Key Takeaways for Copart Stock

- Revenue grew 2% year-over-year to $1.24 billion in Q3 FY2026, beating the Street estimate of $1.20 billion.

- Gross margins expanded 71 basis points to 46%, while operating income grew 3% to $464.3 million at a 37% operating margin.

- U.S. insurance average selling prices hit a seasonally adjusted all-time record high for the quarter, rising 4% year-over-year despite a 4% unit volume decline.

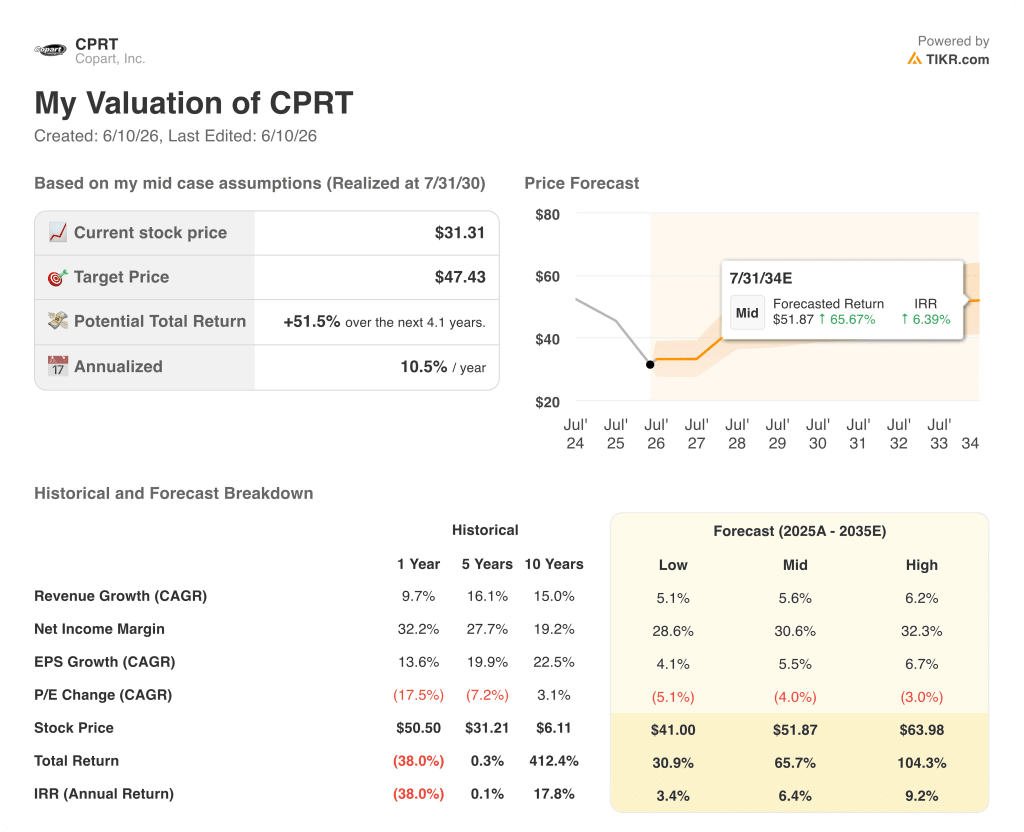

- TIKR’s mid-case values Copart stock at approximately $52 by July 2030, implying around 66% total return from the current price of $31.

Copart Stock Beats Q3 Estimates Even as U.S. Insurance Volumes Fall 4%

Copart (CPRT), the world’s largest online salvage vehicle auctioneer, reported Q3 fiscal 2026 revenue of $1.24 billion on May 21, beating the Street estimate of $1.20 billion, even as U.S. insurance unit volumes declined 4% year-over-year.

The headline number obscures what actually happened at the auction level.

Global average selling prices rose 5% year-over-year, absorbing the unit shortfall entirely and then some.

U.S. insurance average selling prices rose 4% year-over-year, reaching, as CEO Jeff Liaw stated on the Q3 call, “a seasonally adjusted all-time record high for Copart insurance ASPs in the third quarter.”

That record landed against a backdrop of softening claims activity, with consumers pulling back on insurance coverage in response to rising premiums. Earned car years, per ISS Fast Track data cited on the call, declined 4% year-over-year in Q4 calendar 2025, even as vehicles in operation grew 1%.

The company’s international segment offered a sharper contrast. International units grew 6% in the quarter, with insurance units up 5% and noninsurance units growing 11%. International revenue rose 14% to $234.2 million, with service revenues up 18% driven by a 10% increase in fee revenue per unit.

The buyer network doing the heavy lifting spans more than 160 countries, and international buyers now represent more than a third of volume sold at U.S. Copart auctions and nearly half of auction proceeds. When certain Middle Eastern corridors softened due to global conflict, Liaw noted that demand from Central Europe, West Africa, Central America, and the Caribbean filled the gap.

Total loss frequency reached 23.6% in Q1 calendar 2026, up nearly 5 full percentage points over the past four years. Copart views driving that number higher as a core competitive responsibility, not a passive tailwind.

Copart Stock’s Gross Margin Holds at 46% While the Company Builds Into the Weakness

Copart stock’s gross profit grew 4% year-over-year to $572.6 million in Q3 FY2026, with gross margins expanding 71 basis points to 46%.

That expansion happened alongside the launch of domestic long-haul delivery services, a new product that added approximately $15 million in facility operations costs during the quarter but is generating margin at the revenue line.

The gap between gross margin performance and operating margin performance tells a more complete story: with gross margins at 46% and operating margins at 37%, Copart stock is running one of the tightest SG&A structures in the commercial services sector, with selling, general, and administrative expenses holding at $110 million for the quarter, flat against the prior two periods.

Operating income grew 3% to $464.3 million, with operating margins expanding from 37% in the prior-year quarter to 37% in Q3 FY2026, consistent with the 37% reading from Q2 FY2026.

The income statement over the past eight quarters shows something more instructive than any single period: gross margins have moved from 43% in Q1 FY2024 to 46% in Q3 FY2026, a steady structural climb that has held even as unit volumes softened, which indicates that pricing power and mix improvement, not volume leverage, are doing the work.

Copart Stock’s 46% Gross Margin Leads RBA by a Narrowing Gap and Laps Carvana Entirely

Copart stock’s gross margin of 46% in Q3 FY2026 (period ending 4/30/26) sits roughly in line with RB Global’s (RBA) 46%, a gap that has compressed from nearly 5 percentage points in Q1 FY2024 (7/31/24) when CPRT ran 43% against RBA’s 48%.

That convergence is directionally significant: RBA (Ritchie Bros. Auctioneers), the heavy equipment and commercial vehicle auctioneer, has historically carried a gross margin premium over Copart reflecting its higher-fee consignment model, but the two businesses are now operating at near-parity on this metric, with Copart at 46% and RBA at 46% in the most recent quarter.

Meanwhile, Carvana (CVNA), the used vehicle e-commerce platform, operates in an entirely different margin band, posting 20% gross margin in the same period, a structural reflection of the inventory-heavy model it runs versus the asset-light marketplace economics that produce Copart and RBA stock’s 46%.

Is Copart Stock Undervalued in 2026? TIKR’s $52 Model Makes the Case

TIKR’s base case values Copart stock at approximately $52 by July 2030, implying around 66% total return from the current price of $31, or roughly 6% annualized over approximately 4 years.

If insurance volume recovery accelerates and gross margins sustain above 46%, the TIKR high case reaches approximately $64, representing around 104% total return, or roughly 9% annualized.

If volume headwinds persist longer than the historical cyclical pattern would suggest and revenue growth tracks the low-case assumption, the TIKR model produces approximately $41, still representing around 31% total return from today’s price, or roughly 3% annualized.

Every scenario in the model produces a positive outcome from the current price of $31.

Is Copart Stock a Buy Right Now?

Copart stock has declined roughly 38% from its 52-week high of $51 while the income statement has continued to compound: gross margins at 46%, operating income growing 3% year-over-year to $464.3 million, and U.S. insurance ASPs at an all-time seasonal record.

TIKR’s mid-case target of approximately $52 implies around 66% total return.

The risk is the pace of insurance volume recovery, which management describes as cyclical rather than structural.

If that assessment is correct, Copart stock is priced well below its forward earnings power.

Should You Invest in Copart, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Copart, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Copart, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CPRT stock on TIKR for Free →