Key Takeaways:

- Lockheed Martin offers a 3.3% dividend yield, which is nearly the highest yield the stock has offered in the past 5 years.

- Despite a 20% drop in the stock price over the past year, analysts project 24% upside for the stock by 2027 based on steady earnings and conservative assumptions.

- Earnings are expected to grow around 4% annually, with dividends rising approximately 5% per year, supported by multi-year defense contracts and consistent global demand.

Lockheed Martin is one of the largest and most strategically important defense contractors in the world, supplying fighter jets, missile defense systems, satellites, and next-gen technologies like hypersonics to the U.S. and allied governments.

The stock has lagged recently, falling more than 20% over the past year due to margin pressures and a broader shift in investor interest away from defense.

But underneath the surface, Lockheed has kept doing what it does best: generating reliable earnings, delivering steady free cash flow, and raising its dividend with discipline.

At current prices, the stock doesn’t look deeply discounted, but the 3.3% yield is well above normal levels and backed by long-term government contracts.

With earnings expected to grow and cash returns remaining strong, Lockheed offers a dependable mix of income, stability, and upside potential.

For investors looking to own a high-quality name tied to national security, Lockheed continues to earn its place.

Analysts See 9.1% Annual Returns for Lockheed Through 2027

Lockheed Martin currently trades around $421/share, but based on analysts’ consensus estimates used in our guided valuation model, the stock could reach about $521/share by the end of 2027.

That implies total returns of 23.6%, or roughly 9.1% annually, if the company delivers 4.1% annual revenue growth and maintains operating margins around 11.5%.

This projection assumes a forward P/E of 15.3x, which is slightly below Lockheed’s 5-year average of 16.2x.

With strong cash flow, consistent demand from global defense contracts, and growing exposure to high-tech programs, analysts believe today’s price could represent an attractive long-term entry point.

Value any stock in less than 60 seconds with TIKR (It’s free) >>>

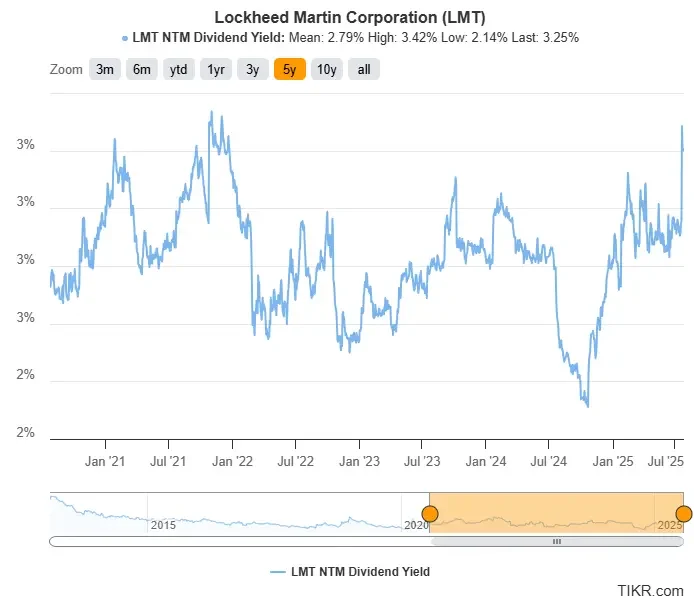

Lockheed’s 3.3% Yield Approaches 5-Year High

Lockheed Martin’s current 3.3% dividend yield stands out not because of business weakness, but due to a stock price pullback while fundamentals remain strong. The yield currently sits near its 5-year high of 3.4%.

The company continues to post steady earnings, generate consistent free cash flow, and secure long-term revenue from multiyear defense contracts.

This disconnect between valuation and business quality has made the yield more attractive than usual.

With geopolitical tensions keeping demand high and government budgets largely intact, Lockheed’s ability to return capital remains solid.

For investors looking to lock in quality businesses with dividend yields backed by real-world demand and durable cash generation, this is one of the more compelling setups in today’s market.

Find high-quality dividend stocks that look even better than Lockheed Martin today. (It’s free) >>>

LMT Projects 4% EPS Growth, 5% Dividend Growth Through 2027

Lockheed Martin is expected to earn $21.88 per share in 2025 and $31.47 by 2027, while paying out $13.29 and $14.75 in dividends in those same periods.

That means the payout ratio would decline from an expected 61% in 2025 to 47% over the next 2 years, which means that analysts expect earnings to comfortably cover dividends.

From 2024 to 2027, analysts project earnings to grow at a steady rate of about 4% annually, while dividends are expected to rise around 5% per year through 2027. That consistent growth is backed by Lockheed’s long-term government contracts and high visibility into future revenue.

Earnings momentum is expected to be driven by continued deliveries of the F-35 fighter jet, growing demand for its PAC-3 missile systems, expanding space and satellite operations, and increased investment in defense-related AI and digital modernization programs.

Lockheed has raised its dividend for 22 consecutive years, backed by strong free cash flow, a healthy balance sheet, and durable demand from both U.S. and international defense budgets.

For long-term investors seeking stable income and consistent growth, Lockheed remains one of the most reliable names in the industrial sector.

See Lockheed Martin’s full growth forecast and analyst estimates. (It’s free) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!