Key Stats for Lattice Semiconductor Stock

- 52-Week Range: $44 to $130

- Current Price: $120

- Street Mean Target: $145

- Street High Target: $175

- Analyst Consensus: Buy (9 Buys, 3 Outperforms, 1 Underperform)

- TIKR Model Target (Dec. 2030): $404

Lattice Semiconductor Stock Surges After $1.65 Billion AMI Deal and a 42% Revenue Beat

Lattice Semiconductor (LSCC), a designer of low-power, reprogrammable field-programmable gate arrays (FPGAs) used in AI servers, data centers, and industrial automation, delivered a transformational quarter following its May Q1 2026 earnings report and a simultaneous $1.65 billion acquisition announcement.

Q1 revenue reached $170.9 million, a 42.2% year-over-year increase that cleared analyst expectations of $164.9 million, with Compute and Communications revenue up 86% year-over-year to $106.6 million.

Adjusted EPS came in at $0.41, beating the $0.37 consensus estimate by 11% and representing 86% growth over the year-ago period, a pace that management attributes to the operating leverage embedded in a fabless semiconductor model.

The companion deal, a $1.65 billion cash-and-stock acquisition of AMI (formerly known as American Megatrends), a firmware and infrastructure management software firm, nearly doubles Lattice’s serviceable addressable market from roughly $6 billion to around $12 billion according to CEO Fouad Tamer on the Q1 2026 earnings call.

Fouad Tamer stated on the Q1 2026 earnings call that “AMI’s expertise in firmware and infrastructure for cloud and AI is a natural extension of our portfolio, deepening our role in system-level security, manageability, and control,” directly linking the deal to Lattice’s everywhere companion chip strategy.

The combined platform spans low-power FPGAs, BIOS firmware, baseboard management controllers (BMCs), and post-quantum cryptography (PQC) tools, positioning Lattice Semiconductor stock as a full-stack play on AI infrastructure security and control rather than a point-solution chip vendor.

Q2 guidance calls for revenue of $175 million to $195 million at the midpoint of $185 million, representing nearly 50% year-over-year growth, alongside non-GAAP EPS of $0.42 to $0.46 and non-GAAP gross margins of 70% plus or minus 1%.

Wall Street’s Take on LSCC Stock

Wall Street is not debating whether Lattice Semiconductor is growing — the 42% revenue print and 86% EPS growth settled that — it is debating how far the re-rating has to run.

The thesis the Street is pricing: Lattice is transitioning from a point-solution FPGA vendor into a system-level platform company, with the AMI acquisition adding firmware orchestration and management software that neither pure-play FPGA vendors nor large-scale ASIC makers can replicate at comparable cost and speed.

Consensus EPS Normalized for calendar Q2 2026 sits at $0.44, growing to $0.47 in Q3 and $0.50 in Q4, putting annualized 2026 EPS on a trajectory toward roughly $1.88 — representing around 85% growth over the 2025 base.

Revenue consensus calls for $185.5 million in Q2 2026, $194.5 million in Q3, and $202.7 million in Q4, a cadence that sustains roughly 40% to 50% year-over-year growth across every remaining quarter of 2026.

Thirteen analysts cover Lattice Semiconductor stock, with 9 Buy ratings, 3 Outperforms, and 1 Underperform, placing the bullish-to-cautious ratio at 12-to-1 and leaving virtually no room for doubt about the directional consensus.

The mean Street price target has moved from $91 at the end of Q4 2025 to $145today, a 60% upward revision in roughly one quarter, with the high target reaching $175, implying that the most bullish analysts see a further 46% upside from the current price.

Trading at 62x NTM P/E against a historical mean of 49x, Lattice Semiconductor stock appears fairly valued: the premium to its own average is real, but consensus EPS growth above 85% through 2026 and bookings well into 2027 justify the elevated multiple.

The Q2 earnings call, expected in early August, is the next binary event to watch — specifically whether AMI closes on schedule in Q3 and whether management raises the $1 billion annual revenue run rate target for Q4.

Lattice Semiconductor’s Income Statement Shows a Business Snapping Back at Pace

Lattice Semiconductor posted Q1 2026 revenue of $170.9 million, up 42.2% year-over-year, the fastest growth rate the company has recorded since its inventory correction began in mid-2024, with operating income reaching $26.67 million, a 244% year-over-year increase from $7.75 million in Q1 2025, as operating margins expanded to 16% from 6% in the year-ago period.

The driver is a combination of revenue scale and disciplined cost structure: total operating expenses fell to $91 million in Q1 2026 despite an 18% year-over-year increase in R&D to near $51 million, because non-recurring SG&A items that inflated prior quarters have normalized.

The trajectory sharpens the argument: operating margins had compressed from 20% in Q2 2024 to a trough of negative 0.6% in Q3 2025 before recovering to 1.8% in Q4 2025 and surging to 16% in Q1 2026, a reversal that reflects not a one-quarter bounce but a genuine inflection tied to the Compute and Communications revenue ramp.

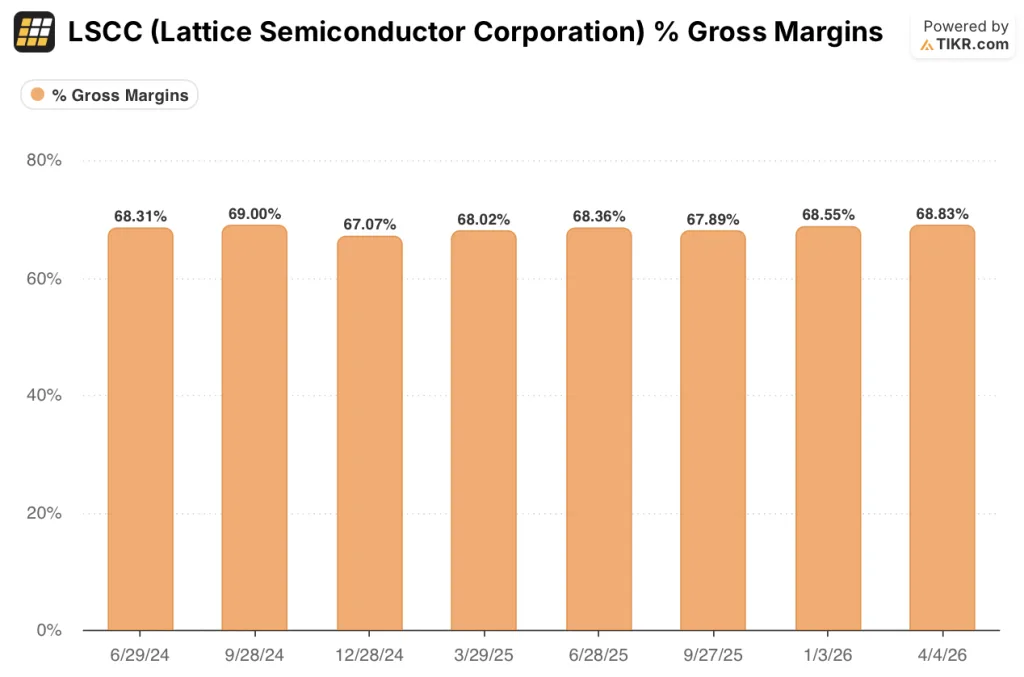

Meanwhile, LSCC’s gross margin held at 69% in Q1 2026, consistent with the 68% to 69% range across the prior six quarters, suggesting that the operating leverage story here is cost-line discipline rather than pricing-power-driven gross margin expansion — a structural advantage that scales with volume.

What Does the Valuation Model Say?

TIKR’s base case values Lattice Semiconductor at around $404 per share by December 2031, anchored to a 25% revenue CAGR through 2035 and net income margins expanding to 36%, inputs supported by the AMI acquisition’s immediate EPS accretion and the company’s accelerating AI data center attach rates.

At 62x NTM P/E against a historical mean of 49x, Lattice Semiconductor stock appears fairly valued near-term, but TIKR’s base case of around $404 implies a 230% annualized return over 5 and a half years for investors with a longer time horizon.

The central tension here is timing, not direction: whether the $1 billion annual revenue run rate materializes in Q4 as guided, or slips to Q1 2027 based on AMI integration complexity.

Bull Case:

- Compute and Communications revenue reaching over 60% of total 2026 revenue as FPGA attach rates per AI server move from roughly 3 units toward a higher range driven by new rack boot, power, and cooling applications

- AMI closes in Q3 2026 on schedule, immediately adding over $200 million in high-gross-margin software revenue to the run rate

- Channel inventory dropping below 2 months enables Industrial and Embedded revenue to inflect materially in 2027, adding a second growth leg that comps against weak 2025 industrial demand

- EPS consensus growing from $0.41 in Q1 2026 to around $0.50 by Q4 2026, a 22% sequential acceleration that re-rates the multiple upward

- Bookings extending well into 2027 de-risk near-term guidance cuts even if hyperscaler CapEx moderates

Bear Case:

- The stock already trades at around 69x NTM EPS after a 70% year-to-date move, leaving little margin for error if AMI integration disrupts Q3 or Q4 execution

- Supply chain cost pressure on back-end assembly and test could compress gross margins below the 69% to 70% guided range in H2 2026

- Double ordering risk: with lead times extending, some portion of the strong bookings may reflect buffer stock behavior rather than genuine end demand

How did Lattice Semiconductor perform in Q1 2026 earnings?

Lattice Semiconductor reported Q1 2026 revenue of $170 million, up 42% year-over-year and above the $165 million analyst consensus. Adjusted EPS came in at $0.41, beating estimates of $0.37 by 11% and representing 86% growth over Q1 2025.

Compute and Communications revenue reached $106.6 million, up 86% year-over-year, driven by AI server demand.

The company simultaneously announced a $1.65 billion acquisition of AMI, targeting a $1 billion annual revenue run rate by Q4 2026.

Is Lattice Semiconductor stock a buy right now?

TIKR’s base case values LSCC at around $404 per share by December 2031, implying roughly 236% total return from the current price of $120.

The Street’s mean target of around $145 already implies 21% near-term upside before AMI’s contribution is fully reflected.

The key variable is AMI integration: if the deal closes on schedule in Q3 2026 and the combined entity exits 2026 at a $1 billion annual revenue run rate, the TIKR base case likely holds.

If integration delays or supply chain cost pressure compress margins below 69%, the timeline shifts.

Should You Invest in Lattice Semiconductor Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lattice Semiconductor Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lattice Semiconductor Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LSCC stock on TIKR for Free →