Key Takeaways for Domino’s Pizza Stock

- Operating income grew 6% year-over-year to $220 million in Q1 2026, outpacing total revenue growth of 4%.

- Operating margins held at 19%, expanding from 18% in the year-ago quarter and holding steady across the trailing eight quarters.

- Gross margins ticked up to 29% in Q1 2026, a new high in the trailing eight-quarter data set.

- TIKR’s mid-case model values Domino’s Pizza stock at approximately $546 by December 2030, implying around 75% total return from the current price of $312.

Domino’s Posts Positive U.S. Order Count Growth in Q1, But Macro Pressure Clouds a Tighter Income Story

Domino’s Pizza, Inc. (DPZ) reported Q1 2026 same-store sales growth of 0.9% in the U.S., falling short of management’s 3% target following an intensification of macro headwinds and competitive pressure in March.

The company operates through three segments: U.S. stores (mostly franchised), international franchise, and supply chain, which manufactures and distributes food and supplies to the franchise network.

U.S. retail sales grew 2.8% in the quarter, supported by positive order counts across all income cohorts and net new store additions that brought the U.S. system to more than 7,200 locations.

The supply chain segment remained a structural anchor, with CFO Sandeep Reddy citing gross margin dollar growth and procurement productivity as the primary driver of operating income that came in 4.2% higher year-over-year, excluding foreign currency and a one-time gain on the sale of corporate aircraft.

Consumer sentiment was the central headwind. CEO Russell Weiner described conditions directly on the Q1 earnings call: “Consumer sentiment hit COVID-level lows and ongoing inflation continued to impact purchase decisions.”

Competitive activity from national pizza peers intensified in the quarter, with rivals matching Domino’s promotional formats. Weiner framed the dynamic as structurally self-defeating for competitors: the company’s advertising budget, which Weiner said is as large as the two biggest competitors combined, enables Domino’s to sustain value offers profitably in a way its rivals cannot.

Internationally, same-store sales declined 0.4% on a constant currency basis, driven largely by underperformance at Domino’s Pizza Enterprises (DPE), the brand’s largest global master franchisee. Excluding DPE, the international segment would have met expectations.

Looking to the rest of 2026, management revised its U.S. same-store sales guidance to positive low single digits from the prior 3% target, while maintaining its unit growth outlook of 175-plus net new U.S. stores and approximately 800 internationally.

Is Domino’s Pizza Stock Undervalued? Operating Leverage Is Quietly Compounding

Domino’s Pizza stock’s revenue grew 4% year-over-year to $1.15 billion in Q1 2026, a deceleration from the 6% pace of the prior two quarters but consistent with the company’s low-single-digit growth profile.

The more important story is what happened beneath the revenue line: gross margins expanded to 29% in Q1 2026, up from 28% in the year-ago quarter and the highest reading in the eight-quarter data set provided.

Domino’s Pizza stock’s operating income grew faster than revenue in the quarter, rising 6% year-over-year to $220 million, with operating margins holding at 19%, up from 18% a year prior.

SG&A remained flat at $110 million quarter-over-quarter and year-over-year, which means the gross margin expansion flowed directly into operating income without being consumed by overhead growth.

Across the trailing eight quarters, operating margins have ranged from 18% to 20%, with the most recent four quarters (Q1 2025 through Q1 2026) all printing at 19% or above, a regime shift from the 17% to 18% range that prevailed through mid-2024.

This is operating leverage working as it should in a franchise-and-supply-chain model: revenue rises modestly, gross profit follows at a faster rate, and a flat SG&A structure lets the incremental margin flow to operating income with minimal friction.

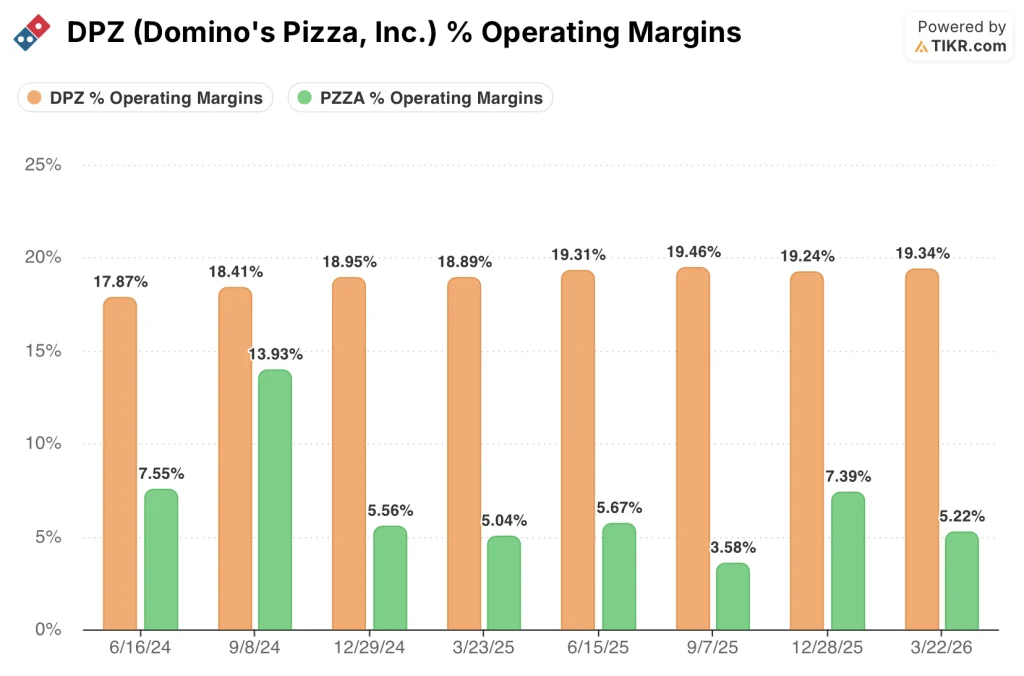

Domino’s Operates at 19% Operating Margins While Papa John’s Has Never Topped 14%

Domino’s Pizza stock runs at 19% operating margins in the most recent quarter, a figure Papa John’s International (PZZA) has not come close to matching across the full eight quarters of comparative data.

Papa John’s operating margins peaked at 14% in Q3 2024 before collapsing to 4% by Q3 2025, a swing of 10 percentage points in three quarters that illustrates the structural fragility of a thinner-margin pizza operator without Domino’s vertically integrated supply chain.

Domino’s Pizza stock’s operating margin floor across the same eight-quarter window was 18%, meaning its worst quarter still outperforms Papa John’s best quarter by 4 percentage points, a gap that is not cyclical noise but a function of two fundamentally different business architectures.

The implication for the thesis is direct: Papa John’s margin volatility requires investors to price in operational risk that simply does not exist in Domino’s income statement, which is one reason the current price of $312 looks like a discount to a business whose margin structure has demonstrated it can hold through COVID-level consumer sentiment readings, competitive promotional wars, and macro pressure simultaneously.

TIKR’s $546 Target on DPZ Stock: What Has to Hold Through 2030

TIKR’s base case values Domino’s Pizza stock at approximately $546 by December 2030, implying around 75% total return from the current price of $312, or roughly 7% annualized over the next 4.5 years.

If Domino’s executes on its mid-case revenue growth assumptions and operating margins remain in the 19% to 20% range consistent with recent quarters, the model prices the stock at approximately $546, with an annualized return of around 7%.

If growth accelerates toward the high end and the multiple holds, TIKR’s high case puts the stock at approximately $639 by December 2030, implying around 105% total return and roughly 9% annualized.

If same-store sales remain suppressed and the valuation multiple compresses further, the TIKR low case values the stock at approximately $452, still implying around 45% total return and roughly 4% annualized, which means even the bear scenario assumes the current price represents a discount to intrinsic value.

Is Domino’s Pizza Stock a Buy Right Now?

At $312, Domino’s Pizza stock trades near its 52-week low of $329, despite operating margins that have held at 19% for four consecutive quarters and operating income that grew 6% year-over-year in Q1 2026.

TIKR’s mid-case model prices the stock at approximately $546 by December 2030.

Whether the stock is a buy depends on whether an investor believes the current macro headwinds are temporary and the operating leverage story holds.

Should You Invest in Domino’s Pizza, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Domino’s Pizza, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Domino’s Pizza, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DPZ stock on TIKR for Free →