Key Stats for Ford Stock

- 52-Week Range: $10 to $15

- Current Price: $13

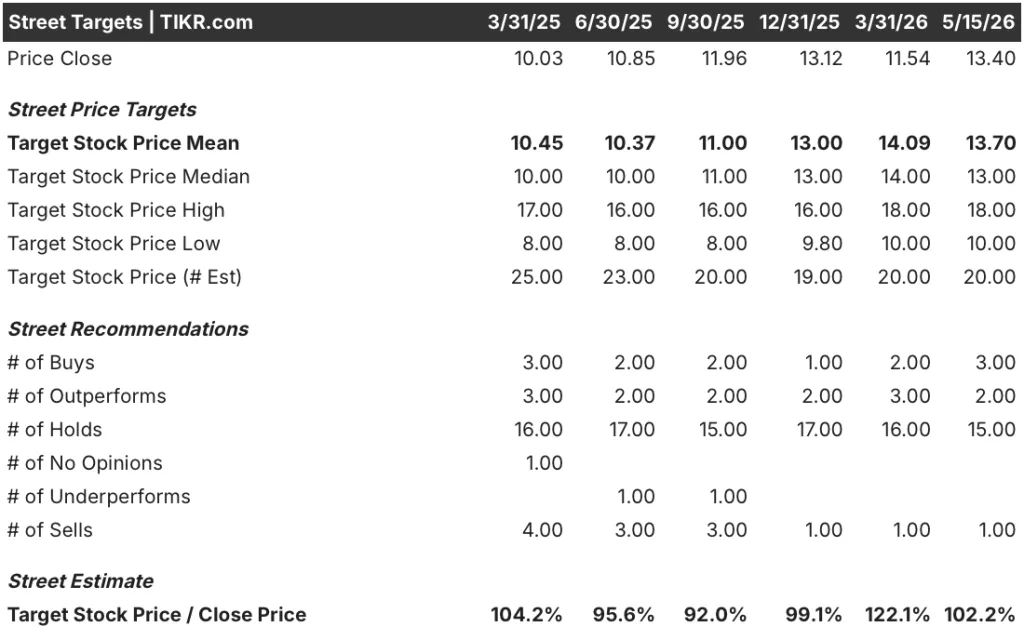

- Street Mean Target: $14

- Street High Target: $18

- Analysts Consensus: 3 Buys / 2 Outperforms / 15 Holds / 0 Underperforms / 1 Sell

- TIKR Model Target (Dec. 2030): $21

Ford Stock Surges 13% as a New Energy Business Rewrites the Investment Case

Ford Motor Company (F) surged 13% in a single session last May 13, its biggest single-day gain in roughly six years, after Morgan Stanley called the automaker’s newly launched energy storage business and its CATL battery partnership an “underappreciated strategic competitive advantage” following Ford’s Q1 2026 earnings call.

The company is one of America’s largest automakers by volume, but the investment case is shifting fast.

Ford announced its wholly-owned energy subsidiary in December, converting Kentucky plant space that had been earmarked for EV battery production into a facility for grid-scale energy storage systems targeting data centers, utilities, and large industrial customers.

The business uses LFP prismatic battery technology licensed from CATL, the world’s leading battery manufacturer, and Morgan Stanley estimates the unit can generate $500 million to $600 million in EBIT annually, turning profitable by 2028.

Ford is committing $2 billion to the energy business, with first customer deliveries targeted for late 2027 and a capacity target of at least 20 GWh annually at launch.

On the Q1 2026 earnings call, CEO Jim Farley was direct about the strategic logic: “The energy business is a key element of our bridge to 8% margin.”

The broader automotive business also delivered, with Q1 adjusted EBIT of $3.5 billion on $43.3 billion in revenue, a result that prompted management to raise full-year adjusted EBIT guidance to $8.5 billion to $10.5 billion, up from the prior $8 billion to $10 billion range.

Wall Street’s Take on F Stock

The debate around Ford stock is not whether the truck business works. It is whether a company generating $43.3 billion in Q1 revenue can attach a second, higher-margin business to that industrial base before the market prices it in.

Revenue is the right metric to anchor this analysis, because the story is a volume business trying to add margin layers, not a growth company expanding its top line at pace.

Q1 2026 revenue of $39.8 billion came in 6.4% above Q1 2025, a clean beat driven by F-Series strength, a richer off-road trim mix in Ford Blue, and continued momentum in Ford Pro’s software and services subscription base, which reached 879,000 paid subscribers, up 30% year-over-year.

The forward picture is more measured: consensus estimates project Q2 2026 revenue of around $44.7 billion, roughly flat with Q2 2025’s $46.9 billion, a 5% year-over-year decline that reflects the Novelis aluminum supply disruption’s overhang on F-Series production volume in the first half of the year.

The recovery is expected in the second half, with Q4 2026 revenue consensus at around $44.3 billion and Q1 2027 at around $41.7 billion, a trajectory that assumes Novelis fully restores throughput and F-Series production normalizes as guided.

Ford Pro’s paid software subscriptions and Ford Blue’s off-road mix expansion are the two mechanisms the Street is watching most closely as evidence that margin durability is improving independent of volume.

Analyst coverage stands at 3 Buys / 2 Outperforms / 15 Holds / 0 Underperforms / 1 Sell across 20 analysts, with a Wall Street Mean target of $14, implying roughly 2% upside from the current price of $13, and a Street High of $18 implying around 34% upside for those who believe Ford Energy’s 2027 launch timeline holds.

With 15 of 20 analysts sitting on Hold and the mean target barely above the current price, Ford stock appears fairly valued on current Street consensus, though that consensus was built before Morgan Stanley’s energy note reset the conversation around what this business could be worth by 2028.

What Does the Valuation Model Say?

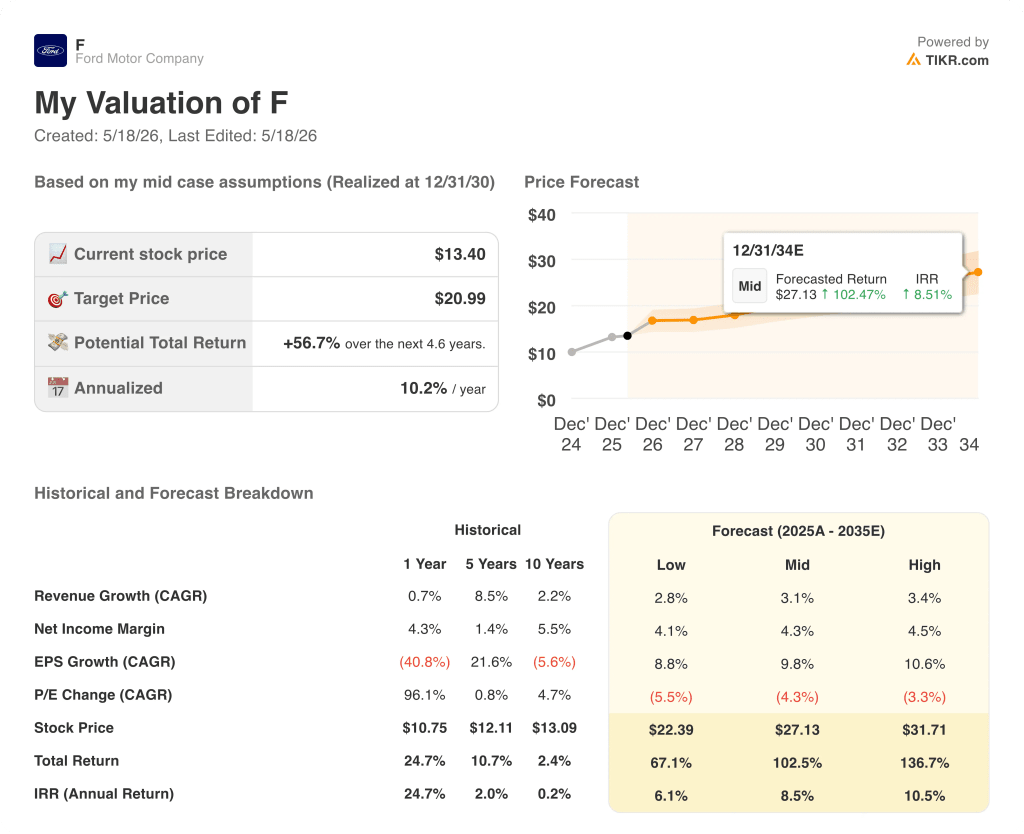

TIKR’s base case values Ford at $21 per share by December 2030, built on a mid-case revenue CAGR of around 3% and a net income margin expanding to around 4%, assumptions that reflect Ford Energy’s contribution beginning to show in the EBIT profile from 2028 onward as the Kentucky facility scales toward its 20 GWh annual capacity target.

With Ford stock trading at $13.4 and the mid-case implying around 57% total return over 4 and a half years, the TIKR model puts F squarely in undervalued territory for investors with a multi-year horizon and tolerance for the near-term noise around commodity costs and the energy launch.

The pivot point for the entire thesis lands in late 2027: if Ford Energy delivers on its first customer shipments on schedule and begins converting inbound interest from utilities and data centers into signed contracts, the Street’s current Hold-heavy consensus is likely to shift, and the mean target gap between $13.70 and the TIKR model’s $21 will close faster than the current 4.6-year base case implies.

Base Case:

- TIKR’s mid-case projects EPS CAGR of around 10% through 2035, anchored to Ford Energy’s EBIT contribution from 2028, Ford Pro subscription growth sustaining its 30% year-over-year pace, and the Novelis aluminum supply chain normalizing by late 2026

- Q1 2026 revenue of $39,819 million grew 6.4% year-over-year, and consensus projects the trajectory to stabilize in the $44 billion to $45 billion per quarter range through 2027 as Novelis headwinds clear and F-Series production ramps

- Ford Blue’s off-road trim mix at nearly 25% of U.S. volume continues supporting average transaction prices above industry average, with Ford Blue EBIT guidance raised to $4.5 billion to $5 billion for full-year 2026

- Ford Pro’s 879,000 paid software subscriptions represent a recurring revenue stream growing at 30% year-over-year that is largely insulated from vehicle volume swings and provides EBIT margin far above the segment average

- Ford’s full-year adjusted EBIT guidance of $8.5 billion to $10.5 billion, raised after a Q1 that delivered $3.5 billion in adjusted EBIT, provides a conservative floor the truck and commercial businesses have already demonstrated they can defend

Downside Risk:

- Commodity headwinds have expanded to just above $2 billion for full-year 2026, around $1 billion worse than the prior estimate, with aluminum pricing driven by global supply constraints and the Middle East conflict; further escalation is not in guidance

- Ford Energy’s 2028 profitability target depends on commercial contracts with utilities and data centers that have not yet been announced, and the Morgan Stanley EBIT estimate of $500 million to $600 million annually is contingent on those contracts materializing on schedule

- The $1.3 billion one-time IEEPA tariff benefit recognized in Q1 will not repeat, creating a meaningful year-over-year headwind in Q2 through Q4 that CFO Sherry House explicitly flagged as the primary driver of back-half earnings step-down

- Model e losses are guided at $4 billion to $4.5 billion for 2026, and while Gen 1 losses improved 35% in Q1, the segment’s EBIT drag persists until the Universal EV Platform launches from Louisville Assembly in 2027

- Unifor has confirmed 2026 Detroit Three labor negotiations begin June 22 starting with Ford, a contract cycle that introduces a cost variable not yet reflected in full-year guidance

Should You Invest in Ford Motor Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ford Motor Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ford Motor Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze F stock on TIKR for Free →