Key Takeaways for Pegasystems Stock

- Pega Cloud revenue grew 36% year-over-year to $205 million in Q1 2026, while total revenue fell 10% to $429.97 million.

- Gross margins compressed from 79% in Q3 2025 to 75% in Q1 2026, with operating margins falling from 25% to 9%.

- Pega Cloud ACV reached just over $900 million, growing 29% year-over-year and now representing 56% of total ACV.

- TIKR’s mid-case values Pegasystems stock at approximately $70 by December 2030, implying around 112% total return from the current price of $33.

Take control of the PEGA setup before the crowd does. TIKR puts the full income statement history, ACV trajectory, and valuation model in your hands, for free. Analyze Pegasystems stock on TIKR for free →

Pegasystems Stock’s Cloud Engine Is Running Hot While the Rest of the Business Cools

Pegasystems (PEGA) is a Waltham, Massachusetts-based enterprise software company whose platform helps large organizations automate complex workflows, manage customer interactions, and govern AI-driven processes at scale, and following Q1 2026 earnings on April 22, the stock sits at $33 after falling roughly 50% from its 52-week high of $68.

The headline looked ugly.

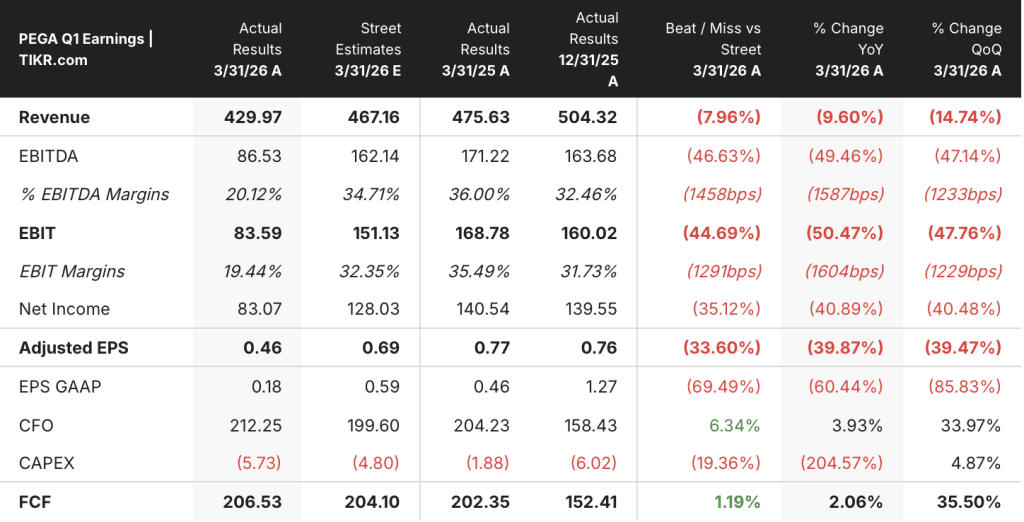

Total Q1 revenue came in at $429.97 million, down 10% year-over-year and roughly $37 million below what analysts had expected, a miss driven almost entirely by the timing of term license revenue, which is recognized upfront when a client renews and can swing sharply quarter to quarter.

But CFO Ken Stillwell had been clear heading into the quarter: “We entered the year knowing the first quarter would also be a challenging comparison given the $60 million of net ACV add in the first quarter of 2025, which was very much an outlier and roughly 20% higher than any other quarter last year.”

Pega Cloud revenue, the business that actually tells you whether enterprise buyers are committing to the platform, grew 36% year-over-year to $205 million, with Pega Cloud Annual Contract Value (ACV), the total annualized value of subscription contracts, reaching just over $900 million and approaching the $1 billion mark for the first time.

Total ACV across all product lines reached $1.622 billion, up 12% year-over-year, with Pega Cloud now representing 56% of the total base and management targeting 75% or more over time.

Two macro factors also created noise: a federal government shutdown disrupted procurement in March, causing several government renewals to slip, and geopolitical tensions in Europe, which accounts for roughly 30% of Pega’s business, added additional caution in the region.

The strategic case at PegaWorld in June was sharper.

Stillwell revealed that total pipeline is up 29% year-over-year, with new logo pipeline specifically up 65%, driven by Blueprint AI, Pega’s workflow design tool that allows enterprise buyers to prototype and build new applications faster than traditional implementation cycles.

The Q3 and Q4 renewal concentration, a pattern typical for Pega in most years, means the back half of 2026 carries the real test of whether that pipeline converts.

Is Pegasystems Stock Undervalued? The Income Statement Has a Compression Problem and a Compounding One

Pegasystems stock’s gross margin fell from 79% in Q3 2025 to 75% in Q1 2026, a compression that matters because gross margin is the starting point for every dollar of operating profit, and it is moving in the wrong direction at the wrong moment.

Gross profit came in at $0.32 billion in Q1 2026, down from $0.37 billion in Q1 2025, as Cost of Goods Sold held steady at $0.11 billion even as revenue fell, which means the fixed cost base inside gross profit is not declining with volumes.

The operating leverage story is where Pegasystems stock gets genuinely interesting: revenue has now declined year-over-year in two of the last five quarters, but Total Operating Expenses have risen steadily from $0.24 billion in mid-2024 to $0.29 billion in Q1 2026, widening the gap between what the business earns at the gross line and what it retains at the operating line.

Operating income for Q1 2026 came in at $0.04 billion, with operating margins of 9%, compared to 25% in Q3 2025 and 27% in Q1 2025, a pattern that shows the business produces healthy margins in strong revenue quarters and compresses sharply when term license timing works against it.

The SG&A line, which expanded from $0.17 billion in mid-2024 to $0.20 billion in Q1 2026, is the primary driver of operating expense growth, with R&D holding relatively flat at $0.08 billion throughout the period, suggesting the investment is weighted toward go-to-market rather than engineering.

The key question inside Pegasystems stock’s income statement is whether Pega Cloud revenue, which carries a 78% gross margin on a trailing basis and grew 36% year-over-year in Q1, can scale fast enough to absorb the SG&A load and bring structural operating margins back to the mid-20s, where the business has historically settled in strong delivery quarters.

Pegasystems Stock Trades at Gross Margin Parity With ServiceNow, But Appian’s Discount Reveals a Different Risk Profile

Pegasystems stock’s 75% gross margin in Q1 2026 matches ServiceNow (NOW) almost exactly, with NOW printing 75% in the same period, a convergence that runs across the full eight-quarter comparison and suggests the gross margin compression flagged in the Financials section is not a Pega-specific structural problem.

Appian (APPN), the third platform in the peer set, tells a different story: APPN posted 73% gross margins in Q1 2026, running below both PEGA and NOW for most of the period shown, with the exception of a brief 80% peak in Q4 2024 that proved transitory and was followed by a return to the low 70s.

What the eight quarters of data establish is that all three workflow and low-code platform businesses operate in a tight gross margin band between 70% and 80%, which means Pega’s Q1 2026 compression from 79% to 75% looks far less alarming in peer context than it does in isolation, and the question for Pegasystems stock shifts from whether the gross margin structure is broken to whether Pega Cloud’s growing revenue mix can push the line back toward the high 70s where the business has historically settled when term license timing is favorable.

Is Pegasystems Stock a Buy? TIKR’s $70 Mid-Case Says Yes, With Conditions

TIKR’s mid-case values Pegasystems stock at approximately $70 by December 2030, implying around 112% total return from the current price of $33, or roughly 9% annualized over approximately 4.6 years.

If revenue grows at approximately 9% annually through 2030 and net income margins expand toward approximately 25%, as the TIKR base case projects, the path to $70 runs through a sustained Pega Cloud ACV ramp, successful Blueprint-driven new logo conversion in the second half of 2026, and SG&A leverage emerging as the sales motion matures.

If the Blueprint pipeline converts at lower rates than expected and term license revenue stays depressed through year-end, the TIKR low case targets approximately $54, implying around 64% total return or roughly 6% annualized, still positive but contingent on cloud mix continuing to build.

If ACV growth accelerates toward 10% annual revenue growth and margin expansion arrives faster than the base case assumes, the TIKR high case reaches approximately $88 by December 2030, implying around 168% total return or roughly 12% annualized.

Is Pegasystems Stock a Buy Right Now?

Pegasystems stock is trading near its 52-week low of $33 following a Q1 2026 revenue miss, with total revenue down 10% to $429.97 million.

The miss was driven by term license timing, not cloud fundamentals: Pega Cloud revenue grew 36% year-over-year to $205 million and Pega Cloud ACV crossed $900 million.

For investors focused on the recurring revenue base, current levels represent a historically wide discount to intrinsic value by most institutional frameworks, though the back-half revenue recovery is not guaranteed.

Is Pegasystems Stock Undervalued in 2026?

At $33, Pegasystems stock trades at roughly half its 52-week high of $68. TIKR’s mid-case model targets approximately $70 by December 2030, implying around 112% total return.

The core valuation argument rests on operating margin recovery: the business printed 25% operating margins in Q3 2025 and 27% in Q1 2025, but compressed to 9% in Q1 2026 when term license revenue was soft.

If cloud mix drives structural margin recovery, the current price embeds pessimism that the income statement does not fully support.

What Did Pegasystems Say About AI at PegaWorld 2026?

At PegaWorld on June 8 in Las Vegas, CEO Alan Trefler and CFO Ken Stillwell made the case that the shift toward AI governance and predictable cost structures plays directly to Pega’s architecture.

Stillwell noted that total pipeline is up 29% year-over-year, with new logo pipeline up 65%, and announced that Pega would not charge customers for tokens inside its platform, a structural differentiation as frontier model providers tighten monetization.

The product announcement centered on Infinity Studio, which brings Blueprint’s AI design capabilities into the full application development environment.

Should You Invest in Pegasystems Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Pegasystems stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pegasystems stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PEGA stock on TIKR for Free →