Key Takeaways:

- Zeta stock could reasonably reach over $28 per share by the end of 2027.

- That implies a potential 83% upside from today’s price of about $15.50.

- The company is gaining traction in AI-driven marketing and identity resolution, while trading at a discount to peers despite faster growth.

- Unlock our Free Report: 5 stock screeners inspired by top investors like Warren Buffett to help you find high-upside stock ideas (Sign up for TIKR, it’s free) >>>

Zeta Global (ZETA) is a software company that helps brands turn customer data into personalized marketing across email, web, and mobile.

Its platform uses artificial intelligence to determine the right audience, message, and timing so that its clients can boost engagement and marketing ROI. As third-party cookies disappear, Zeta’s focus on first-party data and identity resolution is becoming even more valuable.

Despite being unprofitable on a GAAP basis today, Zeta is growing faster than many of its larger peers and is showing improving operating leverage. With long-term contracts and sticky recurring revenue, the business has laid a foundation for scalable growth.

We ran a comprehensive valuation analysis on Zeta stock using TIKR’s Valuation Model to see how much upside it could offer over the next 2.5 years.

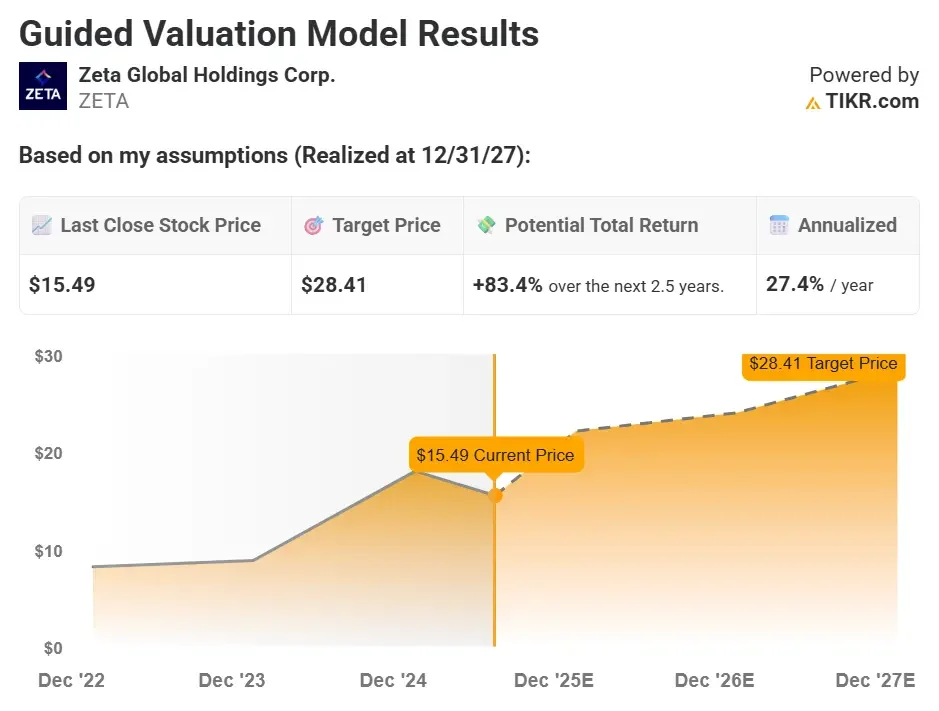

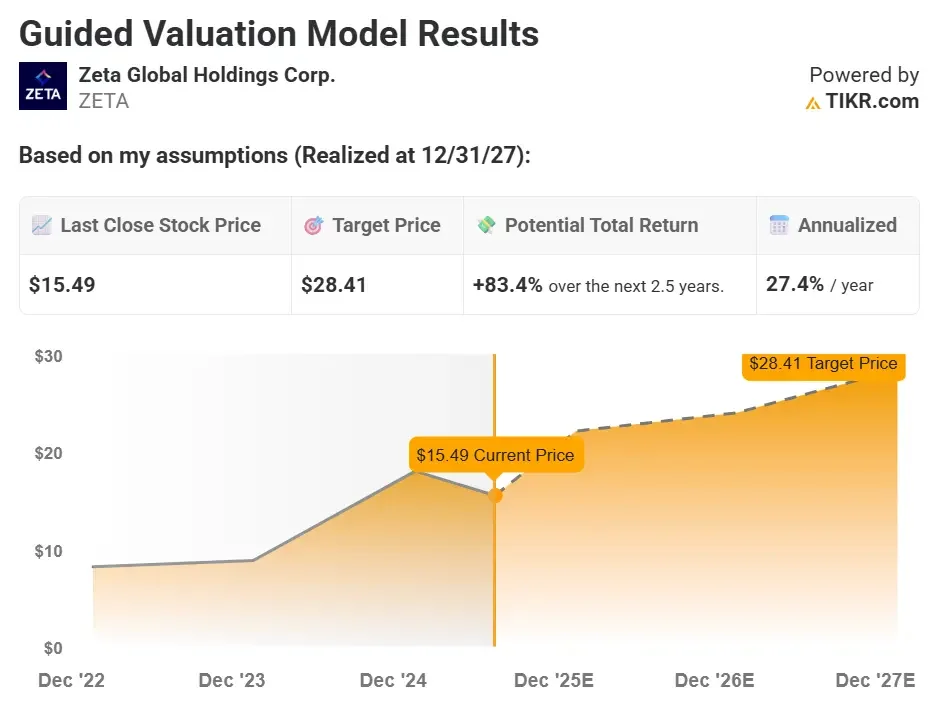

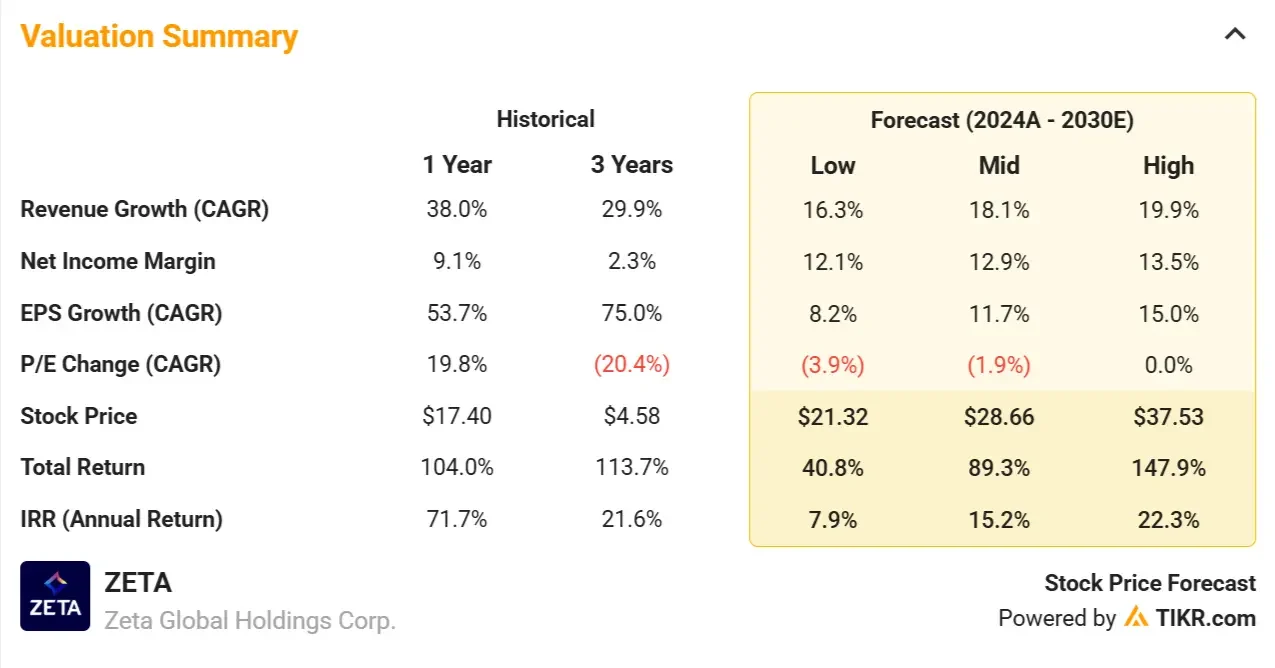

Using realistic assumptions for revenue growth, operating margins, and earnings multiple expansion, our model suggests that Zeta stock could reach $28.41 per share by the end of 2027, which would be a potential total return of 83.4% and an annualized return of 27.4%.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What Zeta Global Does

Zeta Global is a marketing technology company that helps businesses personalize their outreach across email, websites, and mobile apps using artificial intelligence.

Its platform focuses on identity resolution and first-party data, giving brands the ability to target the right customers with the right message at the right time, even as third-party cookies become obsolete. This shift in the ad ecosystem is a major tailwind for Zeta’s business model.

Zeta’s clients include large enterprises across industries, and the company generates most of its revenue through long-term contracts and recurring subscriptions. Its software-driven offering helps marketers improve engagement, conversion rates, and return on ad spend (ROAS).

What makes Zeta compelling is its ability to combine massive data sets, predictive AI, and omnichannel delivery into a single unified platform. As the digital advertising market shifts toward privacy-first solutions, Zeta is positioned as a differentiated player with strong competitive advantages.

Here’s why Zeta stock could deliver strong returns over the next 2.5 years as it scales its platform and expands its margins.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

In our valuation, we’ll simply use analysts’ consensus estimates and break down what analysts think the stock is worth today.

Here’s what we used for Zeta stock:

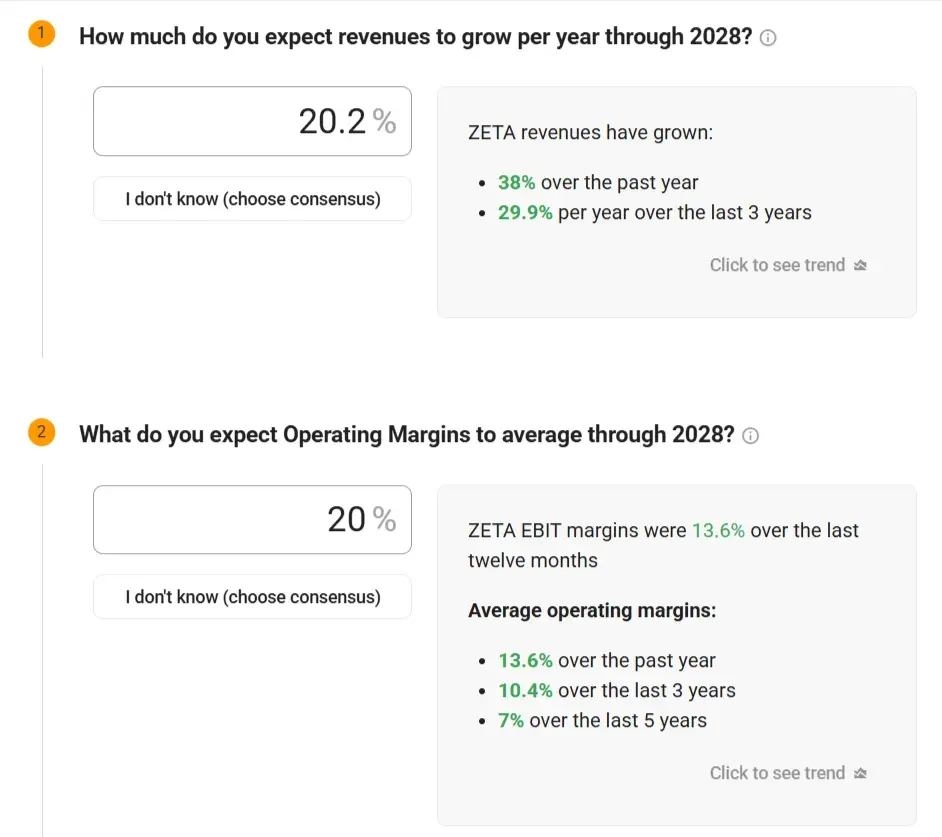

1. Revenue Growth: 20.2% CAGR

Zeta has grown revenue at an average rate of 30% per year over the past three years, including 38% growth in the last year alone.

As more marketers shift spend toward first-party data strategies, we expect Zeta to maintain strong double-digit growth by increasing wallet share with current clients and expanding into larger enterprise accounts.

2. Operating Margins: 20%

Zeta’s operating margins have averaged 13.6% over the past year, and the company continues to improve efficiency as it scales.

We modeled continued expansion toward 20% operating margins, driven by increasing software contribution, automation, and improved customer economics.

Zeta’s GAAP operating margins appear negative due to significant non-cash expenses, most notably stock-based compensation (SBC), which totaled roughly $200 million over the past year.

When adjusting for SBC and other non-core items, the company’s underlying operating margins turn positive, which shows how the business is improving efficiency as it scales.

Investors should understand that while adjusted operating margins provide a clearer view of the company’s core performance, SBC is still a real cost to shareholders. It can lead to dilution if not offset by strong earnings growth or share repurchases.

In Zeta’s case, continued progress toward sustainable profitability and moderation in SBC levels will be key for long-term shareholder returns.

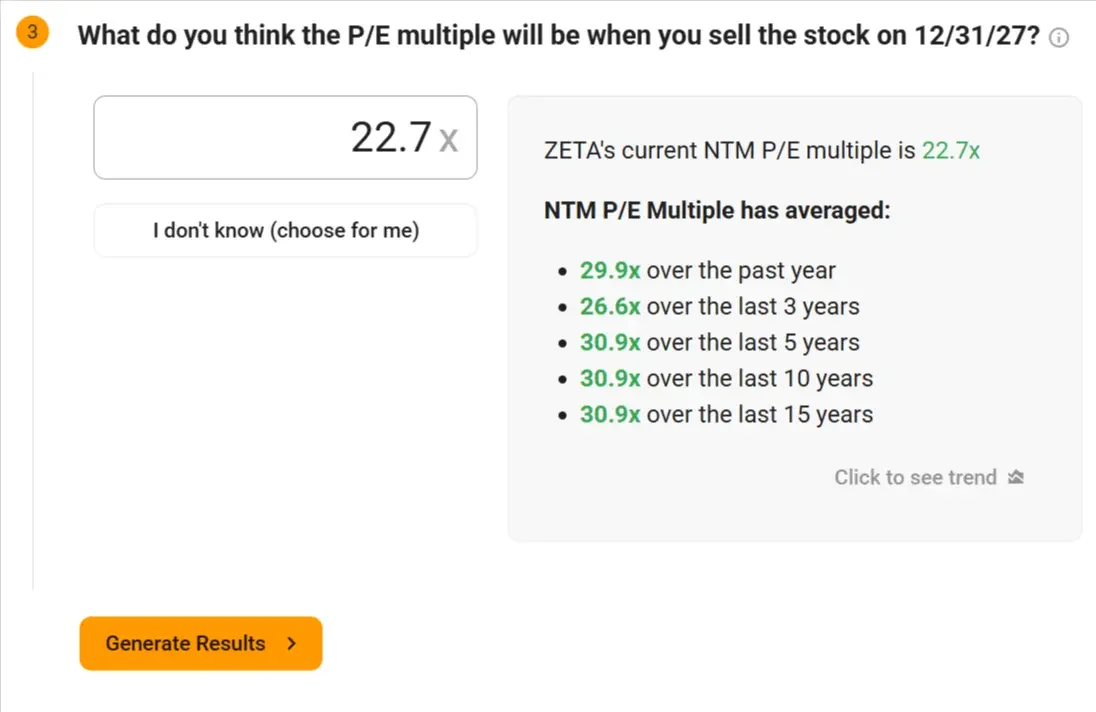

3. Exit P/E Multiple: 22.7x

Zeta currently trades at a forward P/E of 22.7x, which is well below the 30x average it has commanded over the past 5 years.

Given its improving profitability and strong growth profile, we believe this multiple is reasonable and even conservative if investor sentiment improves.

With 20% annual revenue growth and margin expansion, it’s possible the stock could trade at a P/E ratio closer to 30x or 40x. This could drive significant additional upside for the stock.

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Model Says for Zeta Stock

Using the assumptions outlined above, our valuation model estimates that Zeta stock could reach over $28 per share by the end of 2027, representing a potential 83.4% upside from its current price of around $15.50.

Value Zeta with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

This translates to an annualized return of roughly 27.4% over the next 2.5 years.

The model assumes Zeta continues scaling its platform, improving operating margins, and expanding within enterprise accounts as more marketers shift toward privacy-compliant, first-party data solutions.

The model forecasts the business’s future earnings-per-share based on revenue growth and margin expansion, then applies a P/E multiple to estimate the future stock price.

What Happens If Things Go Better or Worse?

TIKR’s model allows investors to test a range of scenarios depending on how well Zeta executes and how quickly the market rewards it with multiple expansion.

Here’s the breakdown of possible returns Zeta could see over the next 5 years (these are just estimates, and nobody knows what the future holds):

- Low Case: Slower adoption and margin pressure → 7.9% annual returns

- Mid Case: Continued growth with improving operating leverage → 15.2% annual returns

- High Case: Rapid market share gains and faster margin expansion → 22.3% annual returns

Even in the conservative scenario, the stock delivers positive returns, while the high-case scenario suggests Zeta could handily outperform the market’s long-term average.

Zeta’s earnings growth is likely to be driven by a combination of factors:

- AI-Driven Personalization: Zeta’s platform helps brands create personalized marketing across email, web, and mobile, improving engagement and ROI.

- First-Party Data Tailwind: As cookies phase out, marketers need better tools to identify and reach customers—Zeta’s identity resolution engine solves that problem.

- Enterprise Expansion: The company continues landing larger clients with higher contract values, expanding its presence in Fortune 1000 accounts.

- Operating Leverage: As revenue grows, margins are expanding—supported by automation, higher software contribution, and recurring revenue.

- Valuation Gap: Zeta trades at a discount to peers like HubSpot and Salesforce despite growing faster and improving profitability.

How the Street Sees Zeta Stock

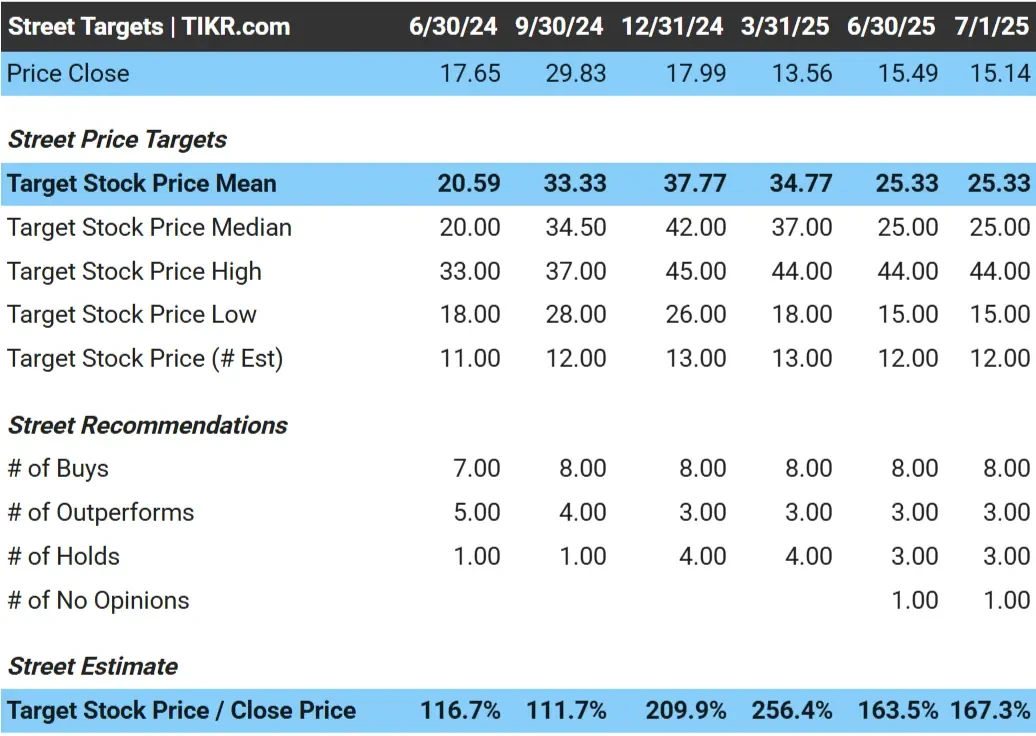

Wall Street analysts remain optimistic about Zeta, with an average price target of just over $25 per share, implying the stock has nearly 70% upside today.

Analysts’ bullish valuation likely reflects Zeta’s potential for stronger margin expansion and continued momentum in enterprise adoption.

See analysts’ growth forecasts and price target for Zeta (It’s free!) >>>

Risks to Consider

While the outlook is promising, investors should be aware of key risks that could affect Zeta’s growth trajectory:

- Execution Risk: Zeta must continue improving margins and converting large enterprise deals into long-term, high-quality revenue.

- Competition: The martech space is crowded, with competitors like Adobe, Salesforce, and HubSpot all investing heavily in AI capabilities.

- SBC-Driven Dilution: High levels of stock-based compensation could dilute shareholder value if not offset by strong earnings growth.

- Profitability Timing: Although free cash flow is positive, the company remains unprofitable on a GAAP basis, which may weigh on sentiment in a rising-rate environment.

- Client Budget Pressure: Marketing budgets can be cyclical—economic softness could delay adoption or contract expansion.

TIKR Takeaway

Zeta offers a compelling opportunity for investors looking to gain exposure to next-generation marketing technology.

Its AI-driven platform, focus on first-party data, and recurring revenue model position the company well to benefit from long-term shifts in digital advertising.

With 83% upside potential over the next 2.5 years, strong revenue growth, and improving operating leverage, Zeta could be one of the more underappreciated software stocks in the market.

The stock remains best suited for investors who are comfortable with earlier-stage growth stories and are looking for high-upside ideas with favorable risk/reward characteristics.

Is Zeta stock a buy over the next 24 months? Use TIKR’s Valuation Model and analyst forecasts to see whether the stock is undervalued today.

Value any stock with TIKR’s Valuation Models (It’s free!) >>>

Want to Invest Like Warren Buffett, Joel Greenblatt, or Peter Lynch?

TIKR just published a special report breaking down 5 powerful stock screeners inspired by the exact strategies used by the world’s greatest investors.

In this report, you’ll discover:

- A Buffett-style screener for finding wide-moat compounders at fair prices

- Joel Greenblatt’s formula for high-return, low-risk stocks

- A Peter Lynch-inspired tool to surface fast-growing small caps before Wall Street catches on

Each screener is fully customizable on TIKR, so you can apply legendary investing strategies instantly. Whether you’re looking for long-term compounders or overlooked value plays, these screeners will save you hours and sharpen your edge.

This is your shortcut to proven investing frameworks, backed by real performance data.

Click here to sign up for TIKR and get this full report now, completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!