Key Stats for Alibaba Stock

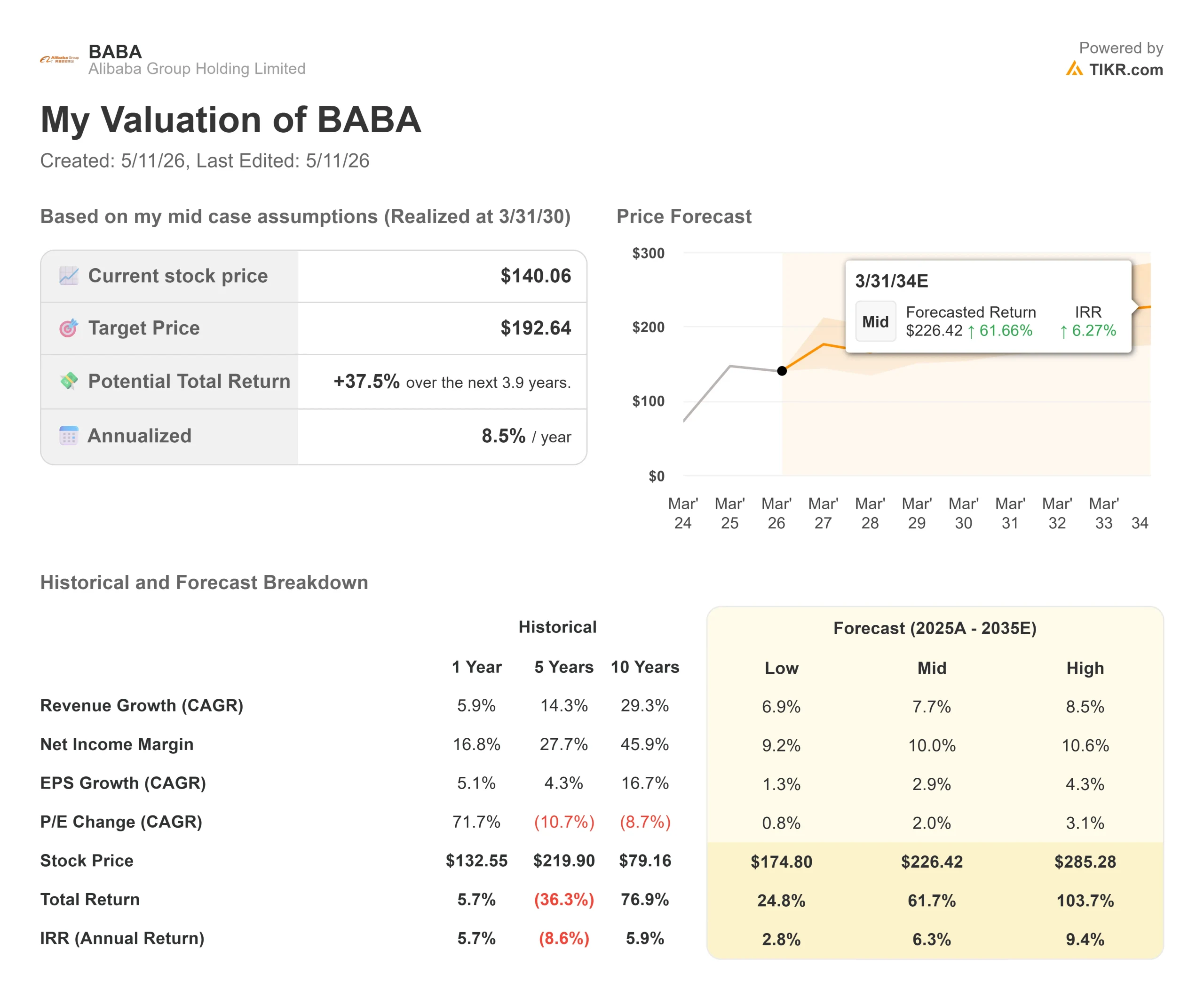

- Current Price: $138.19

- TIKR Model Entry Price: $140.06

- Target Price (Mid): ~$193

- Street Target: ~$189

- Potential Total Return: ~38%

- Annualized IRR: 8.5% / year

- Earnings Reaction (Q3 FY26, reported 3/19/26): -1.99%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alibaba (BABA) is trading about 28% below its 52-week high of $192.67, and the mood heading into Wednesday’s Q4 FY26 report is uneasy. Bulls point to a cloud business accelerating at its fastest rate in years and a $100 billion AI revenue target that CEO Eddie Wu laid out with unusual specificity on the March earnings call. Bears point to collapsing near-term profits, a geopolitical overhang that has erased billions in market cap without warning twice already this year, and a chip smuggling probe that broke three days before earnings. The central question is whether the AI investment cycle is building something durable, or burning cash for a payoff that keeps moving out.

A New Headline, Three Days Before Earnings

On May 8, Bloomberg reported that U.S. authorities suspect advanced Nvidia chips were smuggled to China through a Bangkok-based company called OBON Corp., with Alibaba named as one of multiple suspected end customers. The report, confirmed by Reuters, ties to a March 2026 Department of Justice indictment against Super Micro co-founder Yih-Shyan Liaw for allegedly routing AI servers through Southeast Asia to evade U.S. export controls. The indictment does not name Alibaba. U.S. authorities have not publicly accused the company of any wrongdoing. Alibaba’s response was unambiguous: “Alibaba has no business relationship with Super Micro, OBON or any third-party brokers who may have been mentioned in the indictment in question. We have no involvement in the alleged smuggling activities.”

This follows the February incident when the Pentagon briefly added Alibaba to its 1260H list of alleged military-linked companies, then withdrew it the same day. The stock fell around 3% in Hong Kong before any facts emerged. The pattern is clear: headline risk on BABA moves first, resolves later.

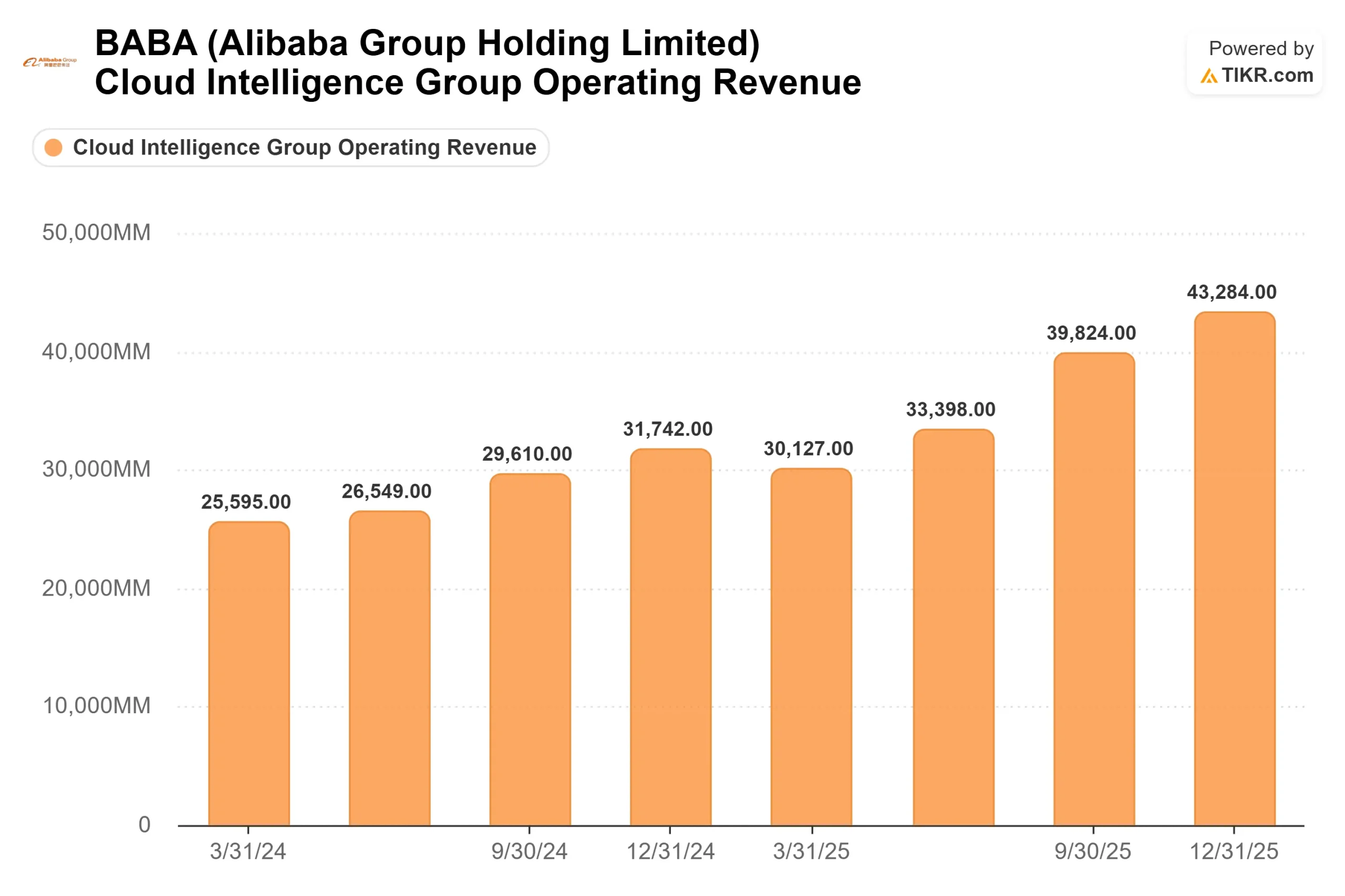

According to TipRanks’ options pricing data, traders are pricing an implied move of about 7.35% in either direction following Wednesday’s release. The direction will be set primarily by what Cloud Intelligence Group reports.

What Management Told Investors in March

The Q3 FY26 earnings call, held March 19, contained the clearest AI strategy articulation Alibaba has offered in years, and it is essential context for reading Wednesday’s numbers.

CEO Eddie Wu argued that enterprises are no longer treating token consumption, the basic unit of AI compute, as an IT expense. They are treating it as a production input, meaning demand scales with business activity rather than with IT budget cycles. That distinction, if it holds, dramatically expands the ceiling for Alibaba Cloud. Wu stated on the call: “Over the next 5 years, our goal is to surpass USD 100 billion in combined cloud and AI external revenue, including MaaS.”

MaaS, or Model-as-a-Service, means selling AI inference capabilities to enterprise customers rather than building proprietary end applications. Wu named three growth drivers: MaaS as the primary engine, private enterprise AI infrastructure deployment as a second market, and the transformation of traditional CPU-centric cloud into agent-optimized infrastructure as a third.

To organize around this, Alibaba created the Alibaba Token Hub Business Group (ATH), which unifies the Qwen model family, the Wukong enterprise agent platform, and consumer AI applications. The goal is tight integration between model development and application deployment, something Wu said separate business units could not achieve.

The Q3 numbers behind the strategy were strong in cloud and under pressure everywhere else:

- CFO Xu confirmed $42.5 billion in net cash as of December 31, 2025

- Cloud Intelligence Group external revenue grew 35% year over year, up from 29% the prior quarter, per CFO Toby Xu on the Q3 call

- AI-related product revenue delivered triple-digit growth for the tenth consecutive quarter.

- Per management, Alibaba Cloud’s domestic market share reached 36% and grew for three consecutive quarters.

- Qwen surpassed 300 million monthly active users

- T-Head, Alibaba’s proprietary AI chip unit, had shipped 470,000 chips as of February 2026, with annual revenue reaching the RMB 10 billion level, per CEO Wu on the call

- Quick commerce revenue grew 56% to RMB 20.8 billion, but China E-commerce Group’s adjusted EBITA fell 43% as Alibaba invested heavily to compete in instant delivery.

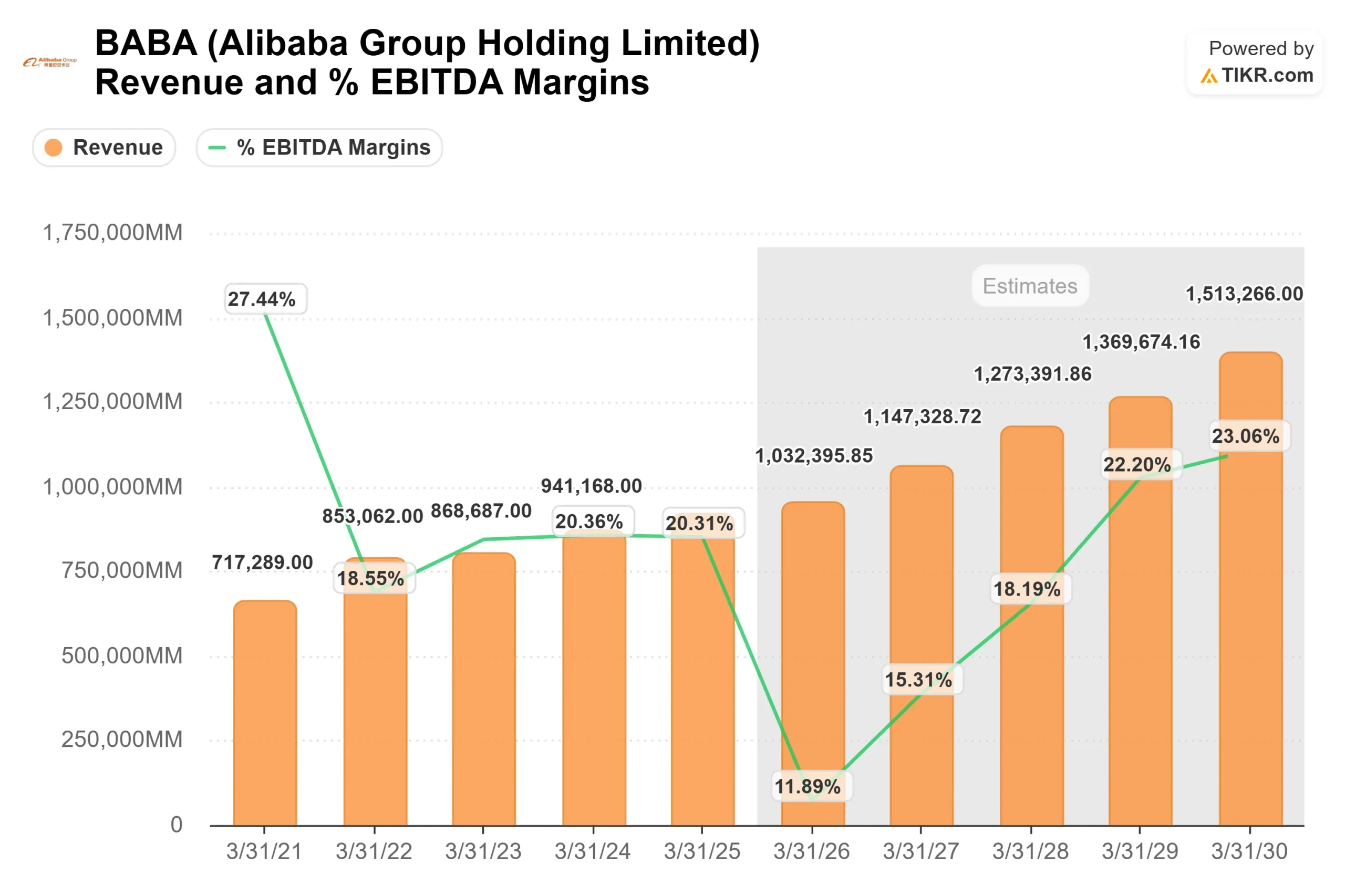

- GAAP net income fell 66% and adjusted EBITA fell 57%, both driven by deliberate investment in AI infrastructure and quick commerce

See historical and forward estimates for Alibaba stock (It’s free!) >>>

What Wednesday Needs to Show

Two things matter on May 13. First, cloud growth needs to hold or accelerate any deceleration back toward 25-29% reframes the story from a productive investment cycle to margin sacrifice with uncertain payoff. Second, quick commerce losses need to show a credible narrowing path toward management’s FY29 profitability target.

At $138.19, BABA trades at 22.08x NTM P/E and 13.67x NTM EV/EBITDA, per TIKR data. That multiple reflects the full weight of margin compression, negative trailing free cash flow, and the persistent geopolitical discount on Chinese tech. TIKR consensus projects free cash flow margins recovering to around 14% by FY30. That recovery is backend-loaded and requires the cloud investment thesis to execute.

Of 46 analysts covering BABA on TIKR as of May 8, 31 carry Buy ratings, 8 Outperform, 2 Hold, and 1 Underperform. The mean Street target stands at around $189, roughly 37% above the current price, one of the wider gaps between consensus and price BABA has seen in recent years.

See how Alibaba performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price (model entry): $140.06

- Target Price (Mid): ~$193

- Potential Total Return: ~38%

- Annualized IRR: 8.5% / year

See analysts’ growth forecasts and price targets for Alibaba stock (It’s free!) >>>

The mid-case uses an approximately 8% revenue CAGR and a 10% net income margin. The two revenue drivers are Cloud Intelligence Group, where external revenue is accelerating as AI monetization scales, and China e-commerce, expected to stabilize as quick commerce investment peaks around FY28. The margin driver is T-Head chip integration into Alibaba’s own cloud infrastructure, which management has tied directly to lower inference costs. The primary risk is timing: if cloud growth decelerates before profit margins recover, the earnings timeline extends beyond what the current multiple prices in.

Conclusion

Watch Cloud Intelligence Group’s total revenue growth rate on May 13. If it holds at 35% or better, the margin recovery thesis gains credibility and Alibaba’s $100 billion five-year target shifts from ambition to early trajectory. If it decelerates meaningfully, the story becomes a long capex cycle with a delayed payoff. The chip allegation is a genuine overhang, but no formal U.S. action has been taken against Alibaba, and the company has denied any involvement. Cloud growth is the fundamental test. Alibaba has the infrastructure, the models, and the cash to execute. Wednesday shows whether the execution is keeping pace.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alibaba?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alibaba, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alibaba alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alibaba on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!