Key Stats for Tesla Stock

- 52-Week Range: $288.77 to $498.83

- Current Price: $396.68

- Street Mean Target: ~$420

- TIKR Target Price (Mid): ~$1,613

- TIKR Annualized IRR (Mid): ~35% per year

- Q1 2026 Revenue: $22.4B (up 16% year over year)

- Q1 2026 Non-GAAP EPS: $0.41 (up 52% year over year)

- Q1 2026 Gross Margin: 21.1% (up from 16.3% a year ago)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Gap Between What Tesla Reported and What the Stock Did

The tension inside Tesla’s (TSLA) 2026 story is not hard to identify. The automotive business is measurably better than it was a year ago, and the new businesses are producing real data for the first time. What the stock hasn’t done is resolve the bigger question: whether Robotaxi and Optimus will ultimately justify the valuation.

The Q1 2026 results were the clearest evidence yet that the automotive foundation has stabilized. Total revenue came in at $22.4 billion, up 16% year over year. Gross margin reached 21.1%, up nearly 500 basis points from a year ago, as lower material costs and a richer mix of FSD subscriptions and services revenue flowed through. Non-GAAP EPS of $0.41 grew 52% year over year.

Tesla’s Services segment, which includes insurance, charging, and software, generated $3.7 billion in revenue, up 42% year over year. That growth matters because service revenue carries structurally higher margins than vehicle sales and compounds with the size of the installed fleet rather than quarterly delivery volumes.

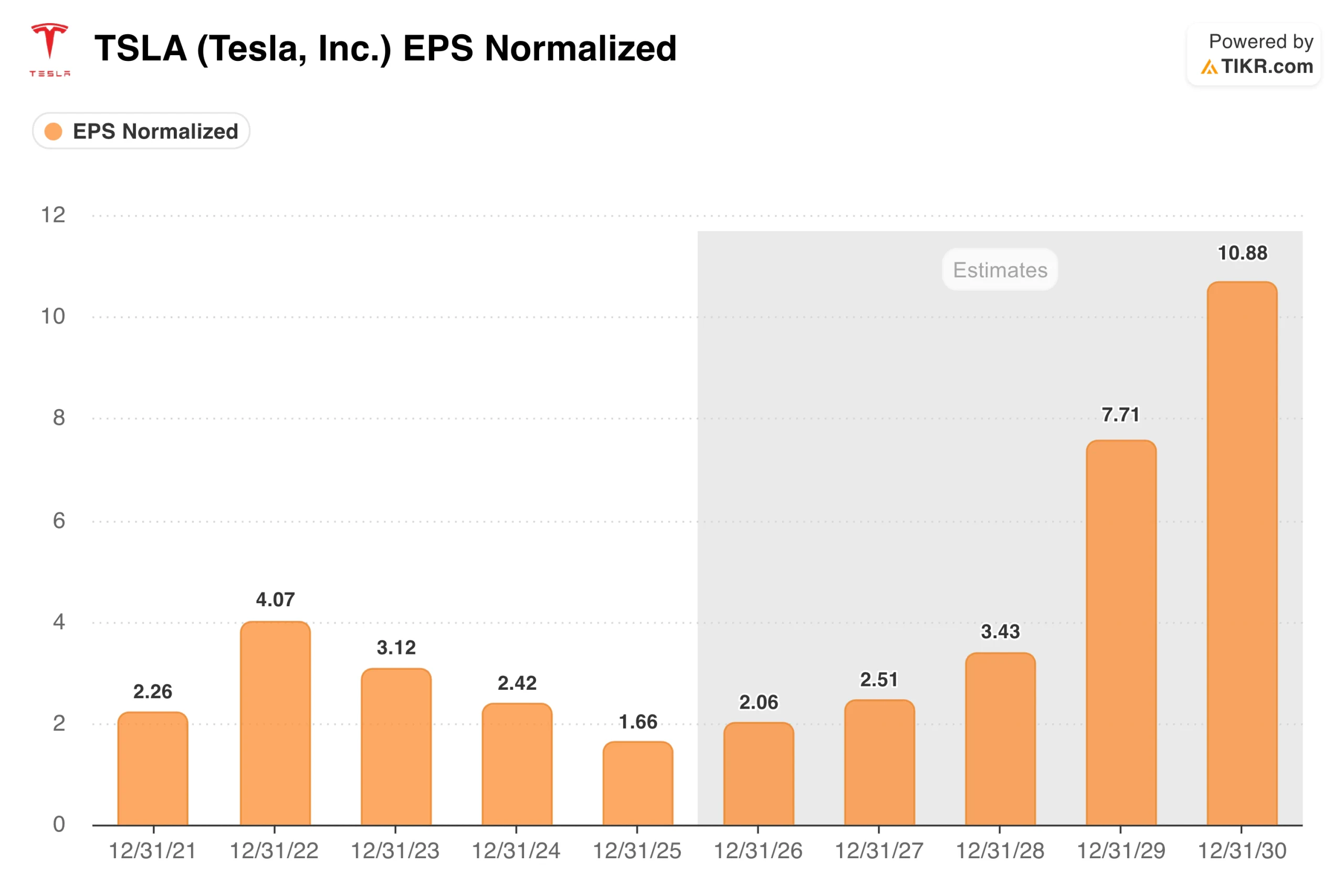

The EPS chart clearly captures the arc. Tesla peaked at $4.07 in 2022, declined to $1.66 in 2025, and is now entering what consensus expects to be a sustained recovery toward $2 in 2026, accelerating from there as autonomy and energy revenues scale. The 2025 trough looks, in retrospect, like the cost of building the next version of the business while running the current one.

See historical and forward estimates for Tesla stock (It’s free!) >>>

Robotaxi Miles Are Doubling, the Cybercab Is Next

The most consequential development in Q1 was not a financial metric, as Tesla launched unsupervised Robotaxi rides in Dallas and Houston in April, adding to its Austin footprint, which began generating paid miles in 2025. Cumulative paid Robotaxi miles nearly doubled sequentially in Q1, and expansion across Phoenix, Miami, Orlando, Tampa, and Las Vegas is underway as permitting progresses.

Management expects commercial Robotaxi rides to generate gross margins above 50% once fleets exceed 5,000 vehicles per metro. The Cybercab, now in pilot production at Gigafactory Texas, is designed for fleet deployment at a lower per-unit cost than the Model Y currently used in the service. Volume production is targeted for later this year.

Optimus is earlier in its arc, and site preparation for a large-scale factory in Fremont has begun, with a first-generation line targeting up to 1 million robots per year. Production targets for 2026 are in the thousands of units, scaling to tens of thousands in 2027.

Free cash flow declined from $7.6 billion in 2022 to a trough of $3.6 billion in 2024 as capex surged for new factories and AI infrastructure, then recovered to $6.2 billion in 2025.

Capital expenditures of $2.5 billion in Q1 2026 alone reflect continued heavy investment, but the operating cash flow of $3.9 billion covered it. The balance sheet shows $44.7 billion in cash and investments, which suggests the company is not running low on options.

See how Tesla performs against its peers in TIKR (It’s free!) >>>

What the TIKR Model Needs to Be True

TIKR’s valuation model targets $1,600 for Tesla stock, with a mid-case annualized return of roughly 35% through 2030. The model assumes revenue growth of around 21% annually, with net income margins expanding toward 23%, reflecting a mix shift toward software, services, and autonomy over time.

The wide gap between the current price and the TIKR target is not primarily a near-term earnings call. It reflects the assumed trajectory of businesses still in the early innings.

The key inputs to watch are Robotaxi ride volume and gross margin as Cybercab enters production, FSD subscription attach rates as the program moves to subscription-only, and Energy Storage deployments as the new Texas Megafactory comes online later this year.

What the Bulls Are Betting On

- Margin inflection is real and durable. The jump from 16.3% gross margin in Q1 2025 to 21.1% in Q1 2026 reflects lower material costs, higher FSD subscription revenue, and a richer services mix, all of which are structural improvements tied to fleet growth rather than one-time tailwinds.

- Robotaxi economics work at scale. Management’s 50%-plus gross margin target for commercial rides is credible if Cybercab production ramps on schedule. At that margin profile, even a modest fleet generates a meaningful EBITDA contribution by 2027 or 2028.

- Energy is a second business hiding in plain sight. The segment grew from $2.8 billion in annual revenue in 2021 to $12.8 billion in 2025, and the new Texas Megafactory is designed to significantly expand Megapack output in the years ahead.

- $44.7 billion in cash funds everything. Tesla can absorb heavy capex, fund semiconductor fabrication, and expand Robotaxi geography without needing to access capital markets.

What the Bears Are Watching

- The transition year is not over. Tesla is simultaneously ramping up Cybercab production, building Optimus factories, constructing a chip fab with SpaceX, and expanding Robotaxi operations. That level of parallel execution is ambitious, and the 2025 revenue decline is a reminder that the automotive business requires attention while the new ones are being built.

- The valuation requires near-perfect execution. A forward P/E near 190 times leaves limited room for a delayed Cybercab ramp, a regulatory setback in autonomy, or a demand slowdown in the automotive segment.

- Competition is accelerating on multiple fronts. Waymo has been operating fully unsupervised rides longer than Tesla and is expanding its own fleet. Chinese manufacturers continue to pressure automotive margins globally, particularly in markets where brand sentiment has been affected by news about Elon Musk.

See analysts’ growth forecasts and price targets for Tesla stock (It’s free!) >>>

Should You Invest in Tesla, Inc.?

The only way to think about Tesla is to hold two things at once. The automotive business has stabilized, margins are recovering, and the balance sheet is strong. At the same time, the current stock price is overwhelmingly a function of what Robotaxi and Optimus become over the next several years, and those outcomes are genuinely uncertain.

Put Tesla through TIKR, and you can see years of financial history, what Wall Street analysts expect for revenue and earnings in the quarters ahead, and whether current price levels are reflecting optimism or something more grounded. Just like Tesla, you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!