Key Takeaways:

- ELV offers a 1.8% dividend yield today, which is the highest it’s been in the past five years.

- Earnings are expected to resume double-digit annual growth in 2026 after a tough 2024.

- Analysts see 35% upside for the stock based on analysts’ consensus price target.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Elevance Health, formerly known as Anthem, Inc., is a major U.S. health insurance company that operates Blue Cross and Blue Shield plans in 14 US states through its affiliated brands like Anthem Blue Cross and Blue Shield.

As one of the largest health insurance companies in the U.S., ELV is a major force in managed care.

With rising dividends, consistent earnings growth, and a strong position in both government and commercial health plans, Elevance could be a long-term winner for dividend-focused investors.

Why Is Elevance Stock Down 10% in the Past Month?

Here are some of the key reasons that Elevance Health stock is down:

- Rising Medical Costs: Elevance reported higher-than-expected medical costs last quarter, especially in their Medicaid business. That pushed their benefit expense ratio up and weighed on profits.

- Medicaid Redeterminations: Now that pandemic-era Medicaid policies have ended, some members are losing coverage. But the members who remain tend to have higher health needs, leading to increased medical costs and added pressure on margins.

- Shaky Investor Confidence: The company cut its full-year earnings guidance last quarter, signaling weaker-than-expected performance ahead. That added to ongoing concerns about the long-term profitability of its Medicaid and Medicare Advantage businesses.

However, analysts think the stock is undervalued today.

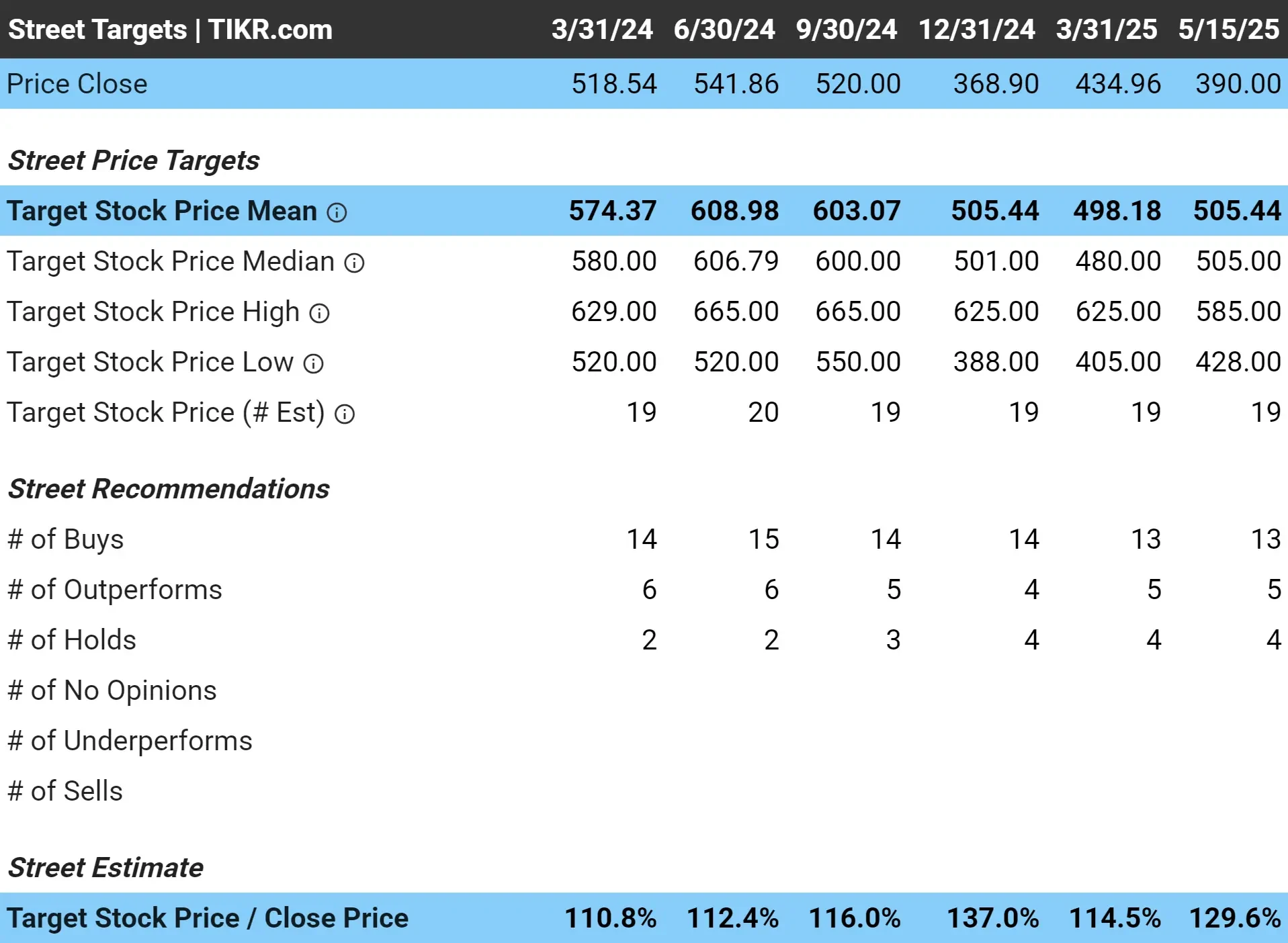

Analysts See Nearly 30% Upside for Elevance Health Stock Today

Elevance Health trades today at around $390/share. Analysts currently have an 18-month average price target of $505/share, which implies that the stock could have a potential upside of about 30%.

That’s a sizeable amount of upside, especially for a stable, cash-generating business like Elevance.

The stock’s forward P/E remains at around 11x, which is well below peers like UnitedHealth (UNH) or Cigna (CI).

With earnings expected to grow steadily over the next few years, ELV could be one of the more undervalued names in the managed care space today.

See why Elevance Health looks undervalued today with TIKR (It’s free) >>>

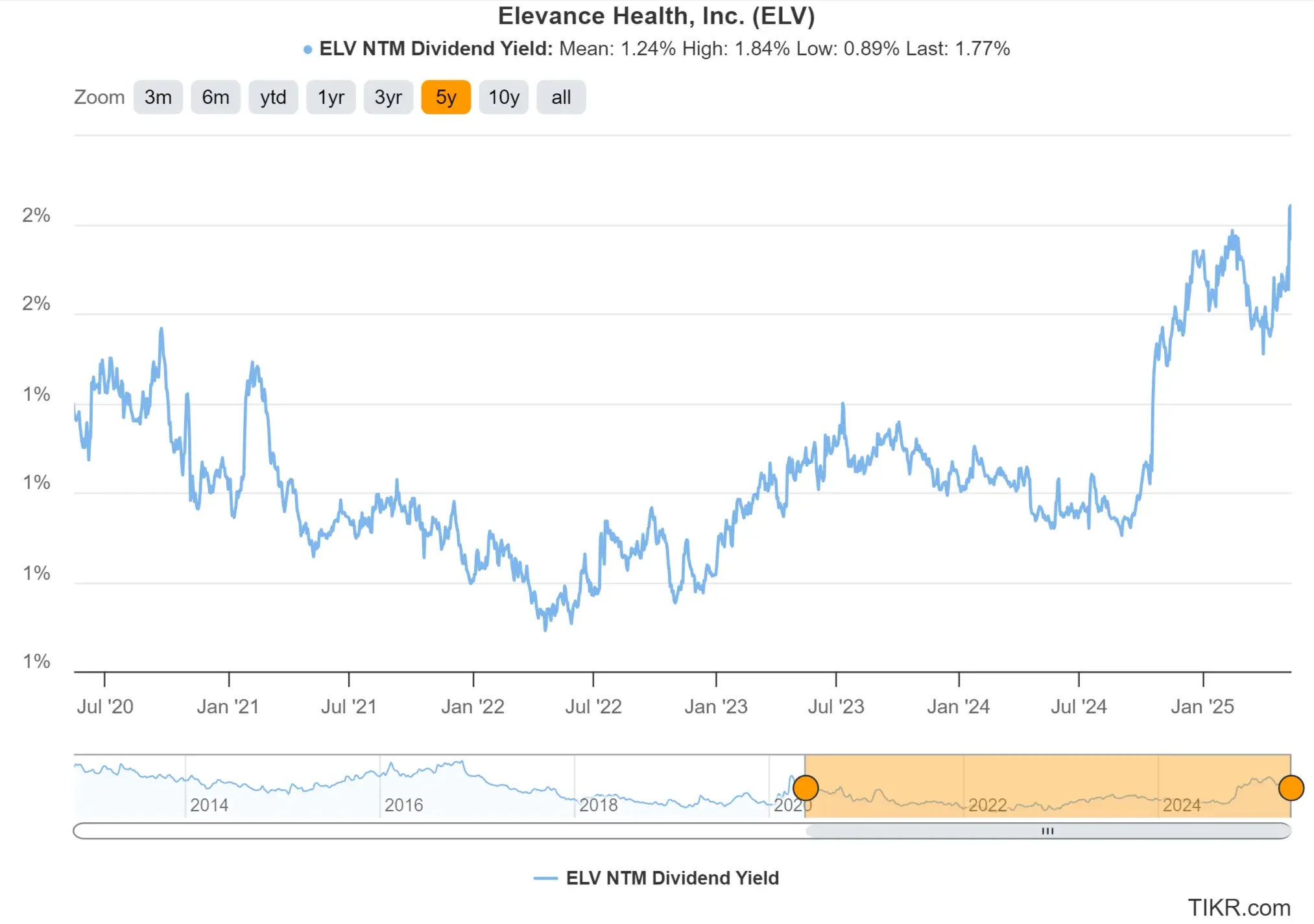

1: Dividend Yield

Elevance Health currently offers a forward dividend yield of 1.8%, which is the highest dividend yield the stock has offered in the past five years. The 5-year average yield is around 1.2%, so today’s level makes the stock look especially appealing.

The higher dividend yield is primarily the result of the stock’s recent price decline. Elevance Health also raised its dividend again in Q1 2025, marking its 12th consecutive year of dividend increases.

For long-term investors, a rising yield and strong free cash flow make Elevance a solid option in the healthcare space.

Find dividend growth stocks even better than Elevance Health with TIKR. (It’s free) >>>

2: Dividend Safety

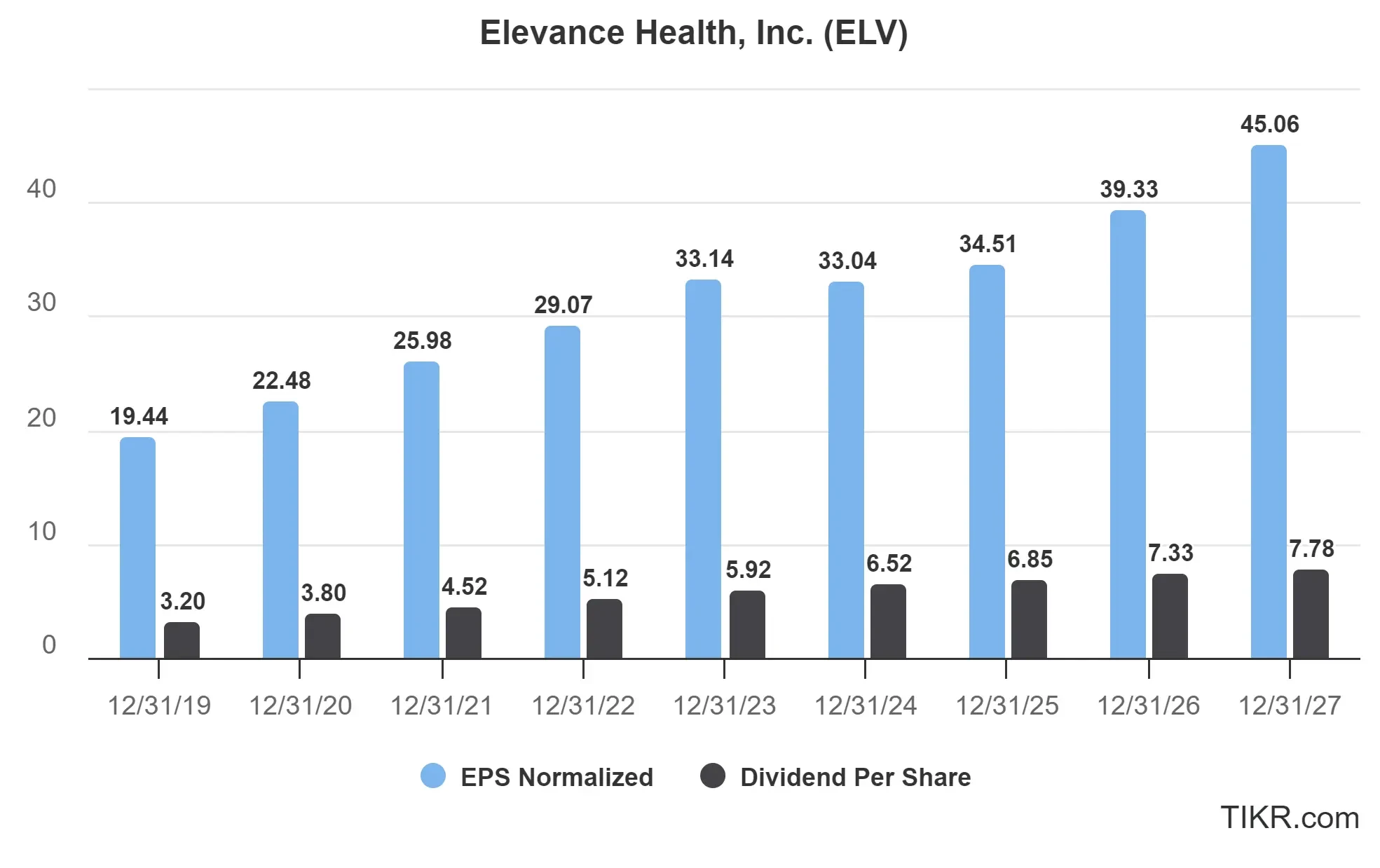

Elevance’s dividend is well-supported by earnings. In 2024, the company paid out $6.52 per share in dividends while generating $33.04 in normalized EPS, resulting in a dividend payout ratio of just under 20%. This is well below the 70% threshold we typically look for in a sustainable dividend.

Analysts expect earnings to grow to $45.06 per share by 2027, while dividends are projected to rise to $7.78. That means analysts expect the future payout ratio to be about 17%, which is very conservative for a dividend-paying stock.

This low payout ratio gives Elevance plenty of room to grow its dividend while reinvesting in the business and absorbing any volatility in medical costs.

See Elevance Health’s full growth forecast and analyst estimates. (It’s free) >>>

3: Dividend Growth Potential

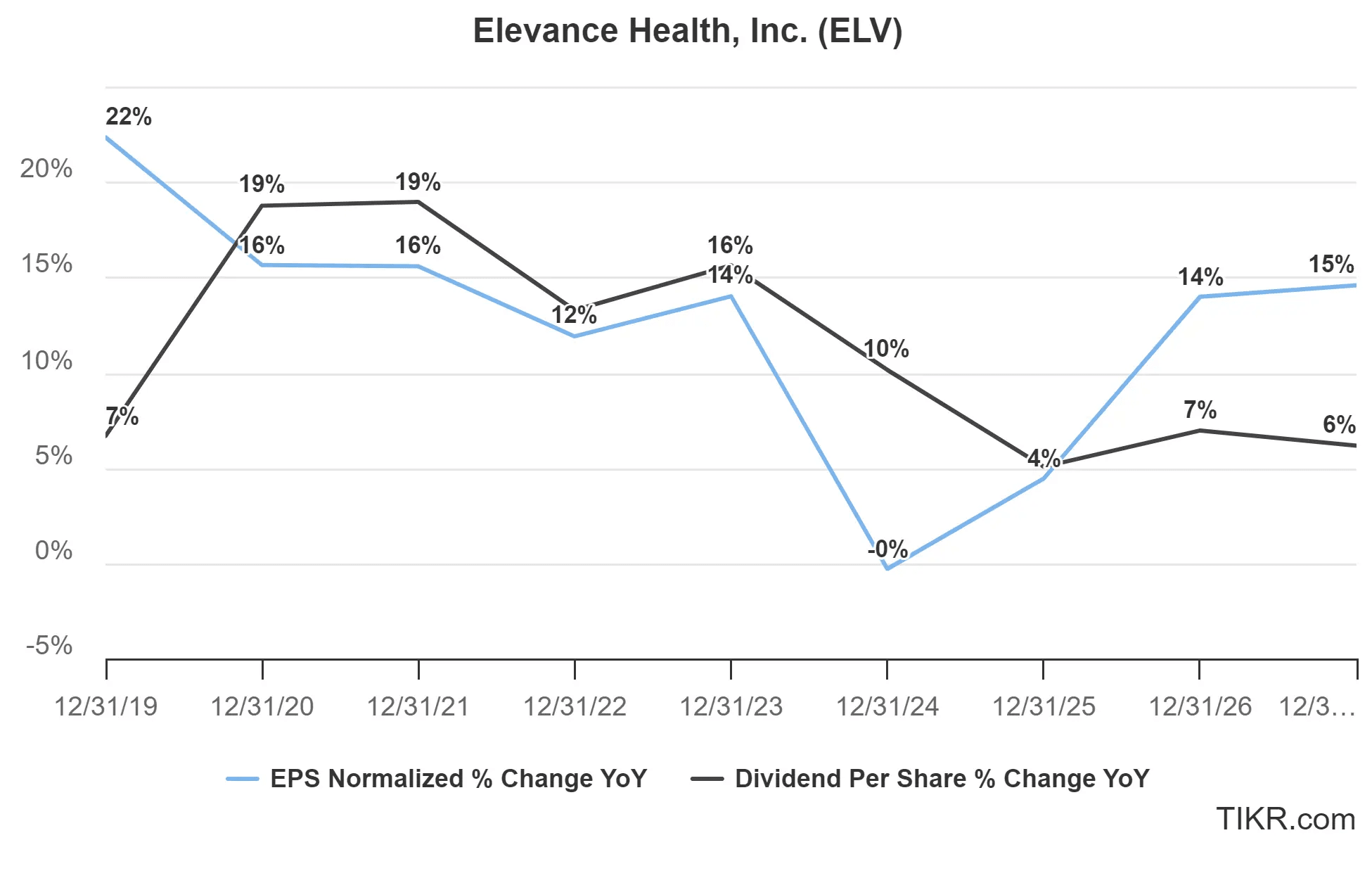

Over the past five years, Elevance has grown its dividend at a 15% compound annual growth rate while earnings grew at an 11% CAGR.

That’s pretty strong earnings and dividend growth, and analysts expect this kind of growth to continue.

Earnings growth slowed down in 2024, but analysts expect the company to resume double-digit earnings growth in 2026. The company is expected to grow dividends in the mid-single-digits over the next 3 years.

With consistent profitability and a low payout ratio, Elevance is well-positioned to keep raising its dividend in the years ahead.

TIKR Takeaway

Elevance Health could be a good stock for dividend growth investors with a payout ratio under 20%, consistent free cash flow, and a strong balance sheet. At just 11 times forward earnings, analysts believe the market is undervaluing this healthcare leader.

For long-term investors looking for quality, stability, and dividend growth, Elevance is worth a closer look.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!