Key Stats for AMD Stock

- Current Price: $485.63

- TIKR Model Target (Mid, Dec. 2030): ~$1,757 (model entry: $452.40)

- Potential Total Return (Mid): ~288%

- Annualized IRR (Mid): ~35% / year

- Q1 2026 Earnings Reaction: +18.61% (May 5, 2026)

- Max Drawdown: 27.76% (March 3, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Advanced Micro Devices (AMD) had a disorienting stretch even by 2026 standards. The stock dropped nearly 11% on June 5, swept into a chip-sector selloff triggered by Broadcom’s earnings non-raise, then bounced more than 5% three days later. On June 12, the analyst who had spent an hour questioning AMD’s CFO at his firm’s conference ten days earlier raised his price target to $560 and his server CPU market forecast to more than $170 billion.

The selloff was noise. The upgrade is the story.

Bank of America’s Vivek Arya raised his AMD target to $560 from $500, named AMD his top CPU pick, and cited the upcoming Venice launch at AMD’s Advancing AI 2026 event as a near-term catalyst. That event is scheduled for July 22-23 in San Francisco. Arya increased his 2030 server CPU total addressable market estimate to more than $170 billion from $125 billion, implying nearly fivefold growth and a CAGR of more than 37% from 2025 to 2030.

What makes the upgrade compelling is that Arya had just sat across from AMD CFO Jean Hu and Head of IR Matt Ramsay at BofA’s own Global Technology Conference on June 2. What they said in that room explains why he moved the number.

What AMD’s CFO Said That Street Targets Don’t Fully Reflect

The existing AMD narrative is established. Q1 2026 revenue came in at $10,253 million, up 38% year-over-year, with the Data Center segment hitting a record $5.8 billion, up 57%, per AMD’s Q1 2026 earnings release. AMD guided Q2 revenue to approximately $11.2 billion, implying around 46% year-over-year growth, and server CPU revenue specifically is expected to grow more than 70% year-over-year in Q2.

What the June 2 conference added is more granular.

CFO Jean Hu broke the server CPU market into three buckets. Traditional general-purpose compute is a $25 to $30 billion market with steady, moderate growth. Head nodes, which coordinate communication between servers and GPUs, will grow faster as GPU cluster sizes expand. But the third segment is where Hu placed the emphasis.

“Agentic AI server racks sit in between the traditional servers and the GPUs,” she said. “Those racks are handling all those different workloads to really make sure all the agentic agents work. That market, whatever, the $120 billion or $200 billion market opportunity, is the majority of that large market.”

Agentic AI refers to automated multi-step workflows where software agents plan, retrieve data, and chain tasks without human intervention. According to AMD’s own CFO, that segment is not the fringe of the CPU opportunity. It is the center.

Matt Ramsay, AMD’s Head of IR, connected the thesis directly to product demand. “The order book fills in for the 256-core 2-nanometer Venice parts that are going to launch in a couple of months and be the primary workhorse for next year,” he said. “That’s where we’re seeing the order book really expand.”

Venice, AMD’s next-generation EPYC CPU built on TSMC’s 2nm process, supports up to 256 Zen 6 cores, a 33% increase over the current Turin generation, targeting AI, cloud computing, and high-performance analytics workloads.

The Infrastructure Setup Going Into H2 2026

AMD’s anchor customer visibility is unusually clear. Both OpenAI and Meta have committed to multi-gigawatt MI450 GPU deployments per AMD’s published press releases, and at the June 2 conference, Hu confirmed both customers are now forecasting above AMD’s original 2027 plan. The Helios rack, AMD’s first rack-scale AI system, is on track for a Q3 2026 production ramp, with Ramsay describing “a pretty significant jump in Q4 revenue.”

On server CPUs, AMD reached a record 46.2% of x86 server CPU revenue share in Q1 2026, according to Mercury Research, up from 41.3% in Q4 2025. That share gain was confirmed directly by Hu at the conference, who said AMD got to “like 46%” on a value share basis.

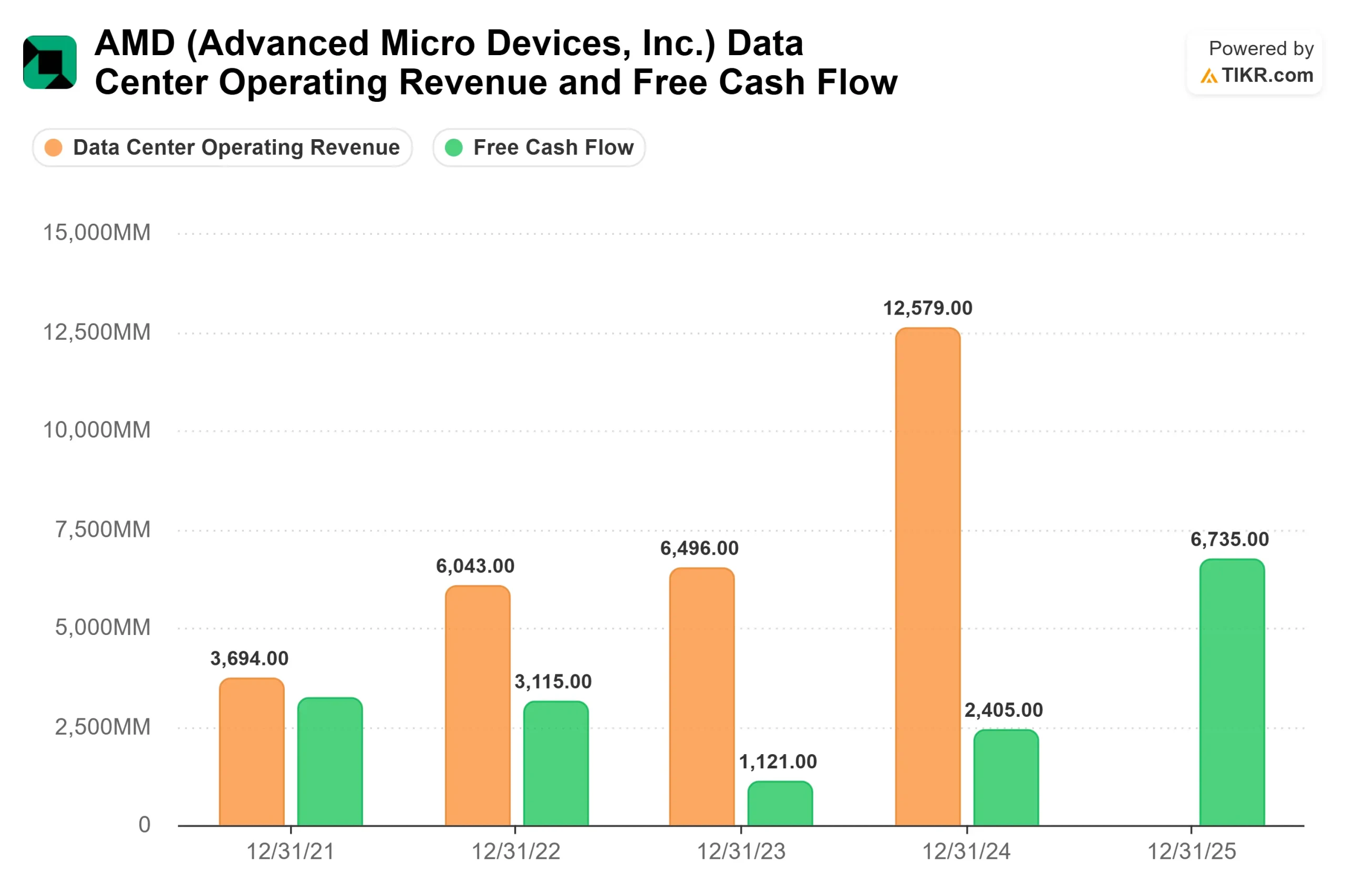

The free cash flow picture confirms the business is converting AI demand into cash. AMD generated $7,173.38 million in LTM levered free cash flow per TIKR, up from $2,304.25 million two years prior. TIKR consensus estimates project free cash flow growing to around $8.3 billion for full-year 2026.

The risk is real and sits in the valuation. AMD’s NTM EV/EBITDA of 44.5x is more than double the semiconductor peer group mean of around 21x per TIKR’s Competitors data, with Nvidia at 16.1x and Broadcom at 19.0x. The MI450 Helios ramp carries below-corporate gross margins in its early quarters, which Hu acknowledged at the conference. Memory cost inflation is creating headwinds in gaming and consumer PCs. And the June 5 selloff showed how quickly sector sentiment can reprice AMD even when the company’s own fundamentals haven’t changed.

See historical and forward estimates for AMD stock (It’s free!) >>>

Is the Premium Justified? What the Numbers Say

The Street consensus per TIKR sits at 36 Buys, 5 Outperforms, 10 Holds, and 0 Sells across 48 analyst estimates, with a mean price target of $482.69 and a Street high of $665.00. BofA’s freshly raised $560 sits in the middle of that range.

The case for the premium rests on the revenue trajectory. TIKR consensus estimates project revenue growing around 43% in 2026 to approximately $49.4 billion, followed by around 54% growth in 2027 to approximately $76.2 billion. A company compounding revenue near 50% annually has earned a higher valuation multiple than peers growing at mid-single digits.

But the current price is already pricing in clean execution. Venice launching on time, Helios ramping at scale into Q4, and MI450 volumes meeting anchor customer forecasts all need to go right simultaneously. Anyone slipping could reprice the stock sharply, even in a strong AI demand environment.

See how AMD performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $485.63

- TIKR Model Target (Mid): ~$1,757 (model entry: $452.40)

- Potential Total Return (Mid): ~288%

- Annualized IRR (Mid): ~35% / year

See analysts’ growth forecasts and price targets for AMD stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of around 42% from 2025 through 2035. The two primary revenue drivers are Data Center AI GPU revenue from the MI450 and Helios ramp, and server CPU revenue from the Turin-to-Venice transition. The margin driver is operating leverage: net income margins are forecast to expand from around 20% at the LTM level toward roughly 35% by 2030 as the high-margin Data Center mix becomes dominant.

If AMD executes on Helios, Venice ships on time, and the agentic AI rack market expands toward BofA’s $170 billion estimate, the ~$1,757 mid-case target by 2030 could prove conservative. If MI450 ramp volumes disappoint, Venice slips, or the semiconductor multiple compresses toward the peer mean, the downside would be significant even on a growing earnings base.

Conclusion

The most important date on the AMD calendar is July 22, when AMD’s Advancing AI 2026 event opens in San Francisco, and Venice makes its full commercial debut. BofA named that event specifically in its upgrade note today.

“Good” means Venice ships on schedule, Helios volumes step up meaningfully in Q4, and Q2 revenue lands at or above AMD’s $11.2 billion guidance. “Bad” means a Venice slip, MI450 volumes below anchor customer forecasts, or margin compression exceeding guidance.

The TIKR mid-case of ~$1,757 by December 2030 suggests BofA’s $560 target is a 12-month number, not a destination. July 22 is when the market gets its first real read on whether that longer path is intact.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in AMD?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMD, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMD alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!