Key Stats for Adobe Stock

- Current Price: $218.80

- Target Price (Mid): ~$414

- Street Target (Mean): ~$329

- Potential Total Return (Mid): ~89%

- Annualized IRR (Mid): ~15% / year

- Earnings Reaction: -6.25% (June 11, 2026)

- Max Drawdown: 47.11%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Adobe Inc. (ADBE) posted a beat-and-raise quarter on June 11, 2026, record revenue, higher full-year guidance, and the first meaningful ARR numbers from its AI products, and the stock fell 6.25% anyway, touching a new 52-week low of $218.09. The headline numbers were not the issue. What spooked investors was CFO Dan Durn’s abrupt departure to Marvell Technology, effective June 15, dropping four days after the earnings call layered on top of an ongoing CEO search that Shantanu Narayen announced in March after 18 years in the role.

Two top-of-house transitions in three months is a lot of noise. But the TIKR data suggests the selloff is a misread, not a verdict.

What Q2 Actually Said

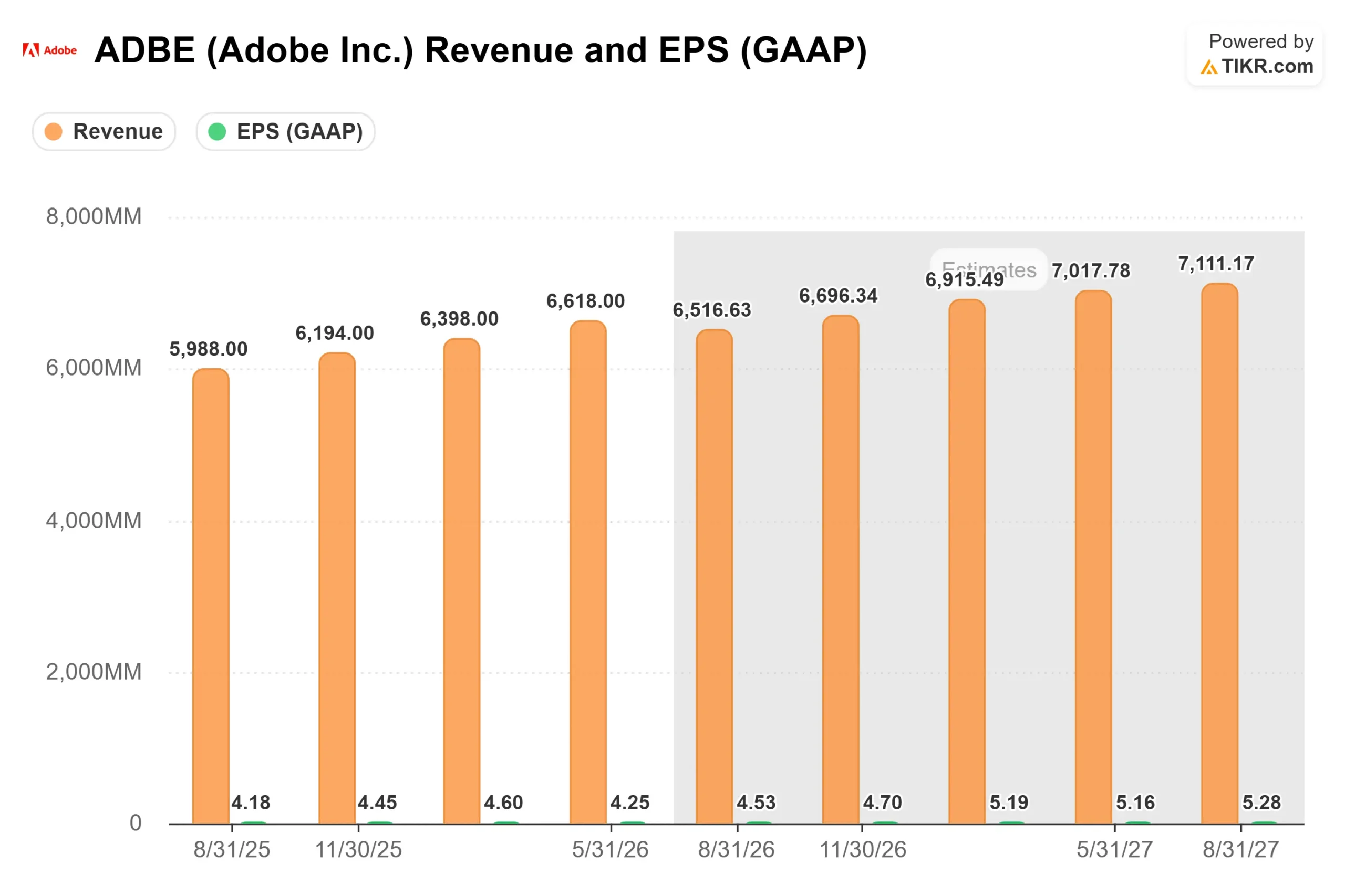

Revenue came in at $6.618 billion, growing 13% year-over-year and clearing the high end of guidance. Non-GAAP EPS hit $5.96, beating the $5.81 consensus by 2.50%. GAAP EPS of $4.25 missed the $4.45 estimate, reflecting a $70 million non-cash goodwill impairment in the Publishing and Advertising segment a legacy unit, not the core business. Full-year revenue guidance was raised to $26.5–$26.6 billion, and non-GAAP EPS guidance moved to $24.35–$24.45.

Per TIKR’s earnings surprises data, Adobe has beaten revenue estimates in each of its last five reported quarters. The Q2 revenue beat of 2.58% was the widest in that run. The one miss: free cash flow came in at $2.107 billion against a $2.273 billion estimate, a 7.31% shortfall.

The AI metrics were more consequential than any of those figures:

Creative freemium MAU grew from 50 million to 90 million year-over-year

Total Adobe ending ARR reached $27.1 billion, up 12.5% year-over-year (including ~$480M from the Semrush acquisition closed in April)

AI-first ARR tripled year-over-year and crossed $500 million

Firefly ending ARR is approaching $300 million, up ~50% quarter-over-quarter

Acrobat and Express MAU surpassed 850 million, up ~20% year-over-year

See historical and forward estimates for Adobe stock (It’s free!) >>>

The Freemium Pivot: What the Market Is Getting Wrong

The bigger concern on the call was not the CFO. It was Adobe’s decision to deliberately slow near-term ARR growth in exchange for faster freemium user acquisition across Acrobat, Express, and Firefly. Management acknowledged this clearly: roughly half the H2 ARR impact comes from rerouting traffic into friction-free product experiences instead of paid-plan landing pages, and the other half from deferring Creative Cloud pricing optimizations that had been planned for the second half.

David Wadhwani, President of Creativity and Productivity, explained the logic on the call: users who arrive through this freemium flow “convert to a paid user” with “much higher engagement and usage patterns than those that go directly into paid, which translates into long-term lifetime value.” The early data support that claim. Firefly ARR grew ~50% quarter-over-quarter. Creative freemium MAU grew 80% year-over-year. Traffic to adobe.com grew over 40% year-over-year in Q2.

CEO Narayen grounded the strategy in company history: “We actually tried to charge for the Acrobat Reader and most customers told us, ‘Allow us to use it, and you’ll find different ways to monetize it.'” The Reader model eventually anchored a $27 billion ARR business. Adobe is making the same bet on Firefly and Express, backed by traffic data that shows the top of the funnel is already working.

What the Valuation Actually Looks Like

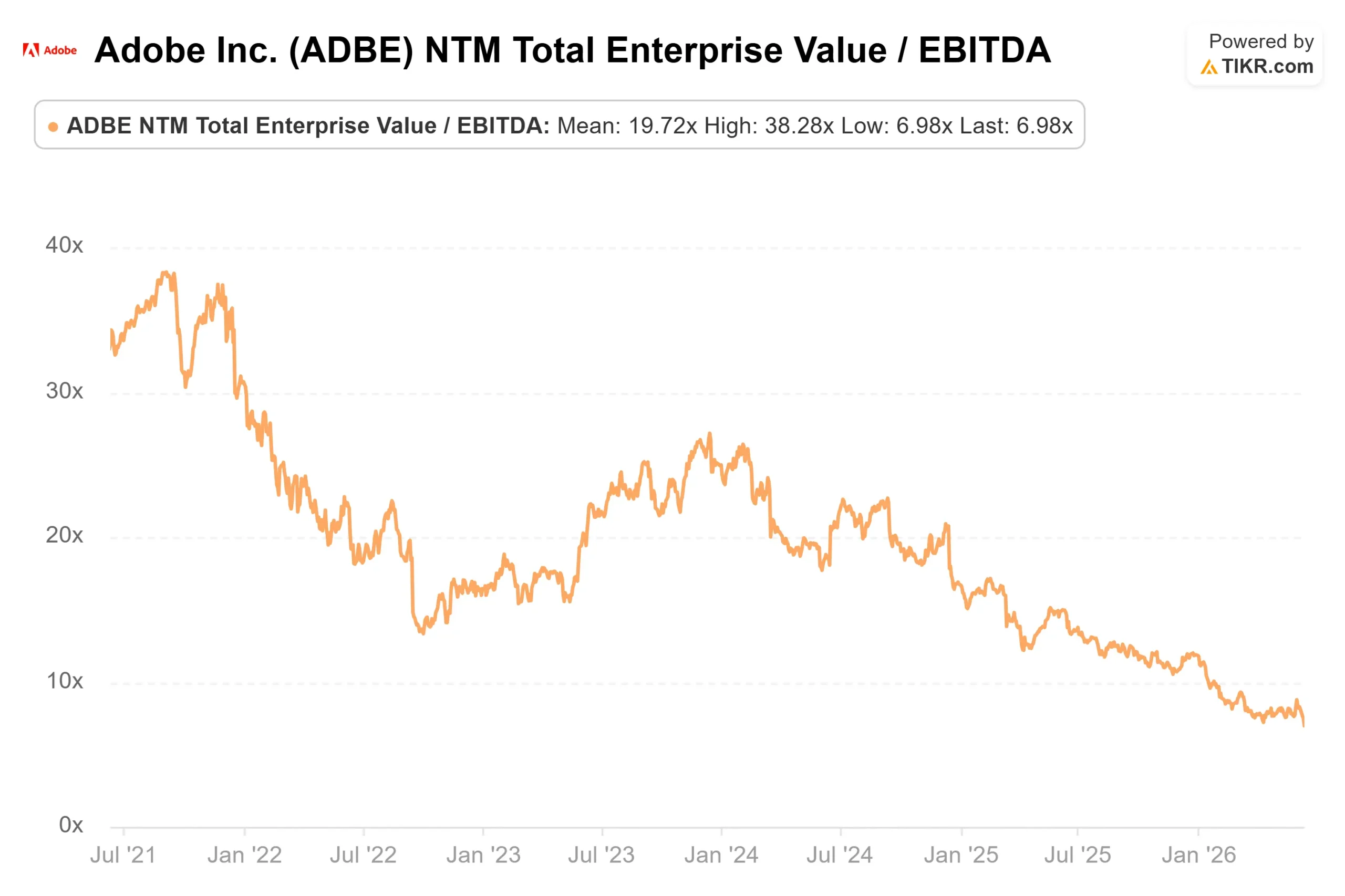

The selloff has pushed ADBE to multiples that are disconnected from the underlying business. Per TIKR’s valuation multiples data:

- NTM EV/EBITDA: 6.98x down from 14.92x a year ago

- NTM P/E: 8.83x down from 19.88x a year ago

- LTM Gross Margin: 89.4%

- LTM ROIC: 49.8%

- 3-year revenue CAGR: 10.5%

- LTM free cash flow: ~$9.3 billion

For context from TIKR’s competitors page, ServiceNow (NOW) trades at 16.05x NTM EV/EBITDA and 23.77x NTM P/E. Workday (WDAY) trades at 8.84x NTM EV/EBITDA and 11.76x NTM P/E. Adobe trades at a discount to both, despite a higher gross margin profile and consistent double-digit revenue growth. The discount reflects the AI disruption fear trade, not a change in Adobe’s fundamentals.

The Street’s own mean target of ~$329 implies around 50% upside from $218.80. Of 39 analysts covering the stock, only 15 rate it Buy or Outperform, while 20 sit at Hold, broad caution, not a consensus that the business is broken.

See how Adobe performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

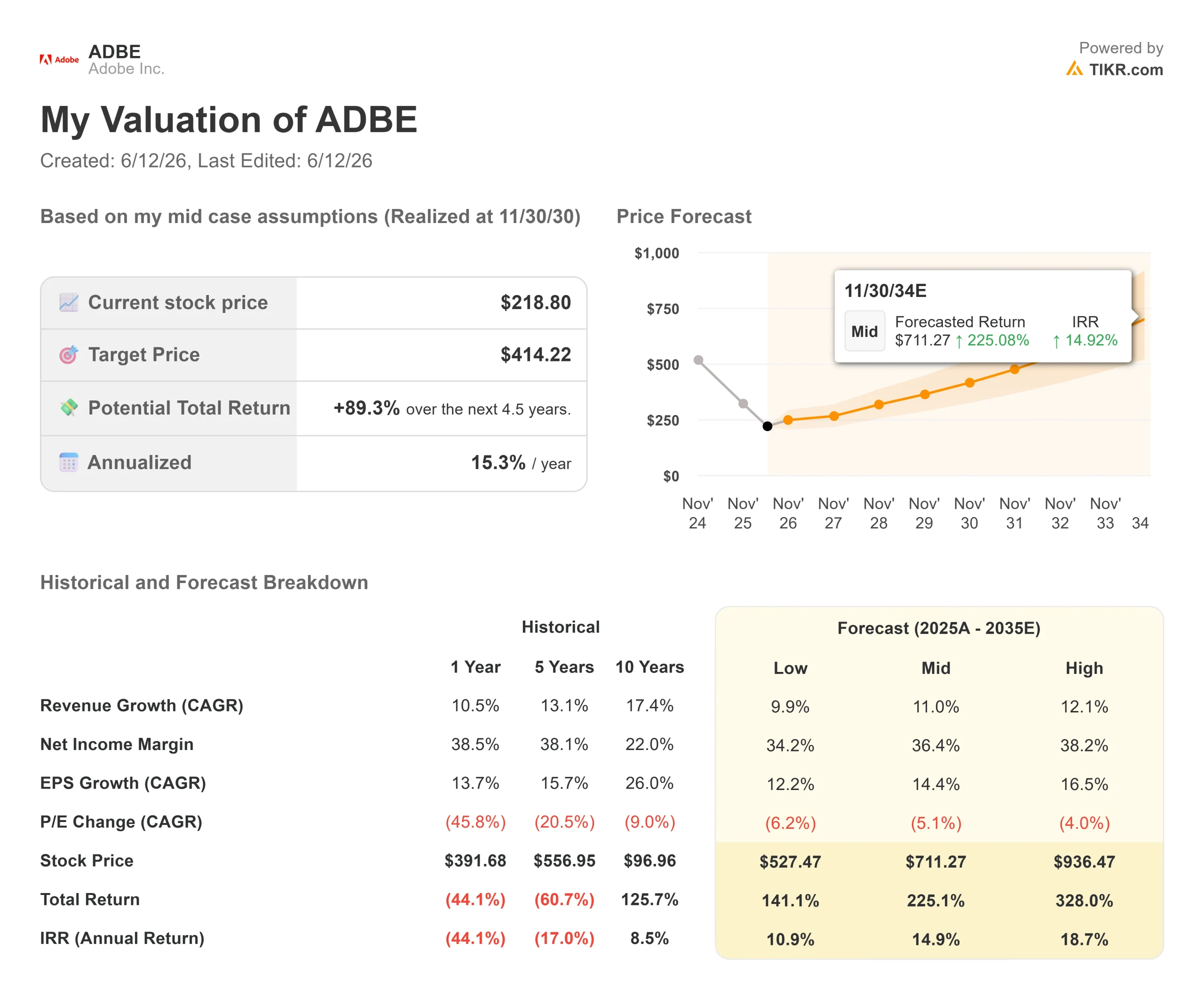

- Current Price: $218.80

- Target Price (Mid): ~$414

- Potential Total Return: ~89%

- Annualized IRR: ~15% / year

See analysts’ growth forecasts and price targets for Adobe stock (It’s free!) >>>

The mid case assumes an ~11% revenue CAGR and a net income margin of around 36%. The two revenue drivers are:

- Firefly ARR scaling from ~$300 million toward a multi-billion ARR product as the freemium funnel converts free users to paid plans

- Enterprise Customer Experience Orchestration, where AEP and native app subscription revenue grew over 30% year-over-year in Q2, and AI-first CXO ARR grew 4x year-over-year

The margin driver is operating leverage, as freemium acquisition reduces per-user acquisition cost over time. The primary risk is conversion rate disappointment if free users don’t convert to paid at the rates management projects, ARR growth undershoots, and the thesis breaks.

The low case puts the annualized return at around 11%. The high case puts it near 19%. Both require Adobe to sustain revenue growth at or near 10% per year, which it has delivered consistently across its last decade of reported results.

Conclusion

The number to watch is Q3 fiscal 2026 net new Digital Media ARR, due around September 2026. Management said on the call that ARR will be more back-half weighted this year Q3 will look soft by design as traffic rerouting takes hold, with enterprise strength expected to load into Q4.

The threshold: if Firefly ending ARR continues its ~50% quarter-over-quarter pace and approaches ~$400 million by the Q3 print, the monetization proof point is intact. If it stalls, the freemium bet is underperforming and the bear case gains real ground.

At $218.80, Adobe trades under 9x forward earnings with an 89.4% gross margin, a net cash balance sheet, and $27 billion remaining on its buyback authorization. The Street’s own consensus calls it 50% underpriced. Leadership transitions and a deliberate ARR slowdown are real headwinds but they are not the same as structural impairment. The market is currently pricing them as if they are.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Adobe?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Adobe, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Adobe alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!