Key Takeaways for MercadoLibre Stock

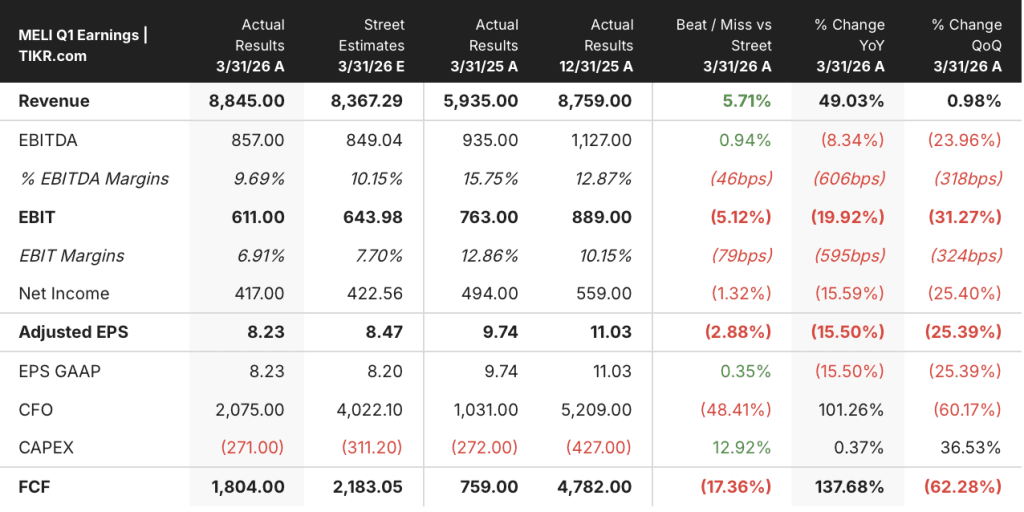

- Revenue grew 49% year-over-year to $8.85 billion in Q1 2026, the fastest growth rate since Q2 2022.

- Operating margins compressed from 13% in Q1 2025 to 7% in Q1 2026, a deliberate consequence of accelerated investment in credit cards, logistics, and free shipping.

- MercadoLibre’s credit portfolio nearly doubled to $14.6 billion, with credit card TPV growing 90% year-over-year.

- TIKR’s mid-case values MELI stock at approximately $8,449 by December 2030, implying around 425% total return from the current price of $1,610.

MercadoLibre Posts Its Fastest Revenue Growth in Four Years While Deliberately Compressing Margins

MercadoLibre, Inc. (MELI), the dominant e-commerce and fintech ecosystem in Latin America, delivered $8.85 billion in net revenue in Q1 2026, a 49% year-over-year increase that CFO Martin de Los Santos called the company’s strongest growth rate since Q2 2022.

The headline number landed ahead of Street estimates of $8.37 billion.

The growth was not an accident.

Brazil, MercadoLibre’s largest commerce market, drove the quarter with gross merchandise volume (GMV) up 38% year-over-year while items sold accelerated to 56% growth. The catalyst was a decision made several quarters ago to lower the free shipping threshold, a move that broadened the buyer base and supercharged purchase frequency.

Cost per shipment fell 17% year-over-year in local currency even as volume surged 56%, a combination that signals the logistics network is achieving meaningful scale efficiencies.

De Los Santos pointed to a specific mechanism on the Q1 earnings call: “By bringing more buyers into the ecosystem, we’re strengthening network effects with higher purchase frequency, broader assortment and a logistics network that becomes more efficient with every incremental package.”

Fintech momentum compounded the commerce story. Mercado Pago monthly active users grew 29% year-over-year. Assets under management grew 77%. The credit portfolio nearly doubled to $14.6 billion. Credit card TPV specifically grew 90%, with MercadoLibre issuing 2.7 million new credit cards in the quarter alone.

Against all of this, the company delivered $611 million in operating income at a 7% margin. Operating margins compressed from 13% a year ago. Management’s message was unambiguous: the compression is a choice, not a condition. De Los Santos closed the call by stating the company is “as confident as ever that the choices we’re making today will maximize long-term cash flow and will lead us to significantly higher margins over time.”

Is MercadoLibre Stock Undervalued in 2026? The Revenue Engine Says Yes, the Operating Line Says Not Yet

MercadoLibre stock’s revenue profile is exceptional by any measure.

Total revenues reached $8.85 billion in Q1 2026, up from $5.94 billion a year earlier, a 49% year-over-year increase that accelerated from the 45% posted in Q4 2025 and the 34% posted in Q1 2025.

Gross profit grew 39% year-over-year to $3.86 billion, with gross margins at 44% in the most recent quarter, stable relative to the 47% posted a year ago.

The gross margin story is relatively contained; the real mechanism driving the investment debate sits one level lower.

MercadoLibre stock’s operating margin compressed from 13% in Q1 2025 to 7% in Q1 2026, a 6-point contraction driven by three specific cost lines: provisions for bad debts jumped from $0.60 billion to $1.24 billion year-over-year, SG&A rose from $0.85 billion to $1.31 billion, and R&D increased from $0.55 billion to $0.70 billion.

The provision growth is the single largest margin drag and the most analytically important line.

Management confirmed on the call that two-thirds of the provision increase comes from the natural accounting consequence of a rapidly growing credit book. When a new loan or credit card is issued, the expected loss must be provisioned immediately. A credit portfolio growing at 87% year-over-year against revenue growing at 49% mechanically compresses margins even when the underlying credit business is profitable on a unit basis.

MercadoLibre stock’s operating income declined 20% year-over-year to $611 million in Q1 2026, the steepest year-over-year decline in the data set, while revenue grew at the fastest rate in four years. That is the core tension the income statement presents: the business is growing faster than ever at the same time the operating line looks worst.

The resolution depends on whether the credit book matures and provisions normalize, whether logistics cost efficiencies continue to improve, and whether the free shipping investment converts into durable market share gains that justify reduced take rates.

MELI Trades at the Lowest Operating Margin of Its Peer Group as PDD Holds an 18% Advantage

MercadoLibre stock posted a 7% operating margin in Q1 2026, the weakest reading in the eight-quarter dataset, while PDD Holdings (PDD) delivered 18% and Sea Limited (SE) reached 8% in the same period.

The gap between MELI and PDD has been structurally wide throughout the comparison window, with PDD operating at 34% in Q2 2024 before compressing to 18% by Q1 2026, a range that MercadoLibre stock has never approached across any single quarter in the dataset.

Sea Limited’s trajectory tells a more instructive story for MELI investors: SE expanded from 2% operating margins in Q2 2024 to 8% in Q1 2026, a six-point recovery achieved while scaling its own commerce and fintech operations across Southeast Asia, and SE now sits marginally above MELI for the first time across this entire dataset.

The competitive read is not that MercadoLibre is operationally inferior, but that both MELI and SE are running at similar investment intensity while PDD operates a structurally different cost model, and the question the peer data sharpens is whether MercadoLibre stock’s margin trajectory over the next eight quarters looks more like PDD’s compression story or Sea’s recovery arc.

TIKR’s $8,449 Target on MELI Stock: What Has to Hold for the Long-Duration Case to Work

TIKR’s mid-case values MELI stock at approximately $8,449 by December 2030, implying around 425% total return from the current price of $1,610, or roughly 44% annualized over 4.5 years.

If MercadoLibre’s credit portfolio matures on schedule, provisions normalize as a share of revenue, and the revenue CAGR holds near the mid-case assumption of roughly 24%, the TIKR model reaches approximately $8,449 and an annualized return of around 44%.

If growth slows to the low-case CAGR of around 22%, the model produces approximately $12,372 by December 2034, implying around 27% annualized over the longer horizon.

If execution accelerates through Brazil credit card scale, Argentina expansion, and continued logistics efficiency gains, the high case reaches approximately $24,841 by December 2034 at roughly 38% annualized.

What Did MercadoLibre Say About Margins on the Q1 2026 Call?

Management framed margin compression as a deliberate choice driven by credit card scaling, logistics expansion, and free shipping investment.

De Los Santos stated clearly that “we are not optimizing short-term margins,” and that the company could dial investment intensity up or down based on results.

Two-thirds of the current provision increase is a mechanical consequence of credit book growth, not credit quality deterioration, per management’s own waterfall analysis presented on the call.

Is MercadoLibre Stock a Buy Right Now?

MercadoLibre stock is trading at $1,610, near the bottom of its 52-week range of $1,495 to $2,645.

The core bull case rests on whether today’s margin compression is a temporary function of credit portfolio seasoning and logistics investment rather than structural deterioration. Revenue grew 49% in Q1 2026, the fastest in four years.

The valuation gap narrows significantly if operating margins recover toward historical levels as the credit book matures.

Should You Invest in MercadoLibre, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MercadoLibre, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MercadoLibre, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MELI stock on TIKR for Free →