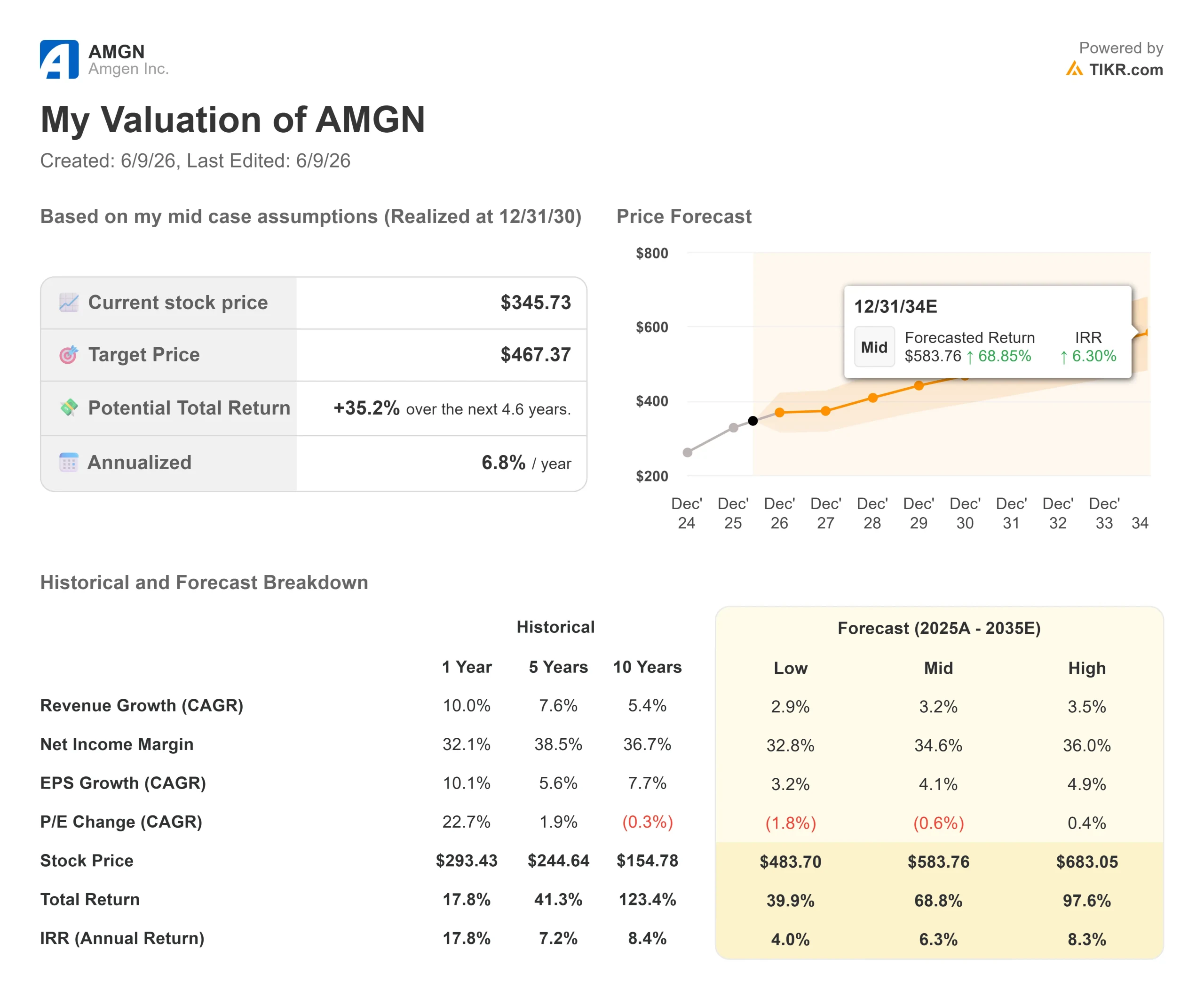

Key Stats for Amgen Stock

- Current Price: $346.95

- Target Price (Mid): ~$467

- Street Target: ~$352

- Potential Total Return: ~35%

- Annualized IRR: ~7% / year

- Q1 2026 Earnings Reaction: -4.75% (4/30/26)

- Max Drawdown: -16.57% (5/4/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The IRS Number That Isn’t What It Looks Like

Amgen Inc. (AMGN) walked into the Goldman Sachs 47th Annual Global Healthcare Conference on June 9 carrying one of the most misunderstood numbers in large-cap biotech. The IRS tax dispute sent the stock down 4.75% on April 30 after Q1 earnings, and pushed it to a max drawdown of 16.57% as of May 4. It has since become the single biggest weight on sentiment. But outgoing CFO Peter Griffith, executive vice president and chief financial officer, spent the opening minutes of the Goldman fireside chat doing something unusual: he walked through the actual math.

The proposed IRS adjustments for 2010 to 2015 include $2 billion in penalties Amgen believes are unwarranted, approximately $2 billion in calculation errors it disputes, up to $3.1 billion in repatriation taxes already paid (including roughly $1.85 billion paid in 2025), and $1.9 billion in cash deposits already made to the IRS. Griffith argued that any extrapolation to later years must also account for a different post-2018 tax framework and lower tax rates. The headline exposure the market absorbed in late April, he said, does not translate directly into incremental cash.

The tax court ruling on the 2010 to 2015 period is expected no earlier than the second half of 2026. Griffith noted the trial ran from November 2024 to January 2025, and put the decision roughly two years out from that window.

The risk is real, though. Amgen itself acknowledged on its Q1 2026 earnings call that a sustained ruling could have a material impact on its financial statements. Griffith’s Goldman Sachs remarks are the company’s most detailed public pushback to date, but investors will need the ruling itself to settle the question.

This is also among Griffith’s final major investor appearances. Amgen announced on May 19, 2026, that it will retire effective August 31, with Thomas Dittrich, a former Amgen finance executive, most recently serving as CFO of Galderma, taking over on September 1. His on-the-record positioning here matters for how investors interpret the IRS risk through year-end.

See historical and forward estimates for Amgen stock (It’s free!) >>>

Six Drivers, 24% Growth, 70% of Sales

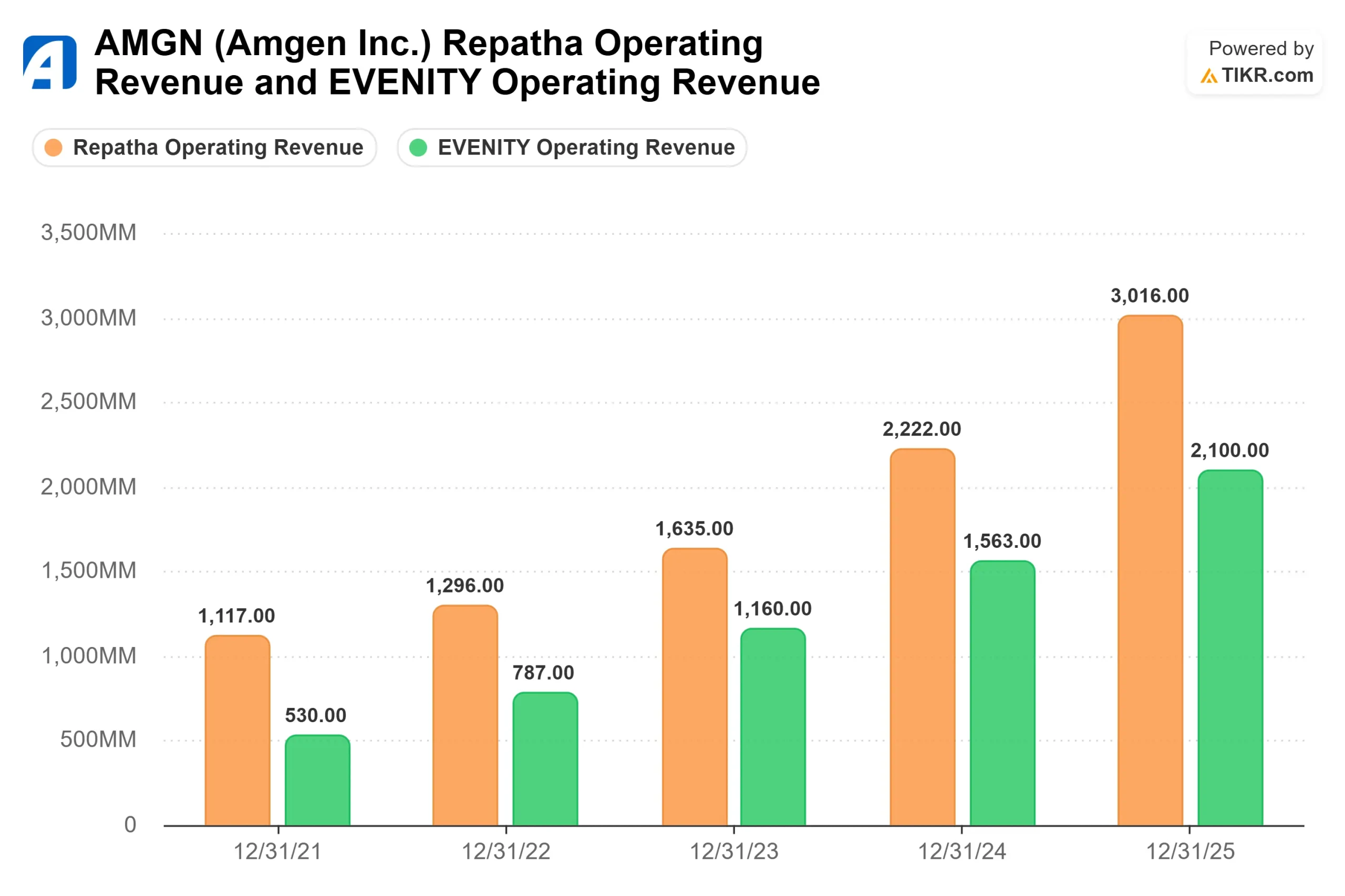

Griffith and commercial chief Murdo Gordon, executive vice president of Global Markets and Policy, described a business whose headline numbers understate the momentum. Six growth franchises, Repatha, EVENITY, TEZSPIRE, the oncology portfolio led by IMDYLLTRA (tarlatamab, a bispecific T cell engager that redirects immune T cells to attack cancer), the rare disease portfolio anchored by UPLIZNA, and biosimilars, together grew 24% year-over-year in Q1 2026 and represented approximately 70% of total product sales, per Amgen’s Q1 2026 earnings release.

Repatha (evolocumab), a PCSK9 inhibitor that lowers LDL cholesterol by blocking a protein that prevents the liver from clearing it, generated $876 million in Q1 2026 sales, up 34% year-over-year, per Amgen’s Q1 2026 earnings release. Gordon and Amgen’s commercial head cited more than 100 million people globally with elevated LDL. Management noted that updated ACC/AHA guidelines leave roughly 80% of high-risk patients, meaning approximately 4 in 5 still above their treatment goals, and PCSK9 inhibitors have reached less than 10% of the eligible U.S. population. The commercial message was unambiguous: that momentum “is durable and will sustain through the end of the decade.” Per TIKR’s annual segments data, Repatha revenue has grown from $1,117 million in 2021 to $3,016 million in 2025.

IMDYLLTRA (tarlatamab) has crossed the $1 billion annualized run rate and now reaches patients at more than 1,800 U.S. treatment sites, with more than half in community settings. The European Commission approved IMDYLLTRA for extensive-stage small cell lung cancer on June 1, opening an additional market. Amgen is initiating Phase III evaluation in limited-stage disease, where management believes the bispecific mechanism performs especially well at lower tumor burdens.

UPLIZNA (inebilizumab) received FDA approval as the first treatment for IgG4-related disease (IgG4-RD), a systemic inflammatory condition that frequently goes undiagnosed. Gordon described the launch as a market-creation exercise, citing an addressable U.S. population of 30,000 to 40,000 patients in IgG4-RD alone, on top of the established NMOSD (neuromyelitis optica spectrum disorder) base and the newly launched generalized myasthenia gravis indication. “The growth outlook for IgG4 is very strong. There’s large headroom there,” he said.

MariTide: The Optionality the Model Doesn’t Price In

MariTide (maridebart cafraglutide) is Amgen’s obesity drug candidate in Phase III under the MARITIME program. It works by blocking GIP receptor signaling while activating the GLP-1 pathway, suppressing appetite and reducing fat storage through two mechanisms simultaneously. Phase II data, published in the New England Journal of Medicine, showed up to 20% average weight loss at 52 weeks without a plateau.

Griffith confirmed Amgen will reach 12 Phase III programs in MariTide by year-end 2026, up from the current nine. Studies span chronic weight management, cardiovascular outcomes, heart failure, obstructive sleep apnea, a switch study for patients on weekly GLP-1 injections, and a long-term maintenance study. Gordon was direct on the commercial edge: the differentiation, potentially as few as four to six injections per year, has held up through all stages of development. “Nothing seems to compare to the differentiated profile that we’ve got,” he said.

The TIKR mid-case model does not include a MariTide revenue contribution within the 2030 forecast window. The ~$467 target reflects Amgen’s existing portfolio only. MariTide is optionality on top, and the current price does not appear to assign it meaningful value either way.

Olpasiran: A Binary Catalyst for 2027

Griffith also highlighted olpasiran, an investigational siRNA therapy, a molecule designed to silence a specific gene targeting Lp(a), or lipoprotein(a), a genetically determined cardiovascular risk factor that statins and PCSK9 inhibitors cannot meaningfully reduce. Approximately 7,200 patients are enrolled in a Phase III outcomes trial. Gordon cited Phase II data showing 95% to 100% Lp(a) reduction. Novartis’s competing drug, pelacarsen, is expected to report Phase III outcomes data in 2027. A positive pelacarsen readout would validate the Lp(a) hypothesis broadly. Gordon believes olpasiran’s deeper knockdown positions Amgen favorably regardless of which drug reports first.

See how Amgen performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $346.95

- Target Price (Mid): ~$467

- Potential Total Return: ~35%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for Amgen stock (It’s free!) >>>

This article uses TIKR’s mid-case assumptions: revenue CAGR of around 3% (mid-case input: 3.2%), with net income margins expanding toward around 35% (mid-case input: 34.6%). At the $345.73 model entry price, those inputs produce the ~$467 target.

The two revenue growth drivers are Repatha’s penetration of an underpenetrated PCSK9 market and UPLIZNA’s multi-indication ramp. The margin driver is operating leverage: Amgen guided to 45% to 46% non-GAAP operating margin for 2026, and free cash flow should improve as the post-Horizon debt load declines. LTM net debt is $45.3 billion; LTM Net Debt/EBITDA is 2.64x, projected to compress toward 1.6x by 2027 per TIKR estimates.

On valuation multiples, Amgen trades at 10.72x NTM EV/EBITDA below AbbVie at 13.48x and argenx at 24.13x per the TIKR Competitors screen. That discount reflects the IRS overhang more than any operational weakness.

The downside: an adverse tax court ruling that ignores the offsets Griffith described reopens the 2016 to 2022 period, compresses near-term free cash flow, and limits business development capacity. The upside: a manageable ruling removes the largest known drag and returns focus to a business where six growth drivers are already delivering 24% combined growth.

Conclusion

The tax court ruling from 2010 to 2015 is the event that defines Amgen’s second half of 2026. A ruling consistent with Amgen’s reserves removes the biggest discount to the mid-case and shifts investor focus back to full-year guidance of $37.1 billion to $38.5 billion in revenue, per Amgen’s Q1 2026 earnings release, Repatha’s NTB (new-to-brand) prescription trajectory, and UPLIZNA’s IgG4 launch metrics. A ruling that materially exceeds Griffith’s offset math puts pressure on the balance sheet and invites a second dispute over 2016 to 2022.

Watch for court scheduling updates between now and Q2 earnings. That is the signal the market has been waiting for since April 30.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amgen?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amgen, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amgen alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!