Key Takeaways:

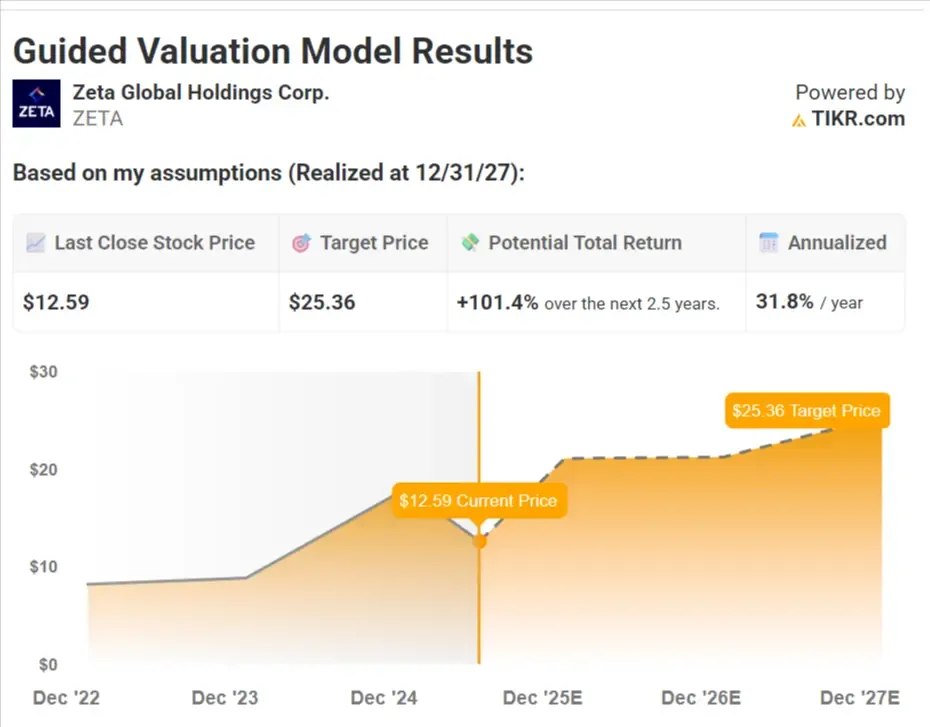

- ZETA Global stock could conservatively be worth over $25/share by the end of 2027.

- That’s a potential 101% upside from today’s price of ~$12.50/share.

- ZETA is projected to grow earnings significantly as revenue compounds at over 20% annually and margins expand.

- Unlock our Free Report: 5 stock screeners inspired by top investors like Warren Buffett to help you find high-upside stock ideas (Sign up for TIKR, it’s free) >>>

Zeta Global (ZETA) is a fast-growing software company that uses AI to help businesses acquire and retain customers more effectively.

It combines first-party data, advanced identity resolution, and real-time personalization into a single marketing cloud platform.

We ran Zeta through TIKR’s new Valuation Model to see what the stock could be worth today, and what kind of upside investors could see.

Using reasonable assumptions based on analyst estimates, the model suggests Zeta could be worth over $25/share by the end of 2027. That would imply over 100% upside from Zeta’s current $12.59 share price.

The best part is that this forecast assumes Zeta continues growing and maintains the same valuation multiple that it trades at today.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What Zeta Does

Zeta helps brands unify customer data, predict behavior using machine learning, and personalize outreach across email, web, app, and more.

The platform acts as an operating system for marketing teams, improving return on ad spend and customer lifetime value.

The company is growing fast. Revenue has compounded at nearly 30% annually over the past three years, and its margins are improving as it scales.

Here’s why the stock could have 100% upside today over the next 2.5 years, which would be over 30% annual returns.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

In our valuation, we’ll simply use analysts’ consensus estimates and break down what analysts think the stock is worth today.

Here’s what we used for Zeta:

1. Revenue Growth: 20.2% CAGR

Zeta has grown revenue by 38% over the past year and nearly 30% per year over the last three years. Analysts estimate that Zeta will average 20.2% annual revenue growth through 2028.

2. Operating Margins: 16.2%

Zeta’s EBIT margins have steadily improved from 7% (five-year average) to 13.6% over the last twelve months. As the business continues to scale, we assume margins will average 16.2% over the next four years.

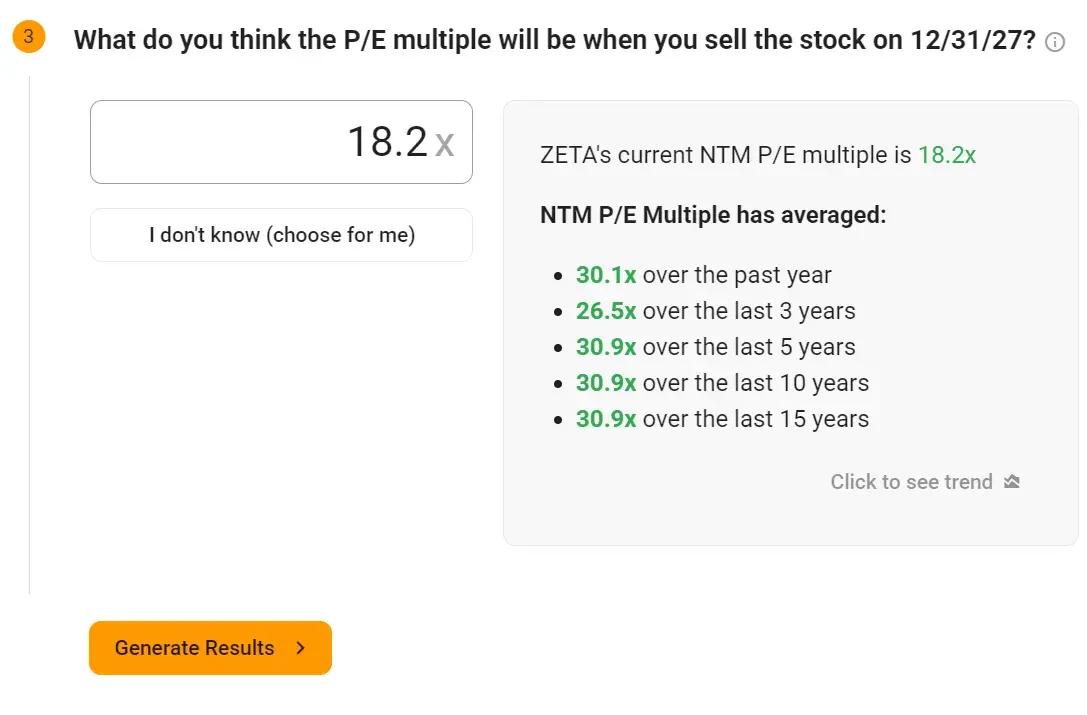

3. Exit P/E Multiple: 18x

Zeta currently trades at a forward P/E of 18.2x. We used the model’s default assumption of an 18x exit multiple, which aligns with current levels and doesn’t rely on multiple expansion.

It’s worth noting that Zeta could trade at a P/E multiple closer to 30x, as it has in the past. This would unlock an additional 50% upside for the stock, on top of the 100% upside that our Valuation Model and analysts alike see.

But, we’ll be conservative and use an 18x P/E multiple:

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Model Says

With the inputs we shared earlier, TIKR’s Valuation Model estimates that Zeta’s stock could reach ~$25/share by the end of 2027.

That’s a potential gain of more than 100% from today’s price of ~$12.50. The model also shows this would translate into an annualized return of around 31.8% over the next 2.5 years.

The model forecasts the business’s future earnings-per-share based on revenue growth and margin expansion, then applies a P/E multiple to estimate the future stock price.

This helps investors understand what financial performance is required to generate strong returns and how much upside is available if those expectations are met.

What Happens If Things Go Better or Worse?

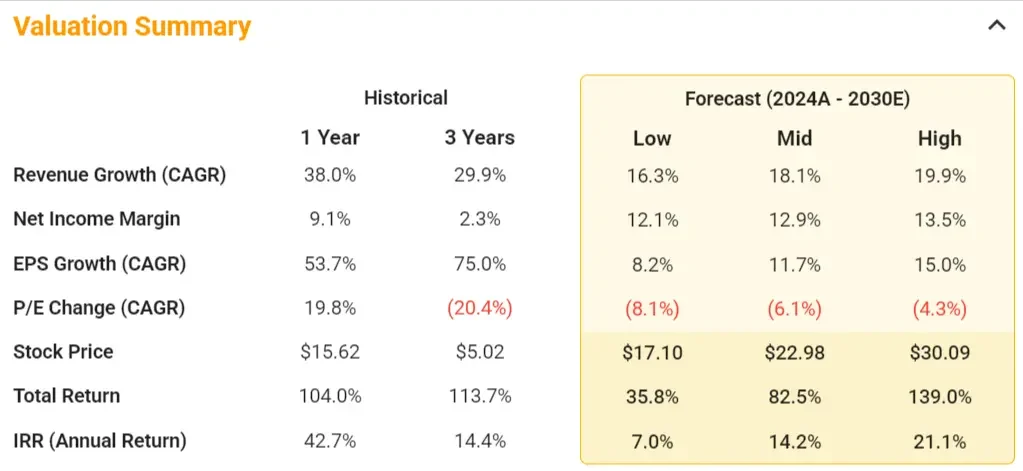

TIKR lets you build conservative and optimistic scenarios so you can see how a stock might perform depending on how the business executes.

This shows that over the next 5 years, based on analyst estimates, the stock could perform in a range between 7-21% annualized returns.

Here’s a quick look:

- Low Case: $17.10/share by 2030 → 7.0% annual return

- Mid Case: $22.98/share by 2030 → 14.2% annual return

- High Case: $30.09/share by 2030 → 21.1% annual return

Even the low case offers a return that’s just about in line with the broader market, assuming Zeta continues to grow but at a more modest pace. The high case reflects strong execution and healthy margin gains.

Zeta’s earnings growth is likely to be driven by a combination of accelerating revenue and expanding margins:

- Expanding Customer Base: Zeta is winning larger enterprise clients across key industries like retail, financial services, and healthcare, helping to grow recurring revenue.

- Higher ARPU (Average Revenue per User): As customers adopt more of Zeta’s marketing modules, the company increases its wallet share and drives higher revenue per client.

- AI-Powered Platform Leverage: Zeta’s platform is largely automated and AI-driven, which allows it to scale without needing to add headcount at the same pace as revenue, improving operating margins.

- Cloud Infrastructure Migration: Moving to Snowflake’s cloud-native platform is expected to reduce infrastructure costs and boost gross margin over time.

- Improved Sales Efficiency: Sales productivity has improved significantly, as the go-to-market strategy becomes more focused and conversion rates increase.

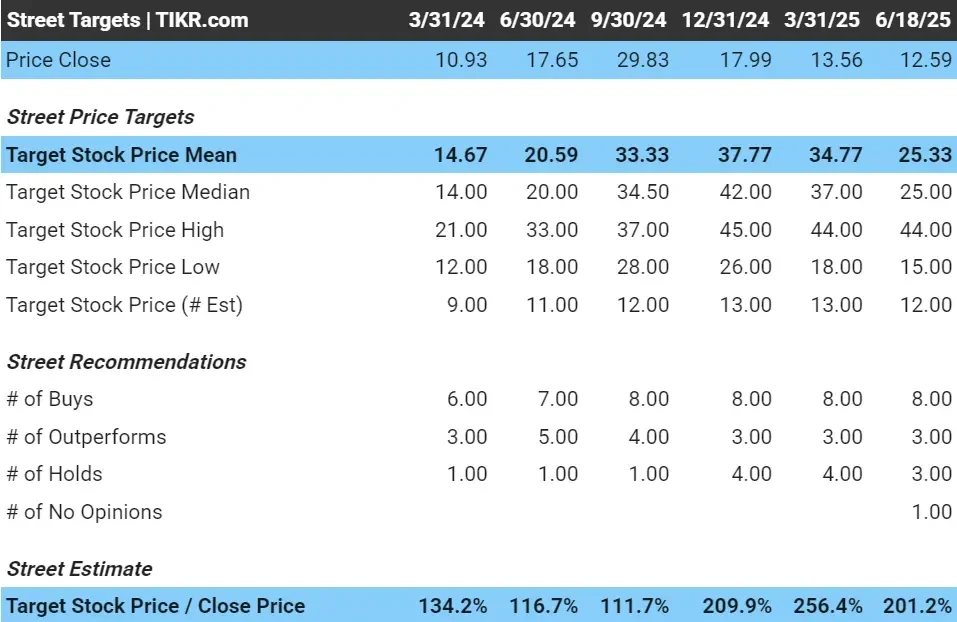

How the Street Sees It

In the near term, Wall Street also sees upside. Analysts have an average price target of ~$25/share, which means they see about 100% upside for the stock:

See analysts’ growth forecasts and price target for Zeta Global (It’s free!) >>>

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact Zeta’s growth trajectory:

- Ad Tech Competition: Zeta operates in a crowded industry alongside giants like Google, Meta, and The Trade Desk. Larger competitors may outspend Zeta or limit its access to key ad inventory and data partnerships.

- GAAP Profitability Still Limited: While Zeta generates consistent free cash flow, its GAAP net income remains negative due to ongoing investments in growth and non-cash charges. This could limit valuation multiples until earnings turn positive.

- Customer Concentration: A meaningful portion of Zeta’s revenue comes from its top customers. Losing a major account could cause revenue volatility and slow growth momentum.

- Execution Risk: Zeta’s long-term success depends on its ability to onboard new clients, retain enterprise customers, and keep pace with rapid shifts in AI and privacy regulations. Missteps in these areas could impact adoption and returns.

TIKR Takeaway

Zeta Global has built a powerful platform that’s growing quickly and becoming more profitable over time.

If the company keeps executing, we believe the stock could be worth significantly more than where it trades today. TIKR’s new Valuation Model makes it easy what a stock could be worth and what kind of upside could be on the table.

Is Zeta stock a buy over the next 24 months? Use TIKR’s Valuation Model alongside analysts’ growth forecasts and price targets to see if it is undervalued today.

Value any stock with TIKR’s Valuation Models (It’s free!) >>>

Want to Invest Like Warren Buffett, Joel Greenblatt, or Peter Lynch?

TIKR just published a special report breaking down 5 powerful stock screeners inspired by the exact strategies used by the world’s greatest investors.

In this report, you’ll discover:

- A Buffett-style screener for finding wide-moat compounders at fair prices

- Joel Greenblatt’s formula for high-return, low-risk stocks

- A Peter Lynch-inspired tool to surface fast-growing small caps before Wall Street catches on

Each screener is fully customizable on TIKR, so you can apply legendary investing strategies instantly. Whether you’re looking for long-term compounders or overlooked value plays, these screeners will save you hours and sharpen your edge.

This is your shortcut to proven investing frameworks, backed by real performance data.

Click here to sign up for TIKR and get this full report now, completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!