Key Stats for Honeywell Stock

- Current Price: $214.87

- Target Price (Mid): ~$321

- Street Target: ~$248

- Potential Total Return: ~52%

- Annualized IRR: ~10% / year

- Earnings Reaction: (0.55%) on 4/23/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What the Market Is Waiting For

Honeywell International Inc. (HON) has climbed roughly 10% year to date, rising from $195.09 at the end of 2025 to around $215 today. The stock still sits about 13% below its 52-week high of $248.18.

That gap reflects a real uncertainty. On June 29, Honeywell will complete the spin-off of its Aerospace division as an independent Nasdaq-listed company (ticker: HONA), with existing shareholders receiving one HONA share for every two HON shares held. What remains will operate as Honeywell Technologies, a focused industrial automation and building technology business that has never traded as a standalone entity. Until now, nobody has had a clean set of numbers for it.

CFO Mike Stepniak’s June 8 guidance call changed that. RBC Capital and Goldman Sachs both raised their price targets in response, with RBC going to $275 and Goldman to $276, each citing the transformation’s potential to unlock shareholder value through pure-play re-rating.

A Blueprint for a New Company

The June 8 call introduced the first standalone financial framework for Honeywell Technologies. For the full year 2026, the company is guiding to 2% to 3% organic sales growth, segment margin expansion of 220 to 270 basis points, adjusted EPS of $4.05 at the midpoint (up 22% to 28% year over year), and free cash flow of roughly $2 billion, with the majority expected in the second half.

The EPS growth looks dramatic, but it is largely structural, not organic. It reflects removing Aerospace, stripping out pension income, and eliminating Quantinuum’s losses from the P&L. The margins tell a more meaningful story.

Honeywell Technologies is expected to exit 2026 at roughly 22% segment margin in Q4, up significantly from the first half. The driver is a cost elimination. When Aerospace departs on June 29, it leaves behind roughly $290 million in shared overhead. Stepniak confirmed that 75% of that is already actioned: the people are gone, the restructuring programs are done. The remainder is targeted for the first half of 2027. “I am 100% confident we’ll be able to eliminate that stranded cost and then some,” he said on the call. In the meantime, operationally the business is already expanding margins by 100 to 120 basis points, ahead of the original 50 to 90 basis point guidance.

Adding to the cleanup: Honeywell’s quantum computing subsidiary, Quantinuum, completed its IPO on June 4, raising $1.68 billion at $60 per share. Removing Quantinuum’s consolidated losses from Honeywell Technologies’ results improves segment profit by roughly $300 million, a drag that had been masking the core automation business’s true profitability.

See historical and forward estimates for Honeywell stock (It’s free!) >>>

Three Segments, One H2 Acceleration

Honeywell Technologies will operate three segments after the spin-off. All three are showing momentum heading into the second half, with May orders running high single digits across the company and Building Automation approaching double digits.

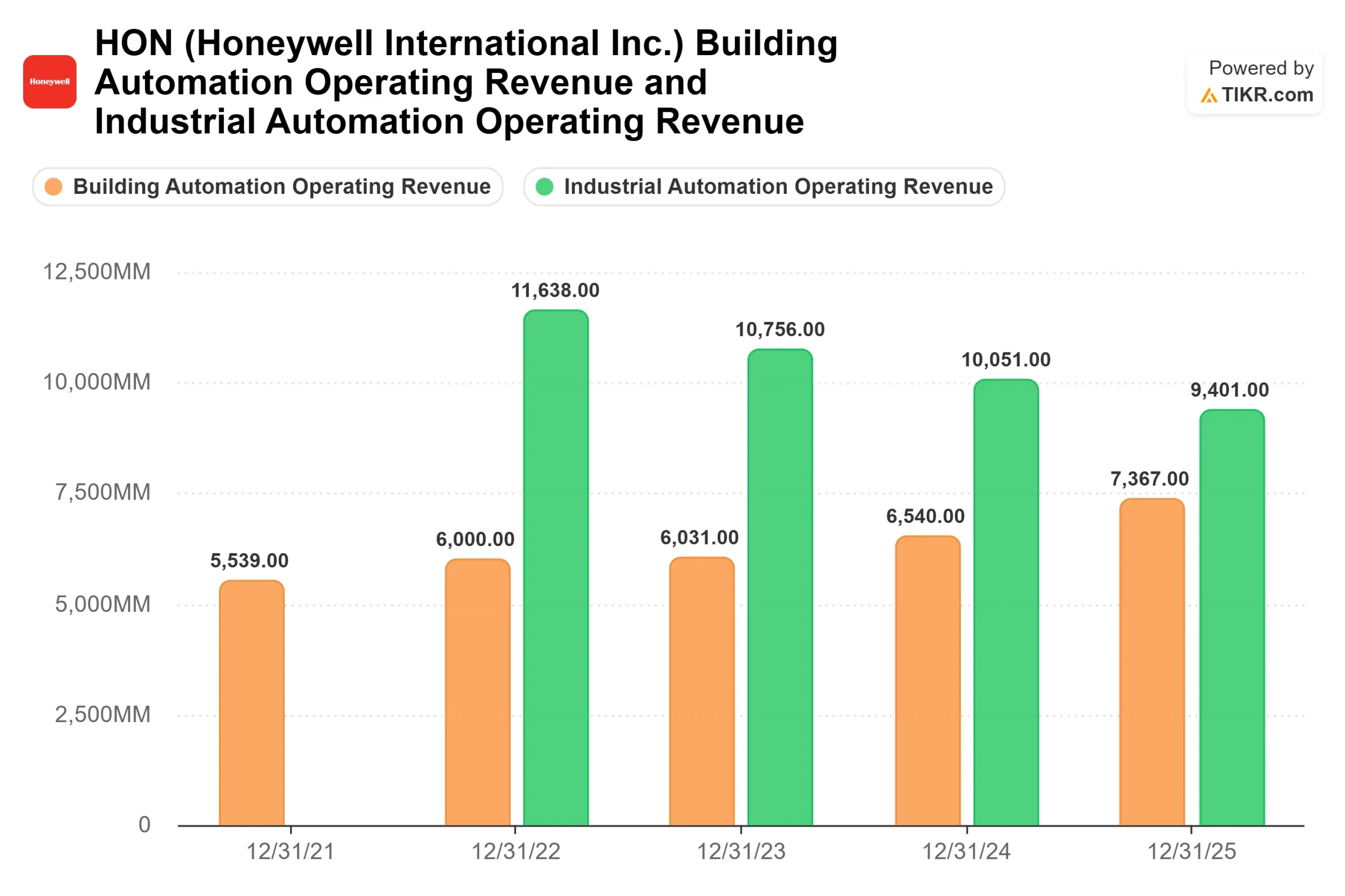

Building Automation sells building management systems, fire and security products, and its Forge connected-building software platform. It has delivered seven consecutive quarters of high single-digit organic growth, and according to Stepniak, order strength is at levels he hasn’t seen in his six years at the company. Revenue has grown steadily from $6,031 million in 2023 to $6,540 million in 2024 to $7,367 million in 2025.

Process Automation and Technology, or PA&T, serves LNG, refinery, and petrochemical customers. It carries a record backlog that is beginning to convert, with customer advance payments received and field teams mobilized. Catalyst demand used by refiners to improve yields is expected to see a double-digit step-up in the second half as crack spreads improve. That conversion is the key driver of the 3% to 5% organic growth guided for H2, up from the full-year pace of 2% to 3%.

Industrial Automation, which sells sensing, measurement, and control products, was originally guided to decline. It has since been upgraded to flat organic growth for the year, with Europe and China recovering faster than expected. Stepniak described the business as a self-help story a simplified, pure-play measurement and sensing operation with improving pricing power and supply chain execution.

See how Honeywell performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $214.87

- Target Price (Mid): ~$321

- Potential Total Return: ~52%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Honeywell stock (It’s free!) >>>

The TIKR mid-case model projects a revenue compound annual growth rate of around 6% through 2030, with a net income margin of around 18%, arriving at a mid-case target of ~$321 per share. That implies roughly 52% total return from current levels, or about 10% annualized.

The two revenue growth drivers are Building Automation’s structural share gains in a software-driven building management cycle and PA&T’s backlog conversion as global LNG project activity accelerates. The margin driver is stranded cost elimination, paired with pricing expected in the 3.5% to 4.5% range through year-end management’s guidance, confirmed on the June 8 call, more than offsetting input inflation.

The primary risk is PA&T execution. If the project backlog converts more slowly than management projects, or catalyst demand softens again, the second-half revenue ramp embedded in guidance doesn’t materialize. That puts free cash flow at risk and likely pulls the stock toward the low $200s.

The upside case is a clean 2027 with the $85 million residual stranded cost drag fully gone, Building Automation sustaining its growth streak, and the market re-rating HON as a pure-play automation company rather than a blended industrial conglomerate. The Street’s mean target of ~$248 suggests that re-rating has already begun. The TIKR model suggests it has further to run.

Conclusion

Honeywell Technologies will be a new stock on June 29. The near-term number that matters most is not EPS, which will be distorted by spin-off accounting for at least two quarters, but Q3 2026 segment margin. Stepniak guided to roughly 21% in Q3 and roughly 22% in Q4. If Q3 lands at or above 21% and PA&T conversion is on track, the stranded cost story is real, and the second-half thesis holds. If Q3 comes in below 20.5%, the model has a problem.

Q3 earnings are expected in late October 2026. By then, the Aerospace noise is gone, and the automation margins will speak for themselves.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Honeywell?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Honeywell, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Honeywell alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Honeywell on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!