Key Takeaways:

- EPD has a 6.8% forward dividend yield, and analysts expect earnings and dividends to grow in the mid-single digits going forward.

- EPD has raised its dividend for 28 years in a row.

- With steady cash flow, the company should be able to keep growing dividends for many years to come.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Enterprise Products is one of the largest and most dependable midstream energy companies in the U.S.

Midstream companies like EPD often make great high-yield dividend stocks because they generate steady cash flow by moving oil, gas, and natural gas liquids through pipelines under long-term, fee-based contracts. These agreements aren’t tied to commodity prices, which helps companies like EPD earn consistent revenue even when energy markets are volatile.

This strong, consistent free cash flow funds the company’s reliable high dividend yield.

With a long track record of raising distributions and managing risk conservatively, EPD continues to be a go-to name for income-focused investors. Today, the stock looks slightly undervalued and could be worth adding to on pullbacks.

Why Is $EPD’s Stock Up About 15% in the Past Year?

EPD shares have climbed about 15% over the past year, outperforming the broader market. Here’s what’s been driving the stock higher:

- Resilient cash flow from fee-based contracts: More than 80% of EPD’s gross operating margin comes from long-term, fee-based agreements. This helps protect earnings during commodity price swings and supports consistent cash flow across cycles.

- Rising demand for U.S. energy exports: US exports of natural gas liquids and crude oil are hitting record highs, and EPD is a key player in moving these volumes. Its extensive pipeline and terminal footprint gives it a strong position as global demand grows.

- Attractive yield in a high-rate environment: EPD offers a compelling forward dividend yield of 6.8%, which is attractive in the current high-interest-rate environment. This yield is backed by solid coverage and stable earnings, making it a reliable source of returns for income-focused investors.

The stock has become a standout for dividend-focused investors by combining stable cash flow, a high yield, and for the long-term growth drivers in U.S. energy infrastructure.

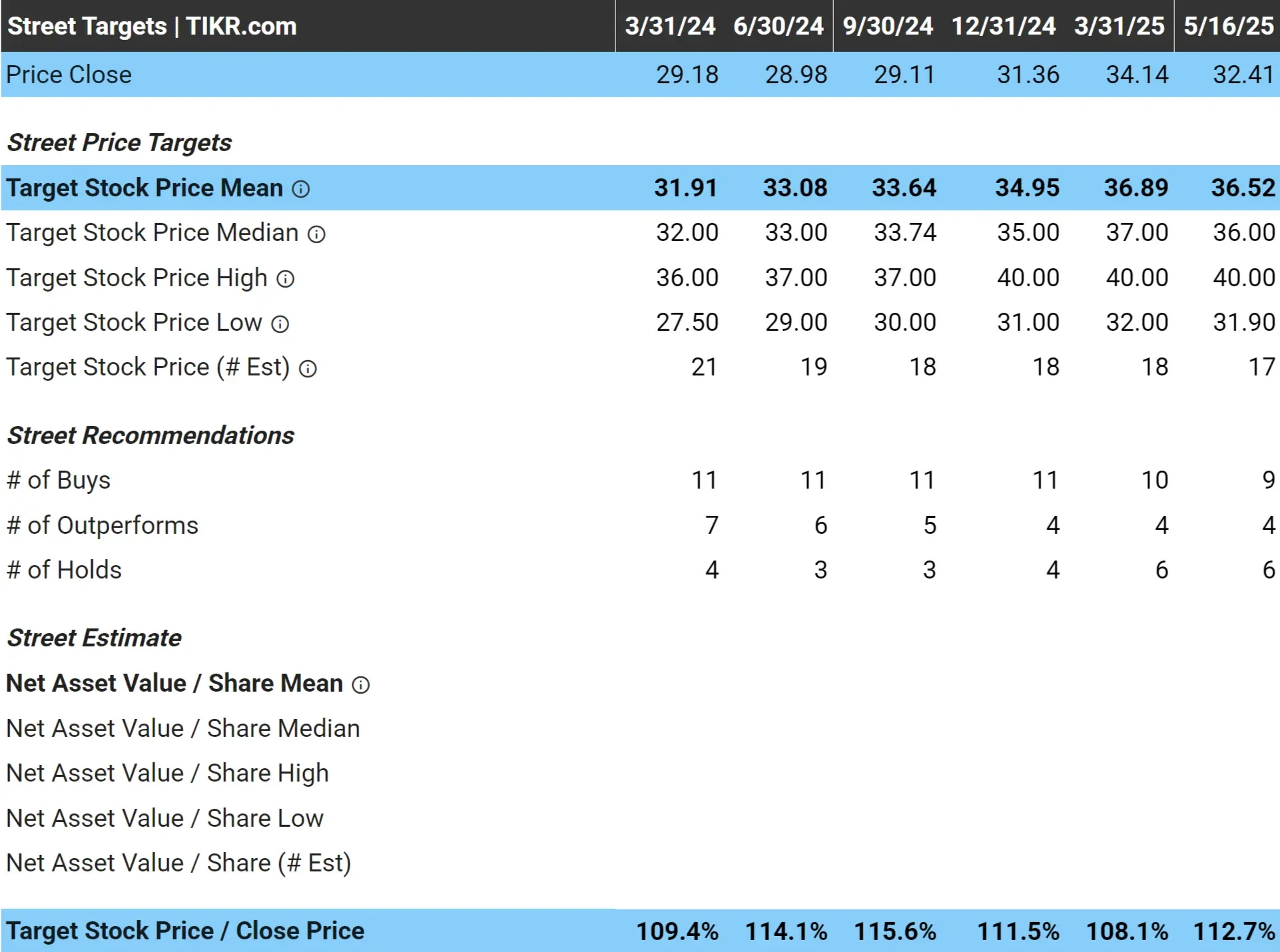

Analysts See Nearly 13% Upside (Not Including Dividends)

Wall Street analysts have an 18-month average price target of $37 for EPD, which implies the stock has about 13% upside from its current price of $32 today.

While 13% upside may not seem like much, this also doesn’t account for EPD’s 6.8% dividend yield. If you’re a high-yield dividend investor, it could make sense to add to the stock when it looks undervalued, because you’re still earning nearly a 7% dividend yield.

Find stocks that are more undervalued than Enterprise Product Partners today (It’s free) >>>

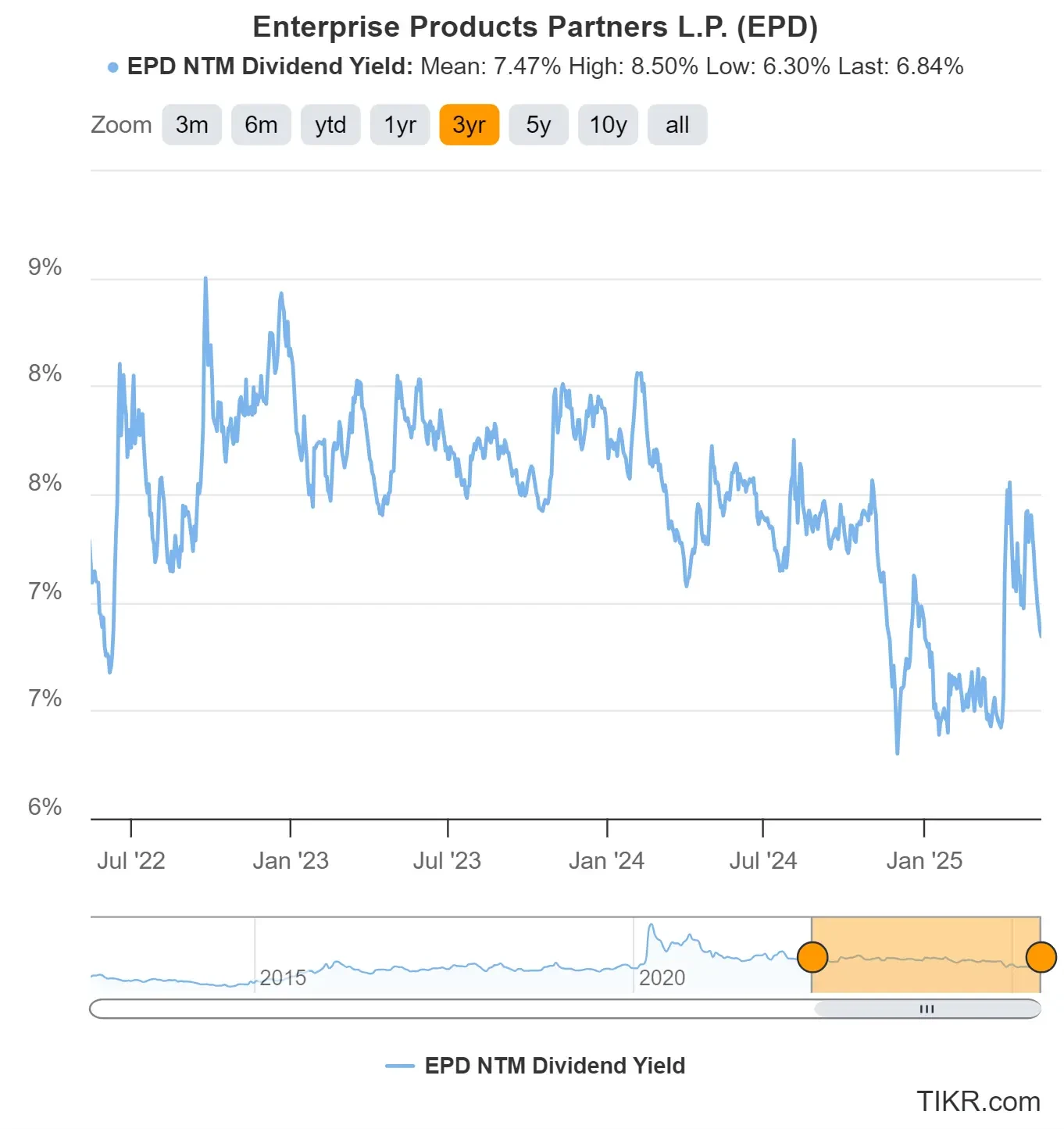

1: Dividend Yield

EPD currently offers a forward dividend yield of 6.8%, which is just below its 3-year average of 7.5%.

While the yield has come down in recent months due to the stock’s rise, it’s still well above the broader market average and reflects strong underlying cash flows. EPD has grown its distribution for 28 consecutive years, with increases expected to continue.

For high-yield dividend investors, this is still an attractive stock today.

See Enterprise Product Partner’s full dividend stats with TIKR. (It’s free) >>>

2: Dividend Safety

Despite the high yield, EPD’s dividend remains safe and well-covered.

In 2025, EPD is projected to generate $2.80 in normalized earnings per share while paying out about $2.18 in dividends. That means the stock is expected to have a dividend payout ratio of about 78%, which is reasonable for a mature energy infrastructure business.

We generally look for payout ratios below 70%, but in this case, the company’s strong and stable earnings make the current payout level still look safe.

EPD also has a conservative Net Debt/EBITDA leverage ratio of 3.3x (we prefer less than 3x, but EPD has consistent cash flows) for the past year and holds an A- credit rating, which further supports the company’s financial strength.

See Enterprise Product Partner’s full growth forecast and analyst estimates. (It’s free) >>>

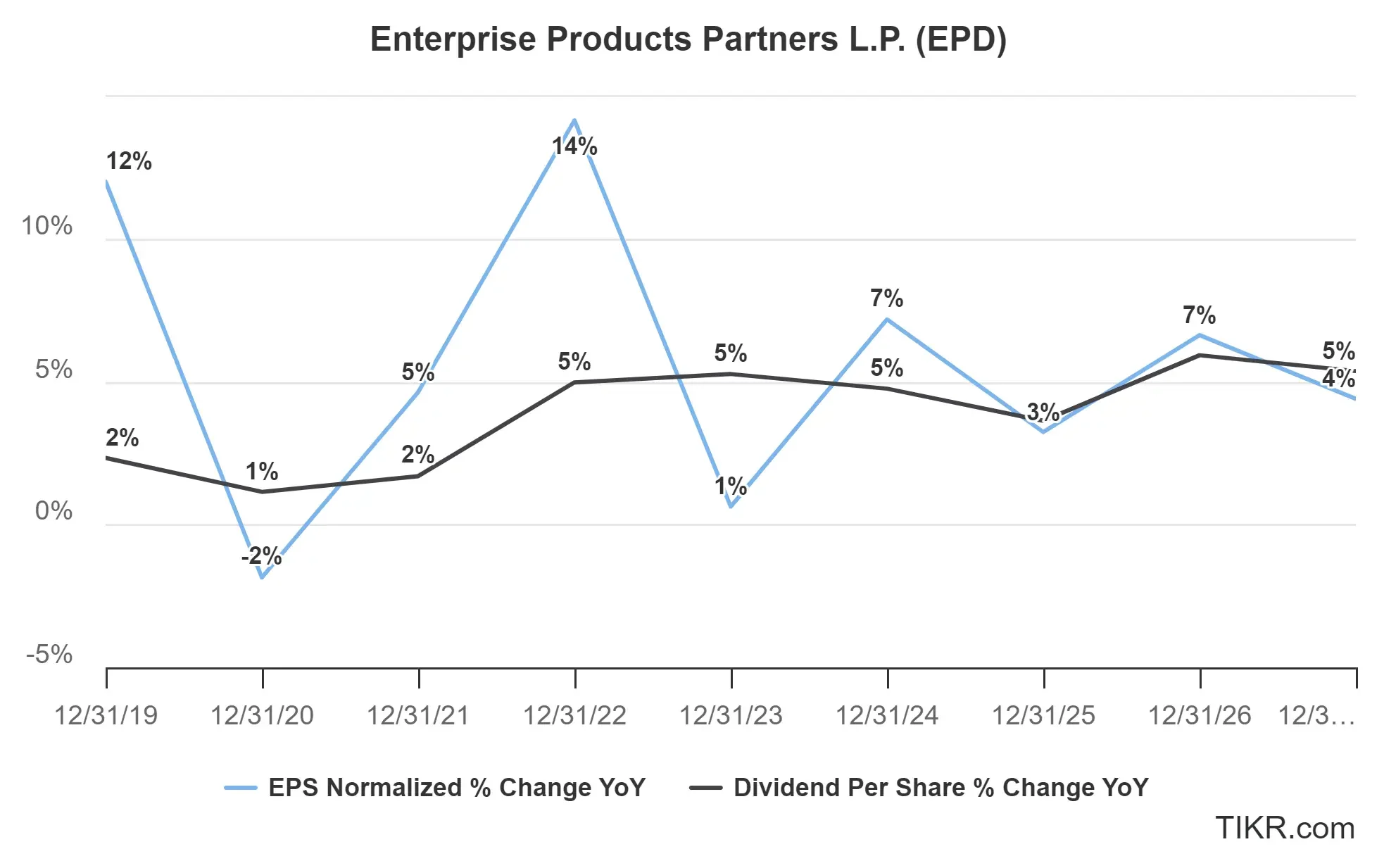

3: Dividend Growth Potential

Over the past five years, EPD has grown its dividend at a 3.5% compound annual growth rate, while earnings have increased at a 4.8% CAGR.

Looking ahead, analysts expect both earnings and dividends to keep growing at a mid-single-digit annual pace.

That’s a solid trajectory for a high-yield stock, and it reflects EPD’s disciplined capital return strategy, backed by stable, fee-based cash flow.

TIKR Takeaway

With a 6.8% forward dividend yield, stable cash flow backed by long-term contracts, and 28 consecutive years of dividend increases, EPD is built for consistent dividends and long-term reliability. The company remains one of the most dependable names in energy infrastructure.

For investors seeking a high-yield dividend stock with low volatility and solid total return potential, EPD continues to be a strong candidate.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!