Key Takeaways:

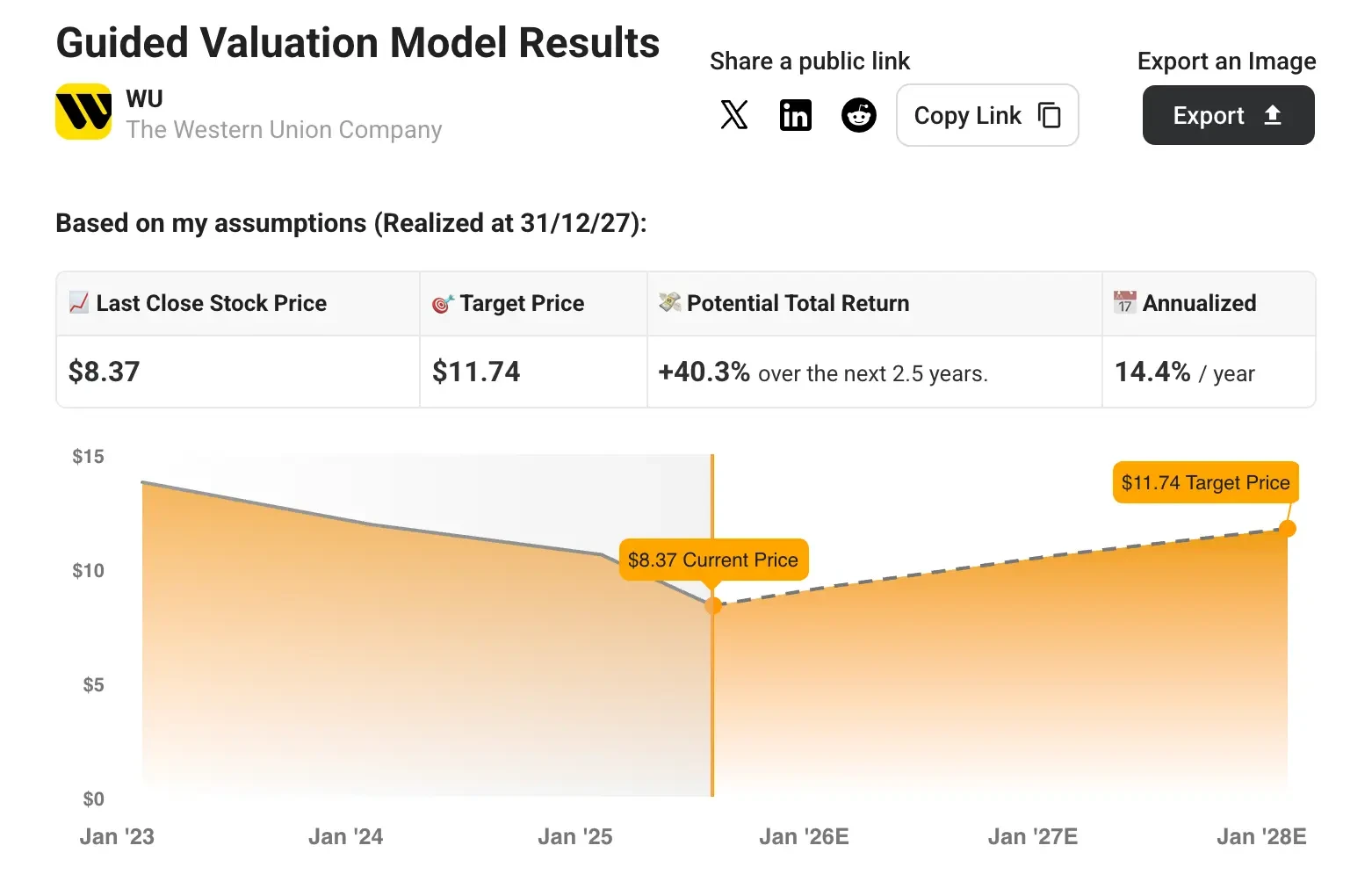

- Western Union stock could conservatively be worth over $11.74/share by the end of 2027.

- That’s a potential 40% upside from today’s price of ~$8.37/share.

- WU stock is projected to benefit from business stabilization and margin expansion as the company executes its Evolve 2025 transformation strategy.

- Unlock our Free Report: 5 stock screeners inspired by top investors like Warren Buffett to help you find high-upside stock ideas (Sign up for TIKR, it’s free) >>>

The Western Union Company (WU) is the world’s largest cross-border money transfer provider, serving millions of customers through its extensive retail network and growing digital platform.

The company has been implementing its Evolve 2025 strategy to transform from a declining legacy business into a stable, profitable growth entity focused on everyday financial services for the aspiring populations worldwide.

We ran Western Union through a comprehensive valuation model to assess its current value and potential upside for investors.

Using reasonable assumptions based on Western Union’s turnaround progress and strategic initiatives, the model suggests that WU stock could be worth over $11.74 per share by the end of 2027. That would imply a 40% upside from Western Union’s current share price of $8.37.

The attractive aspect of this forecast is that it assumes continued execution of its proven stabilization strategy while expanding into adjacent financial services.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What Western Union Does

Western Union operates the world’s largest money transfer network with over 500,000 agent locations across 200+ countries and territories. It facilitates cross-border money transfers through both retail locations and digital channels.

Beyond traditional remittances, Western Union has been expanding into everyday financial services, including foreign exchange, bill payments, prepaid services, and travel money – building what CEO Devin McGranahan calls a “globally diversified provider of everyday financial services.”

The business has demonstrated resilience through economic cycles, serving a loyal customer base of migrants and their families who depend on reliable and secure money transfer services.

Here’s why WU stock could deliver solid returns over the next 2.5 years through successful business transformation and market stabilization.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

In our valuation, we’ll simply use analysts’ consensus estimates and break down what analysts think the stock is worth today.

Here’s what we used for WU stock:

1. Revenue Growth: 0.3% CAGR

Western Union has faced revenue headwinds, with a 3.4% decline over the past year, as it navigated geopolitical challenges and transformation costs.

However, we project modest but positive growth of 0.3% annually through 2028 as digital growth offsets retail stabilization and new financial services gain traction.

2. Operating Margins: 19.3%

Western Union’s EBIT margins have remained strong at 18.8% over the last twelve months despite transformation investments.

We project margins will average 19.3% through 2028 as operational efficiency improvements and digital scaling drive margin expansion.

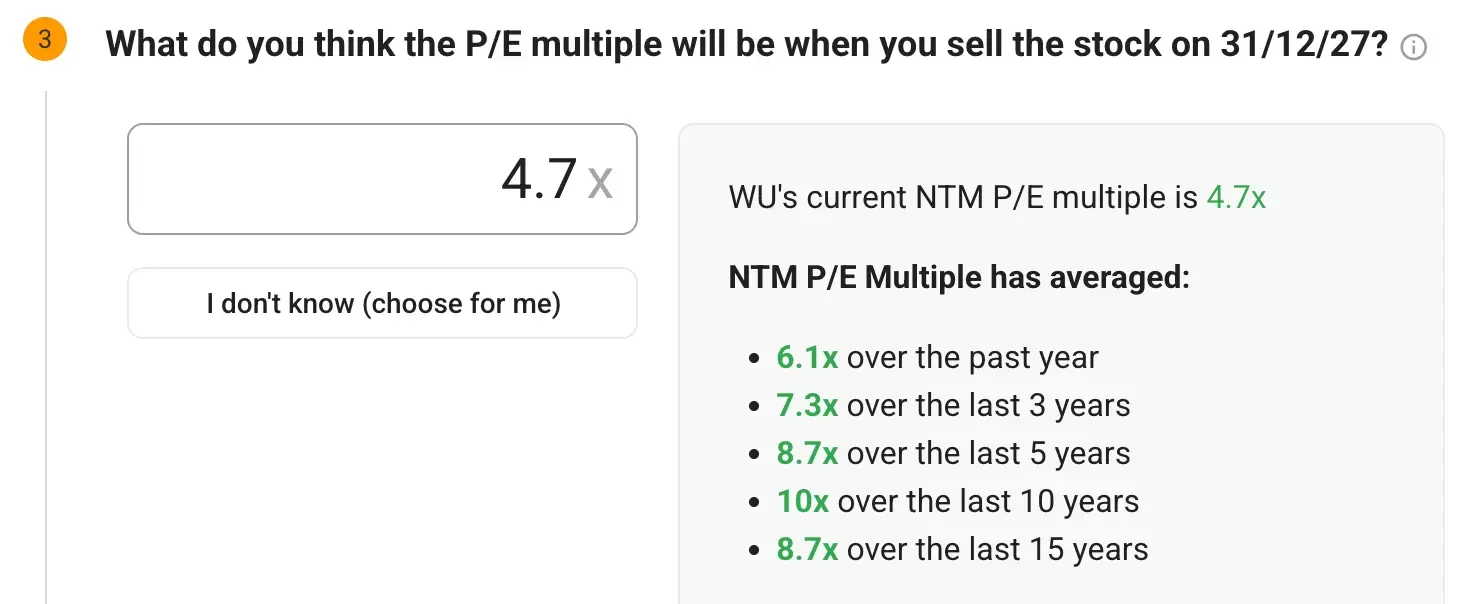

3. Exit P/E Multiple: 4.7x

Western Union currently trades at historically low multiples, reflecting uncertainty surrounding its transformation and market skepticism.

We used a 4.7x P/E multiple, which represents modest multiple expansion as the turnaround story gains credibility while remaining conservative.

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Model Says for WU Stock

With these inputs, the valuation model estimates that WU stock could reach approximately $11.74/share by the end of 2027.

Value Western Union with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

That represents a potential gain of 40% from today’s price of around $8.37. The model shows this would translate into an annualized return of approximately 14% over the next 2.5 years.

This forecast reflects Western Union’s ability to stabilize its core business while expanding into higher-growth adjacent services and improving operational efficiency.

The model forecasts the business’s future earnings-per-share based on revenue growth and margin expansion, then applies a P/E multiple to estimate the future stock price.

This helps investors understand what financial performance is required to generate strong returns and how much upside is available if those expectations are met.

What Happens If Things Go Better or Worse?

The model enables various scenarios based on the success of execution and external factors.

Here’s the range of potential outcomes:

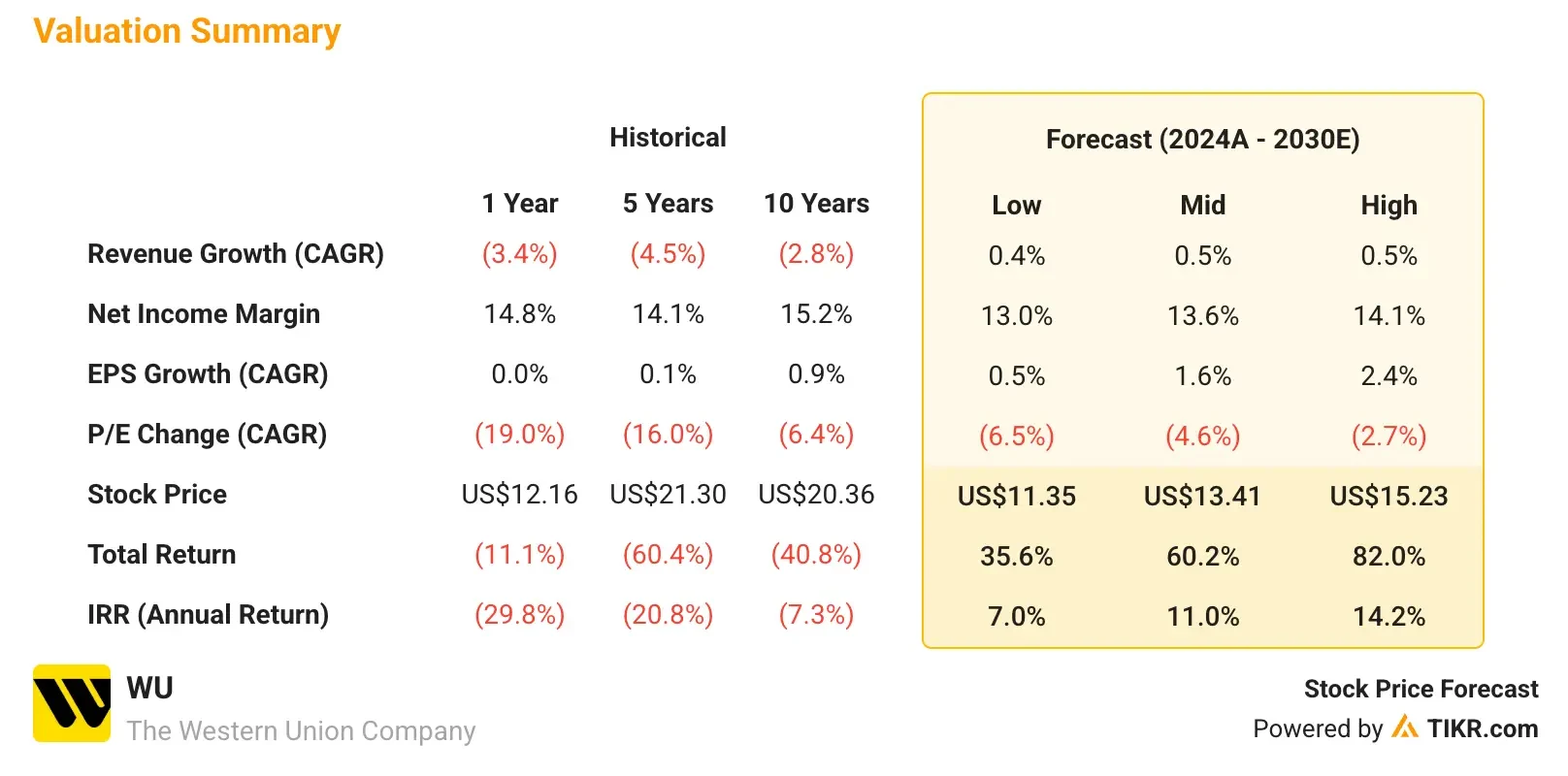

- Low Case: Continued macro headwinds with slower turnaround → 7-9% annual returns.

- Mid Case: Successful Evolve 2025 execution → 11-14% annual returns.

- High Case: Accelerated digital growth and expansion success → 14-16% annual returns.

Even the conservative scenario offers attractive returns, given the current depressed valuation, while the upside case reflects a successful transformation into a stable growth business.

Western Union’s earnings growth is likely to be driven by a combination of factors:

- Digital Transformation: Western Union has achieved eight consecutive quarters of double-digit transaction growth in digital, with branded digital revenue increasing 8% and account-to-account transactions growing by more than 35%.

- Retail Stabilization: The European business demonstrates turnaround potential, with 10% transaction growth, the first double-digit growth in the region in over a decade.

- Geographic Diversification: Rest of World markets (50% of revenue) showing double-digit transaction growth, offsetting Americas headwinds.

- Service Expansion: Consumer Services is growing at a double-digit rate, with Travel Money becoming a nearly $100 million business in Europe alone.

- Operational Efficiency: $140 million in cost savings achieved to date, exceeding the $150 million target two years ahead of schedule.

How Wall Street Sees WU Stock

Wall Street analysts remain bullish on Western Union stock. The current analyst target prices suggest a 31% upside, with the average target around $11.

The company’s 9% dividend yield offers an attractive income stream while investors await the turnaround to materialize.

See analysts’ growth forecasts and price target for Western Union (It’s free!) >>>

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact Western Union’s growth trajectory:

- Geopolitical Headwinds: Immigration policy changes and proposed remittance taxes (3.5% in current legislation) could impact demand and pricing power.

- Competitive Pressure: Digital-native competitors and fintech solutions continue to pressure traditional money transfer pricing and market share.

- Macro Sensitivity: Economic downturns in key corridors can quickly impact remittance volumes and customer behavior.

- Execution Risk: The Evolve 2025 strategy relies on the continued successful execution of multiple initiatives and markets.

- Regulatory Environment: Increasing compliance costs and regulatory scrutiny in key markets could pressure margins and growth.

TIKR Takeaway

Western Union has built a resilient global platform that’s showing early signs of successful transformation under the Evolve 2025 strategy.

If it continues stabilizing the retail business while scaling digital services and expanding into adjacent financial products, we believe WU stock offers attractive risk-adjusted returns for value-oriented investors.

The 40% upside potential over the next 2.5 years, combined with a 10% dividend yield, makes Western Union stock an attractive option for investors seeking both income and capital appreciation.

Is WU stock a buy over the next 24 months? Use TIKR’s Valuation Model alongside analysts’ growth forecasts and price targets to see if it is undervalued today.

Value any stock with TIKR’s Valuation Models (It’s free!) >>>

Want to Invest Like Warren Buffett, Joel Greenblatt, or Peter Lynch?

TIKR just published a special report breaking down 5 powerful stock screeners inspired by the exact strategies used by the world’s greatest investors.

In this report, you’ll discover:

- A Buffett-style screener for finding wide-moat compounders at fair prices

- Joel Greenblatt’s formula for high-return, low-risk stocks

- A Peter Lynch-inspired tool to surface fast-growing small caps before Wall Street catches on

Each screener is fully customizable on TIKR, so you can apply legendary investing strategies instantly. Whether you’re looking for long-term compounders or overlooked value plays, these screeners will save you hours and sharpen your edge.

This is your shortcut to proven investing frameworks, backed by real performance data.

Click here to sign up for TIKR and get this full report now, completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!