Key Takeaways:

- Phillips 66 offers a forward dividend yield of 3.7%, and management is expected to continue growing the dividend and buying back shares.

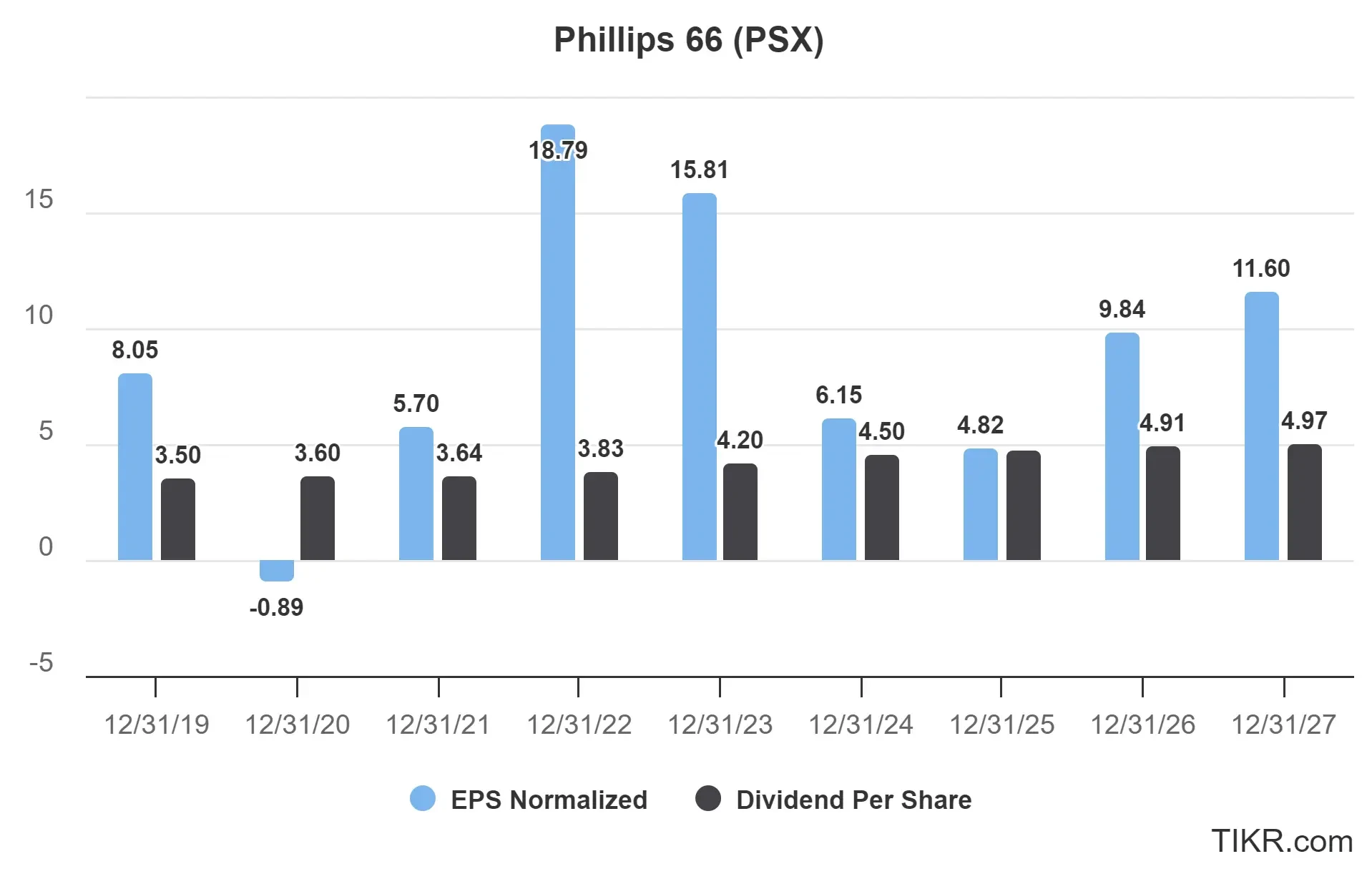

- Earnings are expected to rise over 100% in 2026 to a more normal level.

- Based on current price targets, analysts see about 4% upside for the stock, and the dividend yield boosts total returns.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Dividend investors don’t always look to the energy sector, but Phillips 66 (PSX) could be worth a closer look.

The stock offers a 3.7% forward dividend yield, steady buybacks, and analysts expect the business to see a major earnings rebound in 2026.

While near-term upside may be limited, the dividend helps boost total returns, and the company’s long-term commitment to shareholders makes it a stock to watch.

Why Is $PSX Stock Down 20% From Its 2024 High?

Phillips 66 traded near $160/share in early 2024 but has since dropped to around $124/share. Here’s why the stock has pulled back:

- Refining Margins Have Normalized: The post-COVID spike in crack spreads (the difference between the price of crude oil and the price of the petroleum products refined from it) has faded. Investors now expect more moderate refining profits going forward.

- Weak Chemical Segment: The company’s chemicals joint venture, CP Chem, has struggled with lower polyethylene prices, which have put pressure on segment earnings.

- Lower Utilization Rates: Several of Phillips 66’s refineries have experienced downtime or lower utilization in recent quarters, limiting output and reducing short-term earnings potential.

Despite recent headwinds, Phillips 66 could still be a solid long-term investment due to a likely rebound in refining margins over the next few years.

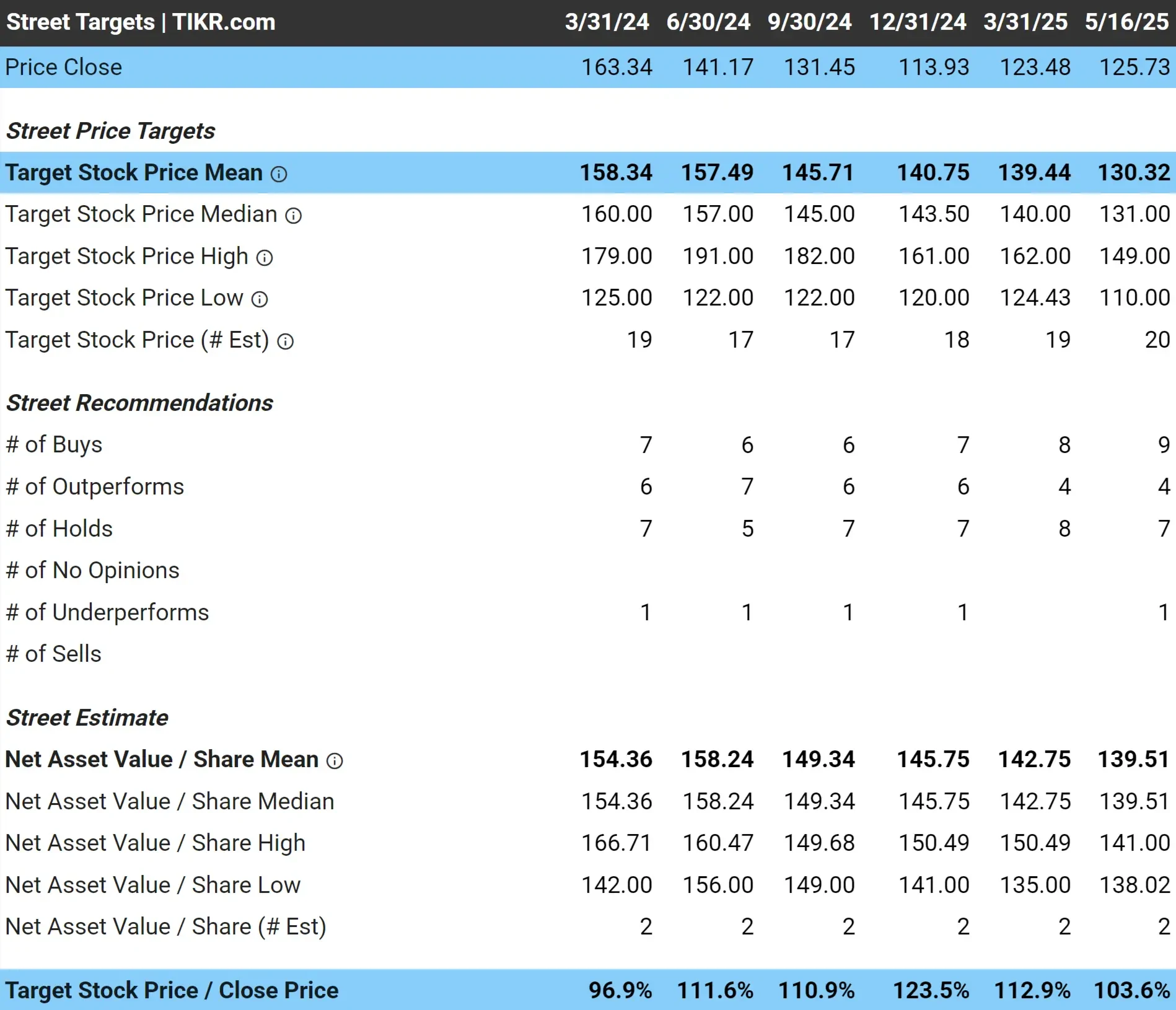

Analysts See Nearly 4% Upside (Not Including Dividends)

Phillips 66 stock trades around $126/share, while Wall Street analysts have an average 18-month price target of $130/share.

That implies roughly 4% upside for the stock. That’s not a lot of upside today, but it also doesn’t account for the stock’s 3.7% dividend yield, pushing the total return potential slightly higher.

If the stock price continues to dip, Phillips 66 could be a really interesting long-term opportunity.

Find stocks that are more undervalued than Phillips 66 today with TIKR (It’s free) >>>

1: Dividend Yield

Phillips 66 currently offfers a forward dividend yield of about 3.7%.

Over the past five years, PSX’s dividend yield has ranged from a low of 2.5% to a Covid-induced high of 8.2%, with a long-term average of around 4.3%.

That puts today’s yield just slightly below its five-year average, which suggests the stock may still be reasonably valued from a dividend yield perspective.

Management is continuing to raise the dividend, signaling confidence in the company’s ability to generate consistent free cash flow, even as refining margins normalize.

See Phillips 66’s full dividend stats with TIKR. (It’s free) >>>

2: Dividend Safety

For 2025, Phillips 66 is expected to earn $4.82 in normalized earnings per share while paying out $4.50 in dividends per share. This means the stock will have a dangerously high dividend payout ratio of around 93% for 2025. We like to see stocks paying out less than 70% of their earnings as dividends.

However, by 2026, earnings per share are expected to rebound to $9.84, so analysts expect the company to easily cover dividend payments going forward.

The company’s net debt-to-EBITDA is a bit high at 4.5x (we prefer under 3x), but with earnings expected to grow in 2026 and beyond, Phillips 66 should have enough financial flexibility to reinvest in the business, buy back stock, and keep raising its dividend.

See Phillips 66’s full growth forecast and analyst estimates. (It’s free) >>>

3: Dividend Growth Potential

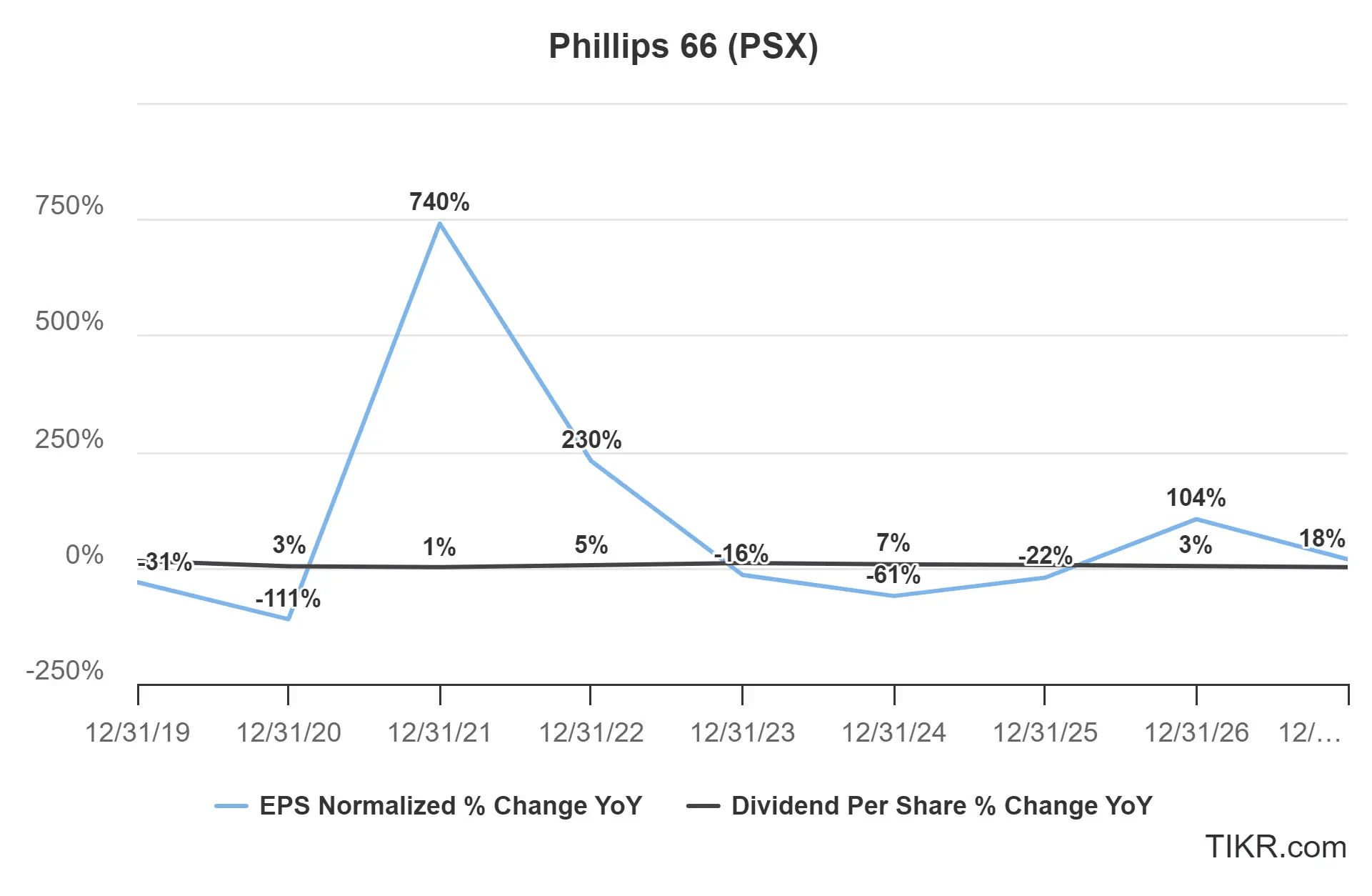

Phillips 66 has kept raising its dividend even when earnings were down. In 2023, earnings fell 16%, but the dividend still went up 10%. In 2024, earnings dropped over 60%, yet the dividend rose another 7%.

Looking ahead, analysts see earnings more than doubling in 2026 and growing 18% in 2027. Dividend growth is expected to average around 3% a year over the next 3 years.

This consistent trend highlights Phillips 66’s commitment to rewarding shareholders, even during earnings volatility. With earnings set to recover meaningfully, the company has plenty of room to keep raising its dividend in the years ahead.

TIKR Takeaway

Phillips 66 offers a relatively high dividend yield, a strong commitment to share buybacks, and earnings are expected to increase dramatically in 2026.

For investors building a long-term dividend portfolio, Phillips 66 stock could be worth adding to your watchlist and buying on dips.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!