and-raise. That track record matters when assessing how much room the $11.5 billion guide might have to the upside.

See historical and forward estimates for Arista Networks stock (It’s free!) >>>

Three Growth Drivers That Have Not Peaked

The Needham transcript clarified three forward growth engines that got less airtime than supply chain concerns.

The first is AI networking breadth. Arista raised its 2026 AI revenue target from $3.25 billion to $3.5 billion. Breithaupt noted it now covers more than 100 customers across hyperscalers, Neoclouds (smaller cloud providers building AI infrastructure), and enterprise, not just the four large AI customers that originally defined the thesis.

The second is scale-across. While scale-out (connecting GPU clusters within a single data center via a leaf-spine network) is Arista’s core business today, VP of Investor Relations Rudolph Araujo described scale-across as an early-stage opportunity with limited competition. Scale-across connects distributed data centers through Arista’s high-end routing platform, driven by the reality that no single facility has unlimited power or cooling. “A lot of our competitors that we would run into in scale-out don’t have the product set to compete in scale-across,” Araujo said. The revenue contribution is not in the current guide, but design-in decisions at hyperscalers happening now will determine who captures that market.

The third is Campus. Arista hit its $800 million campus revenue target for 2025 and raised the 2026 goal to $1.25 billion, implying 55% growth in a market expanding in the low single digits. Araujo’s framing was precise: Arista holds roughly 3% to 4% campus market share today and is winning proofs-of-concept before it is even present on the data center side of campus.

One competitive development this week reinforces the broader demand picture. Cisco reported record Q3 fiscal 2026 revenue of $15.8 billion, up 12% year-over-year, and doubled its AI infrastructure order target to $9 billion, sending shares up 17%. That matters here because it confirms AI networking demand is expanding broadly, not a zero-sum market where Arista wins only if Cisco loses.

XPO: Setting the Table for the Next Hardware Cycle

Arista announced a multi-source agreement for XPO, a 12.8 Tbps liquid-cooled pluggable optics module, which Araujo confirmed delivers more than 40% footprint reduction versus the current OSFP standard. McCool put it in context: OSFP made 800-gigabit switching viable. XPO is designed to do the same for 1.6 terabit and especially 3.2 terabit deployments, where OSFP hits thermal limits.

The commercial implication is significant. As recently as a quarter ago, industry consensus held that coherent pluggable optics (CPO) would be mandatory at 3.2T. XPO removes that constraint, preserving customer optionality and extending Arista’s Etherlink platform into the next hardware generation. First products are expected in 2027. The revenue is not in the current model, but architecture decisions made today will determine who wins the 3.2T wave.

See how Arista Networks performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $141.97

- Target Price (Mid): ~$323

- Potential Total Return: ~127%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for Arista Networks stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of around 17% through December 31, 2030. Two drivers carry that assumption: AI center networking, where Arista’s $3.5 billion 2026 target is supply-gated rather than demand-gated, and campus expansion, where a $1.25 billion 2026 target is building from a 3% to 4% share base. The margin driver is operating leverage as software and services grow as a share of revenue, consistent with Arista’s LTM free cash flow margin of approximately 45% per TIKR data.

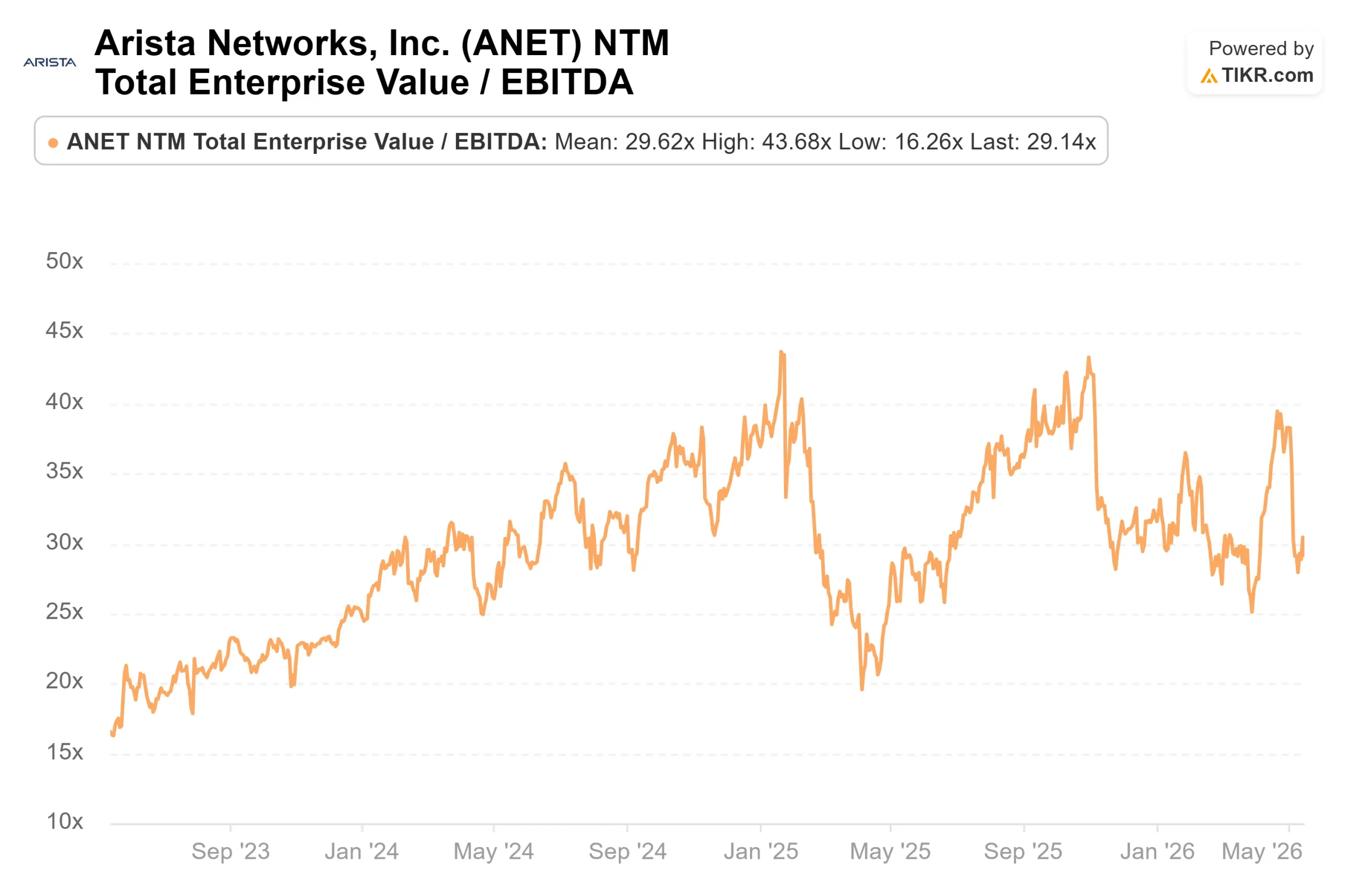

The upside: at around 19% annualized returns to reach approximately $323 by December 31, 2030, the mid-case rewards investors who can hold through near-term supply disruption. The risk: if the $8.9 billion in purchase commitments do not convert to shipped revenue at the implied rate, or if deferred revenue accumulates without being recognized, a stock at roughly 37x forward earnings per TIKR has a limited cushion for a guidance miss.

Of 31 analysts covering ANET, 21 rate it Buy, 8 rate it Outperform, and 1 rates it Hold. The street mean target is approximately $188, implying around 32% upside from current prices per TIKR. The TIKR mid-case is materially higher because it captures campus, scale-across, and XPO contributions over a longer horizon.

Conclusion

The specific thing to watch is Q2 2026 deferred revenue, reported when Arista announces results on August 3, 2026. If the balance grows from $6.2 billion toward $6.5 billion or higher, it confirms AI acceptance cycles are building backlog faster than current-period revenue implies, and the full-year guide has room to run. A sequential decline below $5.8 billion would be the clearest near-term warning sign. Either reading tells investors more about 2027 revenue than the Q2 headline figure itself.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Arista Networks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Arista Networks, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arista Networks alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Arista Networks on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!