Key Stats for Ultra Clean Holdings Stock

- Current Price: $104.83

- Street Target (Mean): ~$107

- TIKR Model Target (Mid): ~$125

- Potential Total Return (Mid): ~19%

- Annualized IRR (Mid): ~4% / year

- Earnings Reaction: +7.97% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Ultra Clean Holdings (UCTT) hit a 52-week high of $104.93 on June 11, closing at $104.83 after surging 15.32% on the day. The stock is up more than 230% year to date, making it one of the strongest performers in the semiconductor equipment space. The catalyst: Oppenheimer raised its price target from $100 to $115 and reiterated an Outperform rating following a June 8 broker-hosted meeting with management, citing a semiconductor equipment cycle it now believes is stronger and longer than previously modeled.

That is the bull case in brief. But the TIKR model’s mid-case target of ~$125 implies only about 19% total return through the end of 2030, or roughly 4% annualized from current prices. The Street’s mean target is ~$107, barely above where the stock closed. Understanding what bulls and bears are actually arguing and what the data supports is the only way to make a clean-eyed decision here.

Ultra Clean’s investor relations materials lay out the company’s role clearly: it makes the critical subsystems inside chip-making machines, including gas delivery panels, chemical delivery modules, and process modules, and provides ultra-high purity cleaning services that keep those tools running. It does not build the machines itself. That means UCTT captures revenue from both new tool installations tied to WFE spending and from rising wafer starts through its services business.

What the Upgrade Actually Signals

WFE, or wafer fabrication equipment, is the capital that chipmakers spend on machines used to manufacture semiconductors, and it is the master variable for Ultra Clean’s revenue. On the Q1 2026 earnings call, CEO James Xiao said customers are quoting $140 billion to $145 billion in WFE for 2026, implying 18% to 20% growth over 2025, and are already signaling growth of 15% or more for 2027. When the forward demand signal stretches two to three years rather than one, the valuation math changes significantly for a company with Ultra Clean’s operating leverage structure, and that extension is precisely what Oppenheimer is now pricing in.

Not all WFE spending is growing at the same rate. Xiao noted that leading-edge foundry logic, high-bandwidth memory (HBM), and advanced packaging are seeing the sharpest capital intensity increases, and these segments are “etch and removal intensive,” meaning they disproportionately drive demand for Ultra Clean’s subsystems. Deposition and etch equipment represented roughly mid-30% of total WFE in the first half of 2026. Customers are projecting that share to rise to the high 30s in the second half, a direct tailwind for UCTT’s product mix.

As for China risk: domestic Chinese customers represent less than 5% of UCTT’s total revenue, confirmed by CEO Xiao on the Q1 call. China’s share of worldwide WFE has normalized from 35%–40% during the 2024–2025 inventory-build period back to the low 20s, which Xiao described as a return to normal, not a structural headwind.

Q1 Beat, Q2 Guidance Points Higher

Ultra Clean reported Q1 2026 revenue of $533.7 million, ahead of the guided midpoint. Product revenue was $465.7 million, and services revenue was $68 million, with services gross margin at 30%. Adjusted EPS of $0.31 beat the $0.26 consensus by 18.1%, and the stock gained 7.97% on the April 28 reporting date.

Q2 guidance calls for revenue of $565–$605 million and EPS of $0.44–$0.60, continuing the sequential growth trajectory. CEO Xiao put the capacity picture plainly: “Our global footprint supports around $3 billion in revenue today and can scale up to $4 billion with modest incremental capital investment.” With the current annualized run rate around $2.1–$2.2 billion, there is meaningful headroom before the company needs major new capital commitments to absorb growth. CFO Sheri Savage confirmed gross margin should continue expanding through the year, with Q4 the expected peak as higher volumes spread fixed costs across a larger revenue base.

See historical and forward estimates for Ultra Clean Holdings stock (It’s free!) >>>

How UCTT Stacks Up Against Peers

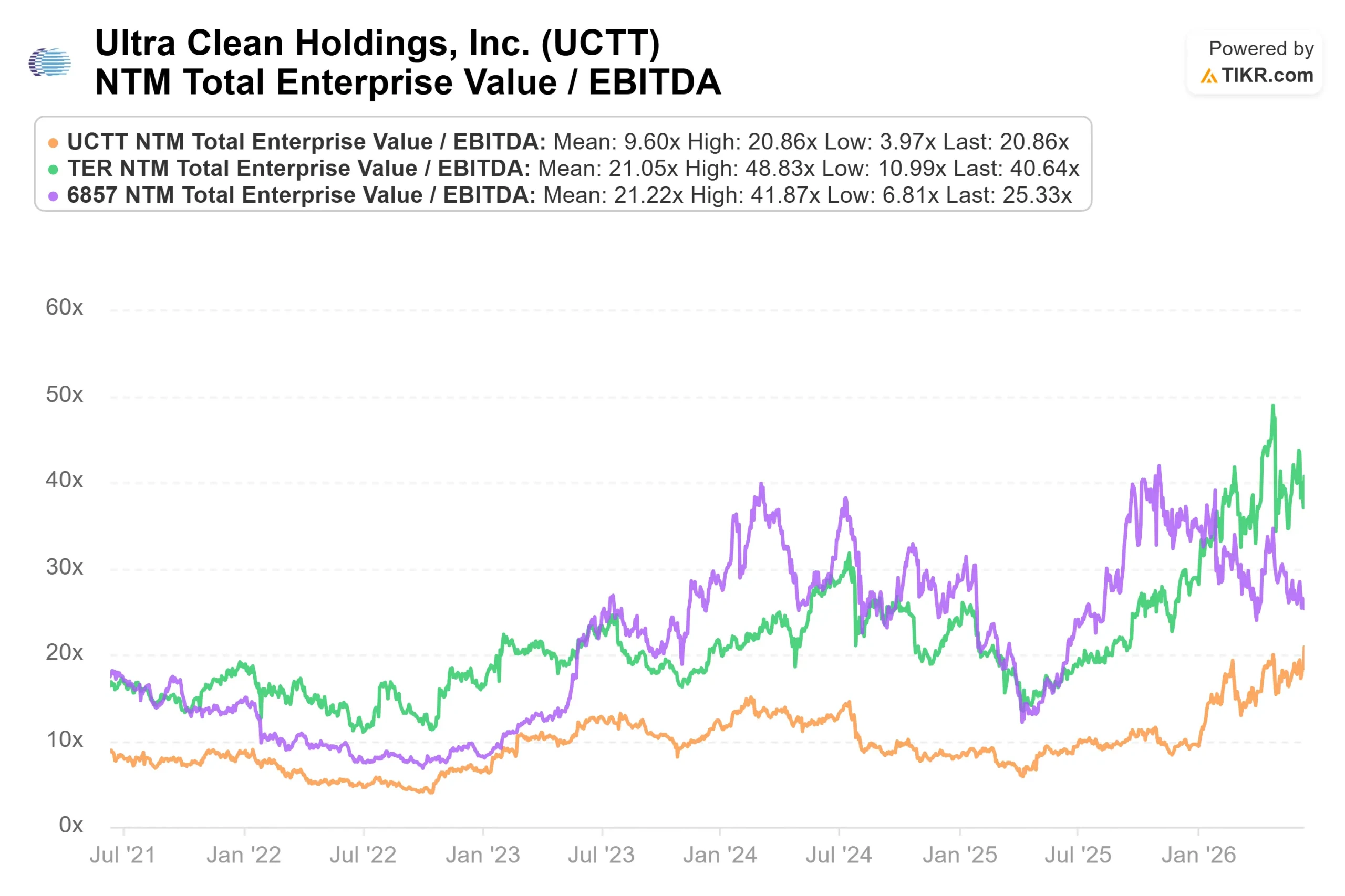

On the TIKR Competitors page, Ultra Clean trades at an NTM EV/EBITDA of 20.86x. The peer group median across 19 semiconductor equipment comparables, per TIKR’s summary statistics, sits at 25.15x. Entegris (ENTG) trades at 24.97x, Onto Innovation (ONTO) at 31.16x, FormFactor (FORM) at 37.41x, and Camtek (CAMT) at 41.55x.

That roughly 17% discount to the peer median is partly justified. Ultra Clean is a subsystem assembler rather than a full equipment maker, so its profit margins are structurally thinner. LTM gross margin is 15.6%. But part of the discount likely reflects skepticism about whether the operating leverage story will show up in the numbers. The Q1 results and Q2 guidance suggest it is beginning to.

What Bears Are Watching

Two things warrant honest attention.

First, CFO Sheri Savage announced her retirement on the Q1 earnings call, after 17 years with the company, committing to stay until a successor is named. Separately, SEC Form 4 filings show she sold approximately 14,421 shares for roughly $1.29 million on June 4, retaining 66,476 shares. The Chief Accounting Officer filed a similar sale of approximately 16,988 shares for roughly $1.52 million on the same date. Executive share sales are common near all-time highs and do not necessarily signal concern about the company’s prospects, but investors should note the activity.

Second, Q1 operating cash flow was negative $33.3 million, driven by deliberate inventory build ahead of the demand ramp. On the positive side, Ultra Clean restructured its debt in Q1: it issued $600 million in zero-coupon convertible senior notes, repaid its Term Loan B, and cut annual cash interest expense by approximately $30 million, reducing its weighted average borrowing rate from around 6.2% to approximately 1.4%. The balance sheet is materially stronger than six months ago. But free cash flow turning consistently positive is the next proof point the operating leverage thesis needs.

See how Ultra Clean Holdings performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $104.83

- TIKR Model Target (Mid): ~$125

- Potential Total Return: ~19%

- Annualized IRR: ~4% / year

See analysts’ growth forecasts and price targets for Ultra Clean Holdings stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of approximately 14% and a net income margin of around 6%, producing a target of roughly $125 and a total return of around 19% through the end of 2030, or about 4% annualized. At $105, the mid-case does not make a compelling argument for buyers who need market-beating returns.

Two revenue drivers anchor the forecast:

- WFE volume growth from the AI infrastructure buildout, with customers providing multi-year demand visibility through long-range forecasts, CEO Xiao described as “building week by week.”

- Services revenue growth tied to rising wafer starts, which management expects to compound in the double-digit range annually as newly commissioned fabs ramp production.

The margin driver is operating leverage: most of Ultra Clean’s cost structure is fixed, so incremental revenue above the current ~$2.2 billion run rate flows through at higher margins. The primary risk is timing if WFE spending plateaus before margin expansion materializes, the thesis stalls. The high case, at approximately 16% revenue CAGR and stronger margin expansion, produces a target near $220 with a total return of roughly 110% through 2030 and an IRR of approximately 9% annualized.

Conclusion

The thesis resolves at Q2 earnings, expected around July 27, 2026. Management guided Q2 revenue to $565–$605 million and EPS of $0.44–$0.60. A result at or above the $585 million midpoint with continuing sequential gross margin improvement would confirm the operating leverage story is tracking. A miss on revenue or a stall in margins would signal the ramp is not translating to financials as quickly as the Street has now priced in.

WFE commentary from TSMC, Lam Research, and Applied Materials in their upcoming earnings will also set the cycle’s forward visibility more than any single subsystem supplier can. For existing holders, the data supports patience through Q2. For new buyers at $105, the mid-case returns about 4% annually through 2030. The high case makes the math work, but only if the cycle extends, as CEO Xiao and Oppenheimer both now believe it will.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Ultra Clean Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ultra Clean Holdings, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ultra Clean Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Ultra Clean Holdings on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!