Key Takeaways for Intuit Stock

- Q3 fiscal 2026 revenue reached $8.56 billion, growing 10% year over year, exceeding the top end of guidance.

- Gross margins held at 84% in Q3, while operating margins expanded to 47% as cost discipline offset softer DIY tax volumes.

- TurboTax Live customers grew 38% this fiscal year and now represent 53% of total TurboTax revenue, up 11 points from last year.

- TIKR’s mid-case values Intuit stock at approximately $469 by July 2030, implying around 65% total return from the current price of $284.

Intuit Stock Beat Estimates and Announced 17% Layoffs on the Same Day

Intuit Inc. (INTU), the financial technology company behind TurboTax, QuickBooks, Credit Karma, and Mailchimp, reported fiscal Q3 2026 results on May 20 that cleared every guidance metric while simultaneously announcing it would cut 17% of its full-time workforce.

Revenue of $8.56 billion came in above the top of guidance and grew 10% from the prior year period.

Non-GAAP diluted earnings per share reached $12.80, up from $11.65 a year ago and ahead of the $12.57 analyst consensus.

The company raised full-year revenue guidance to $21.341 billion to $21.374 billion, implying 13% to 14% growth, with non-GAAP EPS guided to $23.80 to $23.85.

CEO Sasan Goodarzi described the layoff rationale directly in Q3 earnings call: “We are reducing our full-time workforce by 17% to simplify our organizational structure to become a faster, leaner and more focused company.”

The disruption story that has driven Intuit stock down more than 60% from its 52-week high is almost entirely concentrated in one narrow pocket of the business: price-sensitive DIY tax filers earning under $50,000 per year, a segment Goodarzi explicitly called “12% of our total TurboTax TAM.”

Against that headwind, TurboTax Live customers grew 38% this fiscal year, new assisted customers grew 29%, and TurboTax Live now represents 53% of total TurboTax revenue. Global Business Solutions, which includes QuickBooks and constitutes roughly 40% of company revenue, grew 15% in the quarter or 17% excluding Mailchimp. Online Ecosystem revenue for QBO Advanced and Intuit Enterprise Suite grew 38%.

The assisted category is capturing exactly the dynamic Intuit has been building toward: customers who will spend far more on done-for-you financial intelligence than on software alone. As Goodarzi put it: “customers buy confidence, not code, which is why they spend at least 7x more on accounting and tax experts than on software alone.”

The income statement shows durable gross margin and improving operating leverage. Now the question is what that’s worth. Model the TIKR base case for Intuit stock yourself, for free →

Is Intuit Stock Undervalued? What the Operating Leverage Story Actually Shows

Intuit stock’s gross margin of 84% in Q3 fiscal 2026 held nearly flat compared to the 85% posted in the same tax-season quarter a year prior, a signal that cost of revenue is scaling in proportion to the business and pricing power on the high-ARPU products remains intact.

Operating margins of 47% in Q3 represent a significant improvement over the 2% operating margin Intuit stock posted in the non-tax Q1 of fiscal 2025, a reflection of how dramatically earnings concentrate around the April filing season.

The more instructive comparison is across the trailing eight quarters: operating margins ranged from 2% to 8% in the non-tax quarters and 47% to 48% in the peak tax periods, a pattern that is consistent rather than deteriorating.

Total operating expenses of $3.21 billion in Q3 included $2.20 billion in SG&A and $840 million in R&D, growing in absolute terms but consuming a smaller share of the $7.23 billion gross profit generated in the quarter.

The restructuring, which Goodarzi said would primarily flow to margin expansion rather than reinvestment, is designed to flatten the cost structure between peak and non-peak quarters and compress the gap between the 47% operating margin Intuit stock achieves in April and the single-digit margins it posts in the off-season.

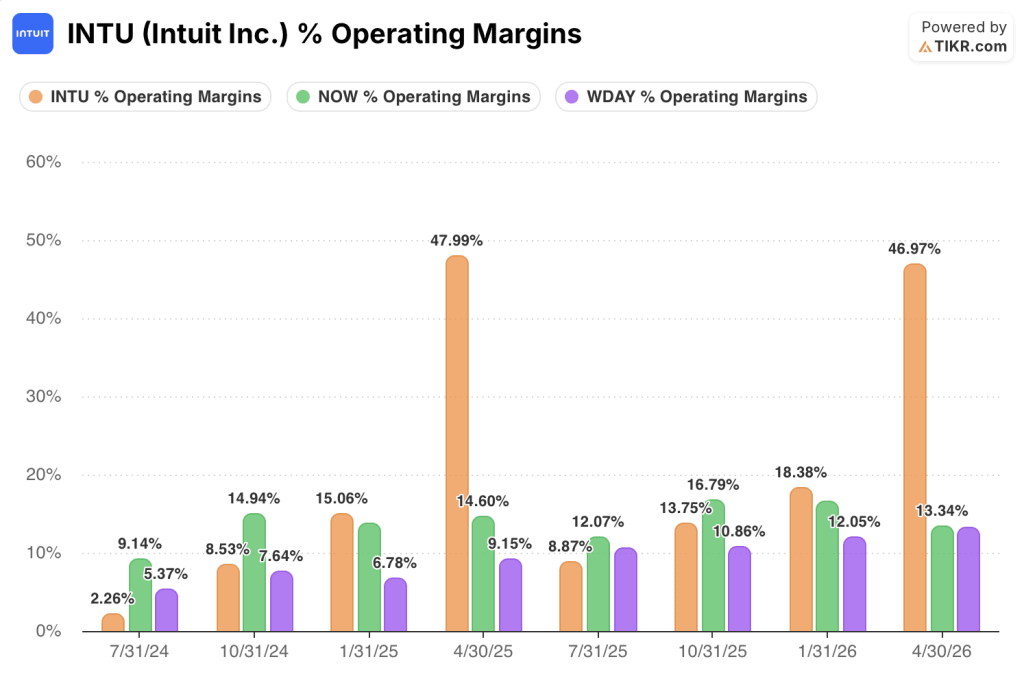

INTU Leads NOW and WDAY on Operating Margins, But the Off-Season Gap Is Where the Story Lives

Intuit stock’s 47% operating margin in the April 2026 tax-season quarter dwarfs both ServiceNow (NOW) at 13% and Workday (WDAY) at 13% in the same period, a gap that reflects the structural earnings concentration built into Intuit’s business model rather than a sustained operational advantage.

The more instructive comparison is in the non-peak quarters, where Intuit stock’s operating leverage case either proves out or falls apart against peers that carry consistent margins year-round: ServiceNow posted 14% to 17% operating margins across the trailing eight quarters with minimal seasonal variance, while Workday ranged from 7% to 13%, both patterns that reflect the steady subscription compounding model those platforms run.

Intuit stock’s non-tax quarters tell a different story: 2% operating margin in July 2024, 9% in October 2024, 15% in January 2025, then collapsing back to 9% in July 2025 before recovering to 14% in October 2025 and 18% in January 2026. The restructuring Goodarzi announced on the Q3 call is specifically targeted at compressing this trough: if the 17% workforce reduction flows primarily to the bottom line as management indicated, the off-season floor should rise meaningfully, narrowing the structural gap to ServiceNow’s consistency without sacrificing the peak-quarter spike that no subscription peer can match.

TIKR’s $469 Target on Intuit Stock: What Has to Hold for the Return to Materialize

TIKR’s base case values Intuit stock at approximately $469 by July 2030, implying around 65% total return from the current price of $284, or roughly 13% annualized over approximately 4 years.

The mid-case assumes revenue growing at around 10% annually, net income margins expanding toward roughly 32%, and the P/E multiple compressing modestly from current levels. If assisted tax continues scaling at 30%-plus and Global Business Solutions holds its mid-to-high-teens growth rate, those assumptions look achievable on the trajectory shown in the Q3 income statement.

If the DIY restructuring stalls or AI disruption spreads from the price-sensitive segment into higher ARPU filers, the bear case of around $526 still implies around 85% total return, or roughly 8% annualized, suggesting meaningful downside protection even in a worse outcome.

The high case of around $867 by July 2030 depends on net income margins approaching 34% and EPS compounding near 13% annually, a path that requires the August platform relaunch to drive genuine consumption-based monetization in the mid-market.

Why does Intuit stock’s operating margin spike in April?

The quarter ending April 30 captures the bulk of TurboTax revenue, which concentrates between January and the April 15 filing deadline.

That revenue floods in against a relatively fixed cost base, pushing operating margins to 48% in April 2025 and 47% in April 2026.

The other three quarters carry the full SG&A and R&D load with only a fraction of the revenue, collapsing margins to single digits in July before recovering through the fall.

The 17% workforce reduction is specifically designed to raise that off-season floor.

Is Intuit stock a buy right now?

Intuit stock trades near a 52-week low after falling more than 60% from its July 2025 high, creating a significant gap between the current price of $284 and TIKR’s mid-case target of approximately $469. The income statement shows durable 84% gross margins and 47% operating margins in the peak tax quarter. Whether that justifies buying depends on how quickly the restructuring savings flow to the bottom line and whether the assisted tax momentum holds.

Should You Invest in Intuit Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intuit Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intuit Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze INTU stock on TIKR for Free →