Key Stats for Bristol-Myers Squibb Stock

- Current Price: $57

- Target Price (High Case): ~$61

- Target Price (Mid Case): ~$50

- Street Target: ~$63

- Potential Total Return (High Case): ~7%

- Annualized IRR (High Case): ~1%/year

- Earnings Reaction: (3.91%) on 4/30/26

- Max Drawdown: (15.96%) on 10/29/25

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Bristol-Myers Squibb (BMY) has spent two years asking investors to be patient. Patent cliffs on ELIQUIS and OPDIVO are real, revenue is declining, and the stock sits 9% below its 52-week high. The debate investors are having is not whether the pressure is real; it is whether the pipeline is big enough and close enough to matter before the damage compounds.

On May 14, 2026, the same day the company announced a $15.2 billion collaboration with China’s Hengrui Pharma spanning 13 early-stage oncology and immunology programs, Chief Commercial Officer Adam Lenkowsky appeared at the Bank of America Global Healthcare Conference and made the case in detail.

The Growth Portfolio Is Real the Math Is Still Hard

The clearest signal from Q1 2026: the growth portfolio grew 12% year over year, as Lenkowsky confirmed. For a $48 billion company, that is not a trivial number.

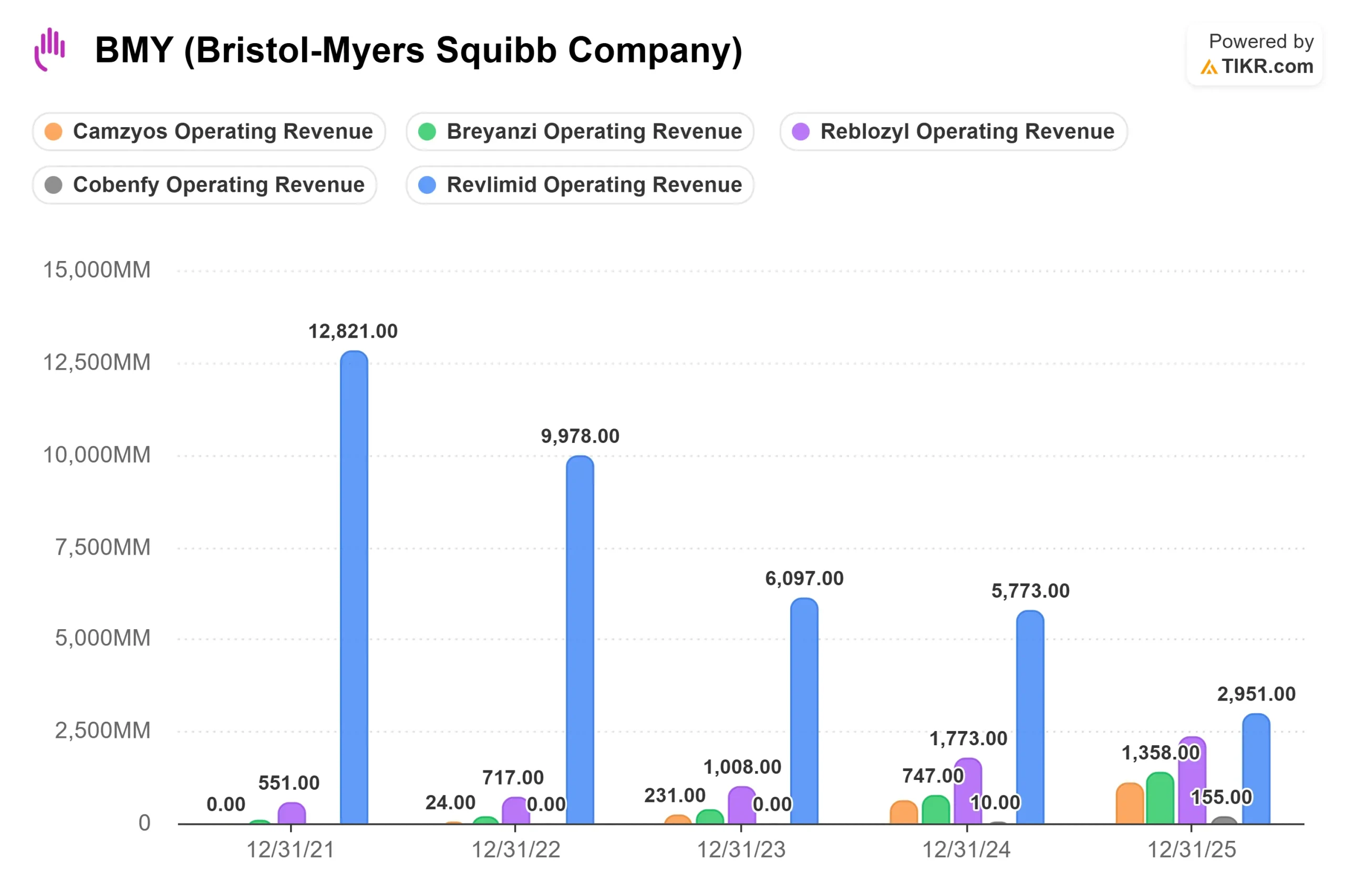

Three products are driving most of it. REBLOZYL, which treats anemia, generated $2,327 million in 2025. BREYANZI, a CAR-T cell therapy for relapsed or refractory large B-cell lymphoma and other blood cancers, reached $1,358 million. CAMZYOS, the obstructive cardiomyopathy drug, hit $1,068 million. All three figures are reported actuals from the TIKR segment data. ELIQUIS remains the cash engine at $14,443 million in 2025, with management guiding for double-digit growth this year.

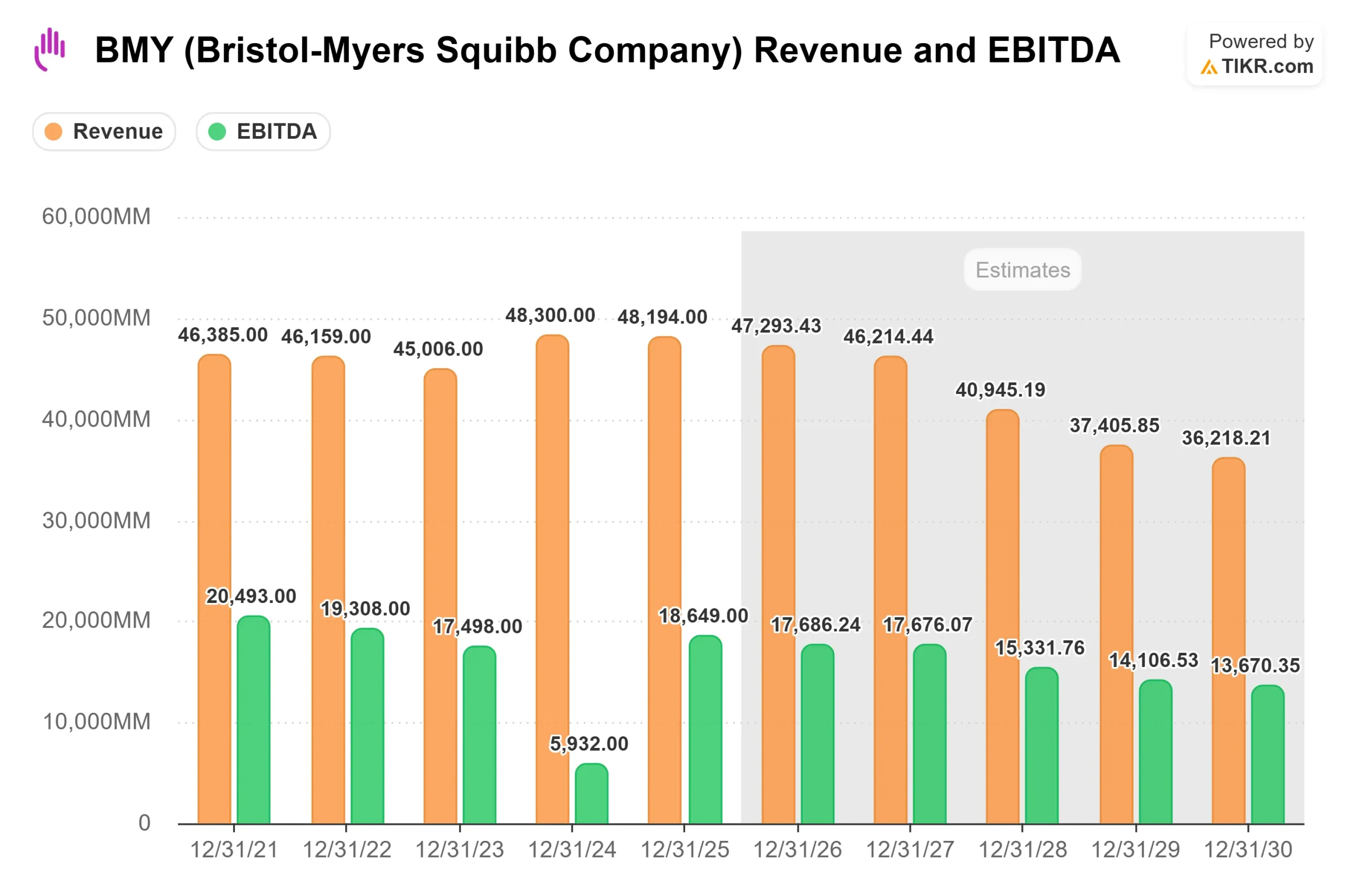

What sits behind those pillars is the harder story. REVLIMID generated $12,821 million in 2021 and fell to $2,951 million in 2025 as full generic competition arrived. TIKR consensus estimates show total revenue declining from $48,194 million in 2025 to around $36,218 million by 2030, a compound annual growth rate of around (2.7%) over that period. The products that exist today are managing a retreat. The products not yet approved are the thesis.

See historical and forward estimates for Bristol-Myers Squibb stock (It’s free!) >>>

Three Things Investors Should Not Miss

CAMZYOS has a real competitive moat for now. A new competitor has entered the obstructive hypertrophic cardiomyopathy (oHCM) market, a condition causing abnormal thickening of the heart muscle. Lenkowsky was candid about what he is actually seeing: physicians who have tried the competing drug are defaulting to CAMZYOS’s established dosing workflow. “Most of the patients are on either 5 or 10 milligrams,” he said. “Patients are going to feel better almost immediately, versus what we’ve seen with the competition, you really need to titrate that up to the highest 2 doses.” BMS has also partnered with Viz.ai, an AI diagnostic company now operating inside roughly 120 centers of excellence, which has screened over 3 million echocardiograms to improve diagnosis rates. With approximately 100,000 diagnosed oHCM patients still untreated, the runway remains real even with a second entrant in the market. Both the Viz.ai partnership and patient figures were confirmed by Lenkowsky.

COBENFY’s real story is Alzheimer’s, not schizophrenia. COBENFY, approved for schizophrenia and distinguished by its muscarinic receptor mechanism, completely different from every existing antipsychotic, generated $155 million in full-year 2025 revenue, per TIKR segment data. Lenkowsky acknowledged the pace plainly: “COBENFY is delivering steady growth.” But his real argument was for what comes next. Every existing antipsychotic carries a black-box warning for elderly patients with dementia. COBENFY does not. BMS is running the pivotal ADEPT program in Alzheimer’s disease psychosis, with data expected by the end of 2026 per management. If those trials read positively, the addressable population expands well beyond schizophrenia, and the regulatory asymmetry becomes the commercial argument in long-term care settings.

Milvexian is the biggest binary event on the calendar. Milvexian is an experimental anticoagulant that BMS is co-developing with Johnson & Johnson, targeting atrial fibrillation patients who need stroke prevention with less bleeding risk than current options. Lenkowsky put the opportunity in direct terms: roughly 40% of the approximately 10 million diagnosed AFib patients in the U.S. are either untreated, undertreated, or have discontinued therapy largely because of bleeding concerns. His stated base case: “Comparable effect to ELIQUIS… with a superior bleeding profile.” OCEANIC-AF results are expected by year-end 2026, per management. That is the single most consequential binary event for BMY’s long-term revenue trajectory. Both the 10 million patient figure and the 40% estimate were stated by Lenkowsky.

The Hengrui Deal: Right Strategy, Long Timeline

The $15.2 billion Hengrui collaboration is structured carefully: BMS commits $600 million upfront, with up to $950 million through 2028. The remaining value is milestone-contingent. All 13 programs are early-stage and have not yet entered human trials, so the near-term cash impact is manageable, and the deal does not change 2026 financials.

The strategic logic is about 2030 and beyond. When OPDIVO biosimilars eventually arrive, BMS needs a new generation of immuno-oncology combinations ready. Lenkowsky framed the intent directly: “By leveraging complementary capabilities across geographies, we aim to accelerate early clinical learning and make informed decisions that support driving top-tier growth in the next decade.” The Hengrui assets join a pipeline that already includes pumitamig, a PD-L1/VEGF-A bispecific antibody with seven active Phase 3 trials across lung, breast, and gastric cancers, as confirmed by Lenkowsky. It is the right long-term strategy. It is also a 2029 story.

How BMY Is Priced Against Peers

At $57, BMY trades at 8.26x NTM EV/EBITDA and 9.30x NTM P/E, per TIKR. That is a steep discount to Johnson & Johnson at 15.46x NTM EV/EBITDA and Merck at 13.47x. Even Pfizer, navigating its own post-COVID revenue transition, trades at 8.03x, nearly in line with BMY. The discount reflects a specific market judgment: JNJ and MRK have cleaner near-term earnings trajectories and less concentrated pipeline risk than BMY carries today. Of the 30 analysts covering BMY per TIKR, 6 have Buy ratings, 4 Outperform, 18 Hold, 1 No Opinion, and 1 Sell. The Street consensus target is around $63, implying roughly 10% upside from current levels. The market is not pricing in failure, it is pricing in uncertainty.

See how Bristol-Myers Squibb performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $57.00

- Target Price (High Case): ~$61

- Potential Total Return (High Case): ~7%

- Annualized IRR (High Case): ~1%/year

See analysts’ growth forecasts and price targets for Bristol-Myers Squibb stock (It’s free!) >>>

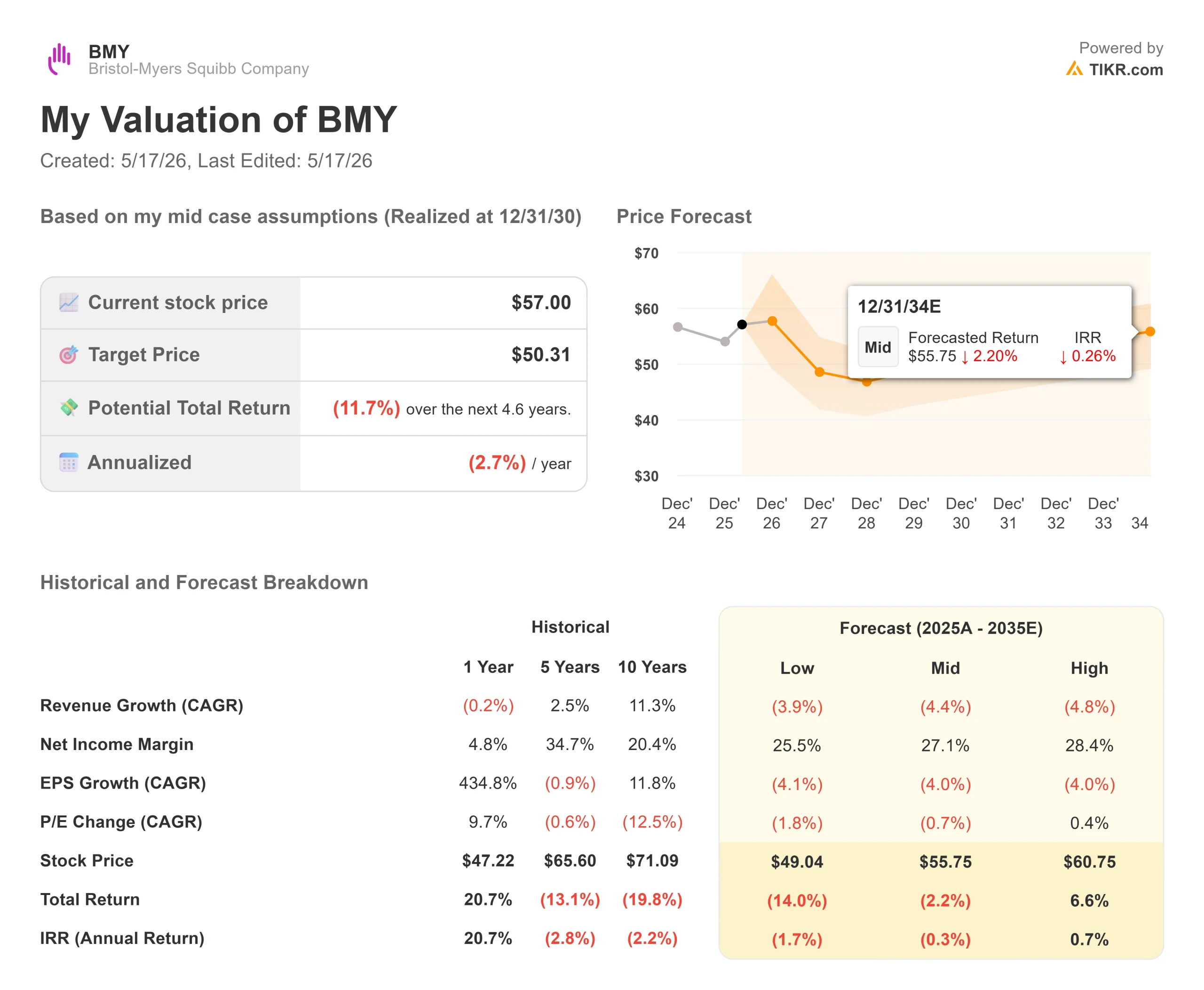

The TIKR model does not flatter the bull case in its mid-case scenario, which projects a target of around $50 by 12/31/30 a (11.7%) total return and (2.7%) annualized IRR from $57. The high-case scenario, implying around $61, is used here because it frames the right investment question: what has to go right?

The two revenue drivers in the high case are sustained double-digit growth across the core growth portfolio and at least one meaningful pipeline win, most plausibly Milvexian or COBENFY, in Alzheimer’s, contributing new revenue by 2029 or 2030. The margin driver is net income margins recovering to around 27% as acquisition-related amortization rolls off, per TIKR model assumptions. The primary risk is a milvexian miss or COBENFY Alzheimer’s failure; either scenario pushes the outcome toward the mid-case target.

The mid case is not a tail risk. It is what plays out if the pipeline simply does not deliver on schedule. The 4.5% dividend yield and FY2025 free cash flow of $12,845 million, per TIKR, provide a floor. But income alone does not justify owning BMY at $57 over a five-year horizon. The pipeline has to contribute.

Conclusion

The next six months will define more of BMY’s trajectory than anything management said at BofA. OCEANIC-AF milvexian data are expected by year-end 2026 per management. The threshold is specific: statistically significant bleeding reduction versus ELIQUIS, with a stroke hazard ratio close to 1. If milvexian clears that bar, the ELIQUIS succession story becomes a near-term commercial reality, and the multiple has room to expand. If the hazard ratio comes in unfavorably, even within an approvable range, commercial uptake narrows sharply to high-bleed-risk subgroups, and the long-term revenue case weakens considerably.

Watch the milvexian readout. Not just the headline. The forest plot.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Bristol-Myers Squibb?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Bristol-Myers Squibb, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Bristol-Myers Squibb alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Bristol-Myers Squibb on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!