Key Takeaways:

- Enbridge currently offers a high 6.1% forward dividend yield.

- It has raised its dividend for 30 consecutive years and plans to keep growing it alongside distributable cash flow.

- Enbridge stands out as a dependable income pick thanks to its stable cash flows and regulated, inflation-linked contracts.

- It’s a strong candidate for any dividend-focused portfolio and is worth keeping on your watchlist for potential buying opportunities.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Enbridge is widely known for its role in North America’s energy infrastructure, but it has also become a dependable dividend stock over the years.

Enbridge operates over 17,800 miles of liquids pipelines and 76,000 miles of natural gas transmission, backed by steady cash flow from regulated contracts. That makes it a stable, long-term dividend payer and a potential buy-and-hold pick for patient investors.

Why Is ENB’s Stock Up 20% in the Past Year?

Enbridge stock has quietly climbed 20% over the past 12 months, outpacing many peers in the energy sector. Here are some of the factors that have led to this strong performance:

- Strong Distributable Cash Flow Growth: Enbridge’s distributable cash flow increased by 6% year over year, giving investors confidence in the sustainability of its high dividend.

- Stability Amid Market Volatility: As a regulated utility-like business with long-term contracts, Enbridge attracted defensive capital during market uncertainty and rising rates.

- Major U.S. Gas Utility Acquisition: Investors reacted positively to Enbridge’s $14 billion acquisition of Dominion’s gas utility assets, expanding its footprint and future cash flow potential.

Analysts see Enbridge as a reliable long-term dividend payer that’s potentially undervalued today.

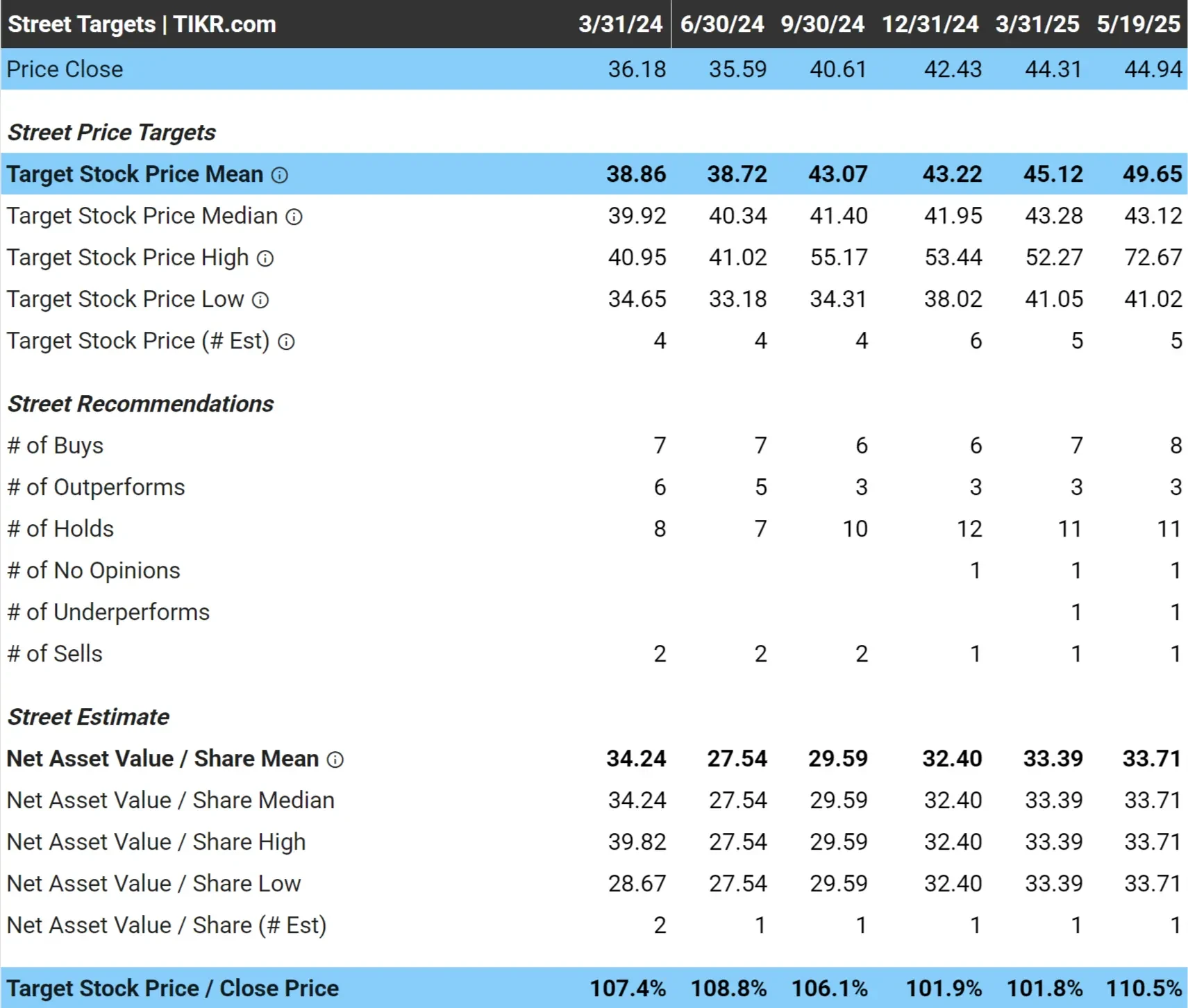

Analysts Think the Stock Has 10% Upside Today

Wall Street analysts currently have an average price target of $50/share for Enbridge, which implies that the stock has about 11% upside since it’s trading around $45/share as of May 19, 2025.

While that might seem like low upside, it’s worth noting that Enbridge is a stable, cash-generating infrastructure giant with one of the most reliable dividend track records in North America.

With a 5.7% dividend yield and inflation-protected cash flows, Enbridge could continue to deliver solid total returns for long-term dividend investors.

Find stocks that are more undervalued than Enbridge today (It’s free) >>>

1: Dividend Yield

Enbridge currently offers a forward dividend yield of 6.1%, slightly below its 5-year average of 6.9%.

The lower yield suggests the stock may be fairly valued at today’s price.

But with over 70 years of uninterrupted dividends and 30 years of consecutive dividend increases, Enbridge remains a reliable option for long-term dividend investors.

See Enbridge’s full dividend stats with TIKR. (It’s free) >>>

2: Dividend Safety

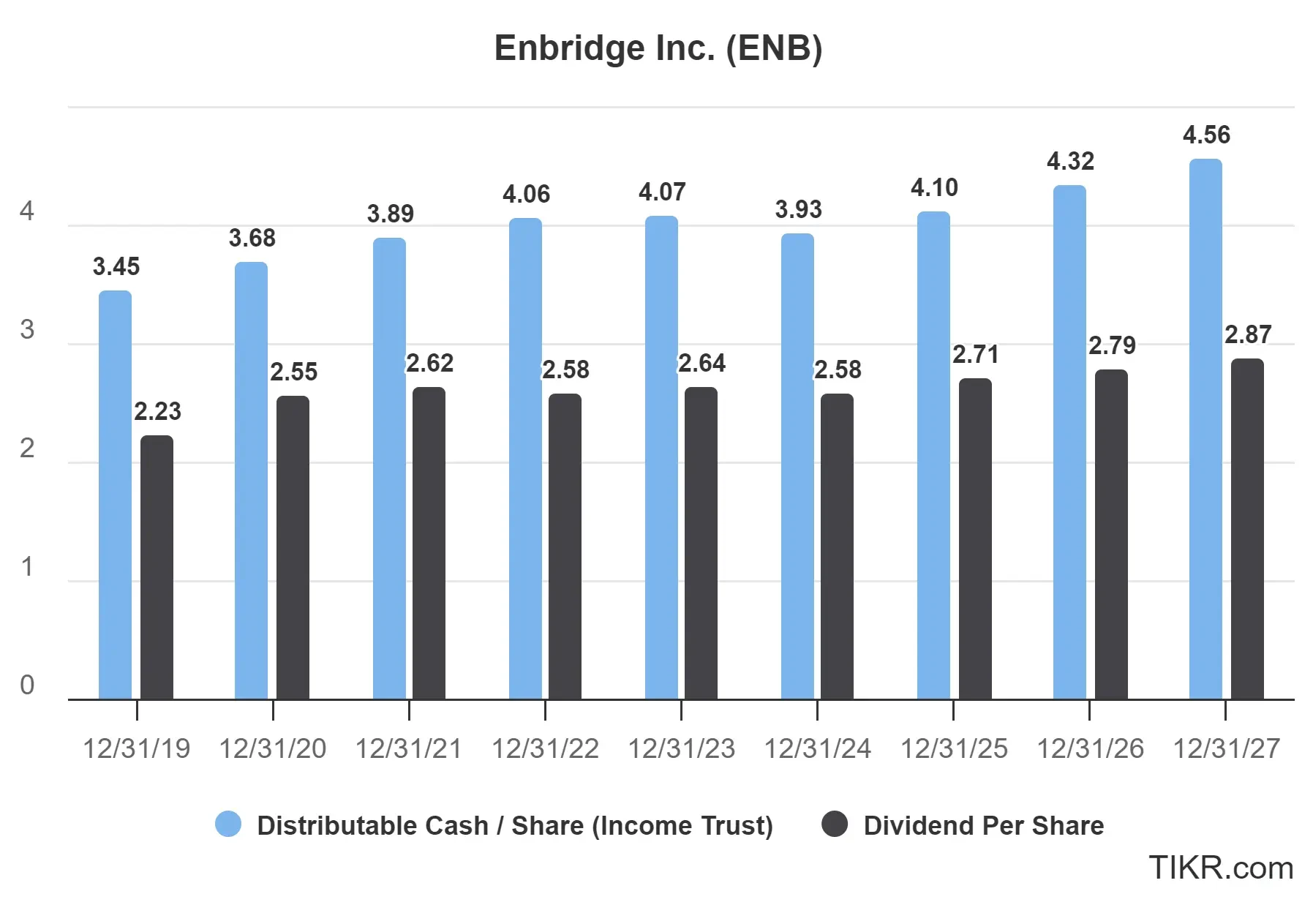

For 2025, Enbridge is projected to pay $2.71 per share in dividends while generating $4.10 in distributable cash per share, resulting in a dividend payout ratio of about 66%. That’s comfortably within the company’s target range of 60-70% of DCF.

Enbridge uses distributable cash per share as its preferred earnings measure, since it better reflects the company’s actual cash-generating power. Distributable cash is fairly similar to operating cash flow, and operating cash flow is basically net income with a couple of non-cash expense add-backs.

Enbridge is a Canadian company, so while dividends have been rising in Canadian dollars, they’ve occasionally declined in U.S. dollars due to currency fluctuations. Enbridge has raised its dividends for 30 consecutive years, and that streak is expected to continue.

Looking ahead, analysts expect both distributable cash and dividends to continue rising through 2027, with the payout ratio remaining in a healthy range.

See Enbridge’s full growth forecast and analyst estimates. (It’s free) >>>

3: Dividend Growth Potential

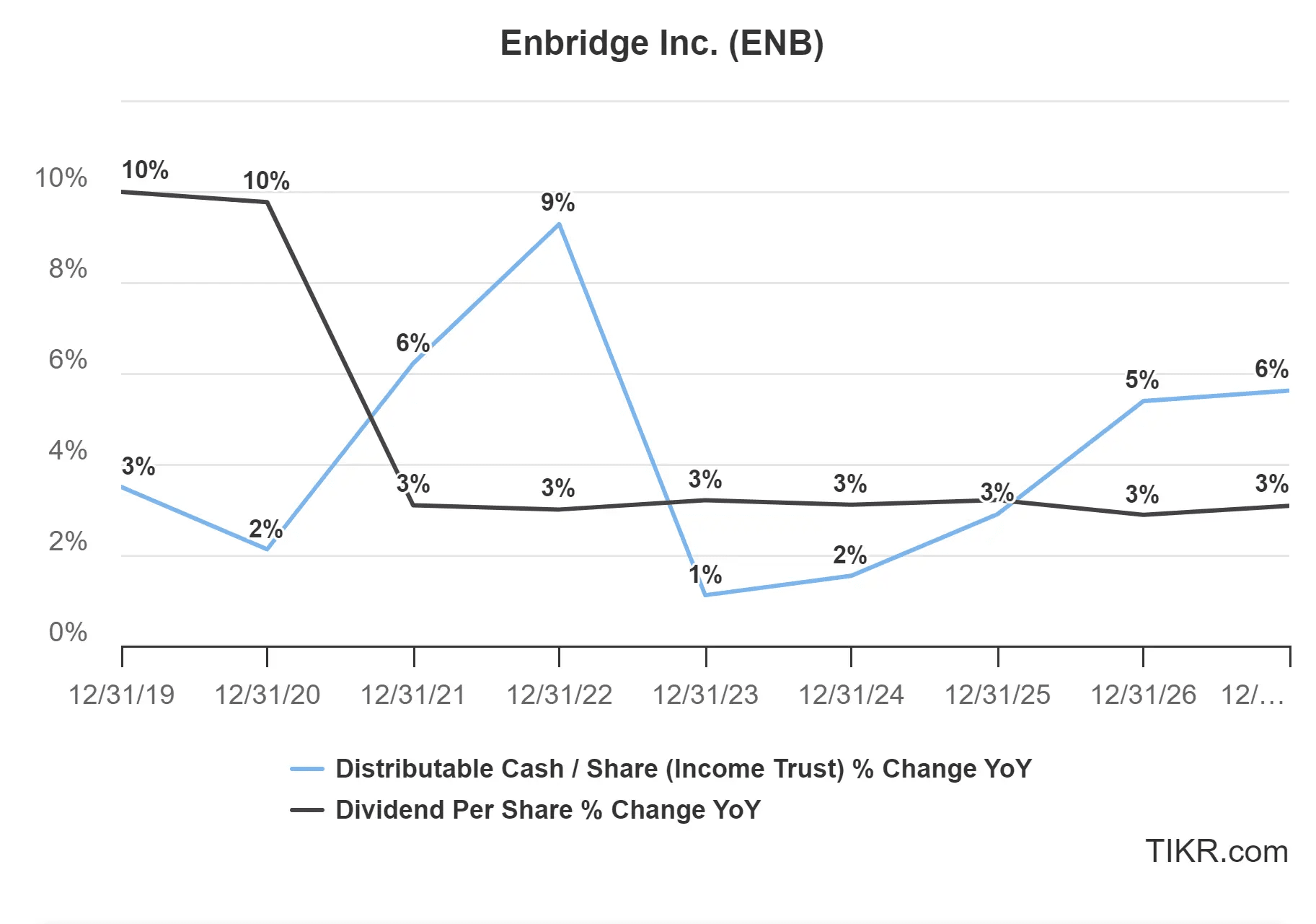

Over the past five years, Enbridge’s distributable cash has grown in the low-single-digits, with occasional strong performance. Dividend growth in US dollars slowed from about 10% annually to about 3% annually.

Over the next three years, distributable cash is projected to grow at a 4.6% compound annual growth rate, while dividends per share are expected to grow at a slower 3.1% CAGR.

That’s pretty healthy growth for a high-yield dividend stock, giving Enbridge room to continue growing and delivering long-term growth for shareholders.

TIKR Takeaway

Enbridge isn’t a fast-growing stock, but with essential infrastructure assets, stable cash flows, and a long history of dividend increases, it has the foundation to keep rewarding shareholders for years to come.

Even though analysts see limited upside today, it could be a solid dividend stock to buy and hold for investors seeking reliable dividend and long-term stability.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!