Key Takeaways for Delta Air Lines Stock

- Delta Air Lines stock posted total revenue of $15.85 billion in Q1 2026, up 13% year-over-year and a first-quarter record.

- Gross margins compressed from 17% in Q1 2025 to 15% in Q1 2026, as fuel costs outran record revenue growth.

- Operating income fell 11% year-over-year to $500 million, with operating margins dropping to 3% from 4% a year ago.

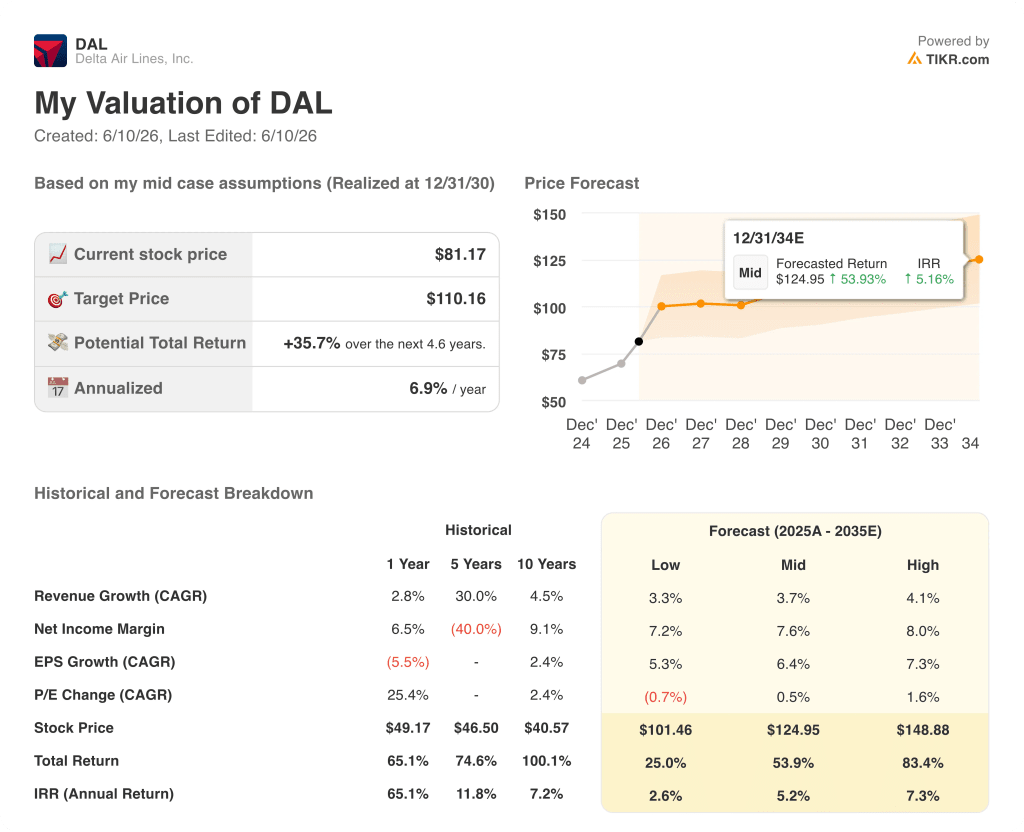

- TIKR’s mid-case values Delta Air Lines stock at approximately $125 by December 2030, implying around 54% total return from the current price of $81.

Access institutional-grade financials for Delta Air Lines stock before the rest of the market connects the dots. TIKR gives you the full income statement history, forward estimates, and valuation tools that turn data into conviction. Start analyzing DAL on TIKR for free →

Delta Air Lines Just Delivered Record Q1 Revenue While a $2 Billion Fuel Shock Rewrote the Rest of the Year

Delta Air Lines (DAL) walked into Q1 2026 with the strongest revenue quarter in its history and walked out with a full-year earnings debate dominated by a Middle East conflict that sent jet fuel to roughly double what the airline was paying a year ago.

Total revenue of $15.85 billion topped analyst estimates by more than $980 million, a margin of beat that is unusual for a company this size.

The number behind the quarter’s headline was not the revenue beat but the trajectory of demand underneath it: corporate sales grew double digits and set a quarterly record, and diverse revenue streams, which DAL defines as premium cabins, loyalty, the American Express partnership, and third-party aircraft maintenance, represented 62% of total revenue.

On the American Express relationship, CFO Dan Janki disclosed that remuneration grew 10% to over $2 billion in the quarter, led by 12% card spend growth, a data point that separates Delta Air Lines stock from the pure-play airline narrative that the market sometimes assigns to it.

CEO Ed Bastian was direct in Q1 earnings call about what fuel means for the year ahead: “The war in the Middle East has driven an unprecedented spike in jet fuel with prices roughly double what they were earlier in the year.”

DAL’s refinery, which directly supplies a portion of its fuel needs, provides a partial hedge: the Q1 average of $2.62 per gallon included a $0.06 benefit from that asset, and the Q2 fuel assumption of approximately $4.30 per gallon embeds an estimated $300 million refinery benefit.

The June quarter outlook calls for low-teens total revenue growth on flat capacity, with an operating margin of 6% to 8%, recapturing 40% to 50% of what Janki described as “more than $2 billion of additional fuel expense in the quarter.”

MRO (Maintenance, Repair, and Overhaul), Delta’s third-party aircraft servicing business, was a second-quarter story within the quarter: revenue more than doubled over the prior year to $380 million on heavy work scope execution, with a full-year outlook of $1.2 billion, representing nearly 50% growth versus 2025.

Fuel is masking what the underlying demand picture is telling Delta Air Lines stock. Pull the income statement on TIKR and see how the margin structure has moved through each quarter, so you can separate the transient cost shock from the durable revenue story. Build your DAL analysis on TIKR for free →

Delta Air Lines Stock’s Gross Margin Is the Number the Fuel Headline Is Hiding

Delta Air Lines stock’s gross margin in Q1 2026 fell to 15%, down from 17% in Q1 2025, as cost of goods sold rose to $13.46 billion against revenue of $15.85 billion.

The compression matters not because it is unprecedented but because it reverses a pattern that had been building: gross margins were 24% in Q2 2024, softened through the back half of that year, recovered to 24% in Q2 2025, and have now traced a second downward arc driven entirely by fuel.

Delta Air Lines stock’s operating margin tells the same story with more severity: at 3% in Q1 2026, it compares to 4% in Q1 2025 and 12% just two quarters earlier in Q2 2025, a span that captures exactly how exposed the income statement is to fuel timing.

The gap between gross margin and operating margin, which reflects SG&A, depreciation, and other operating expenses totaling $1.89 billion in Q1 2026, held roughly stable on a dollar basis, meaning the margin compression is concentrated at the gross profit line rather than in overhead growth.

Operating income of $500 million fell 11% year-over-year from $570 million in Q1 2025, on revenue that grew 13% in the same period: revenue growing at more than 13 times the pace of operating income compression is the arithmetic of a cost shock, not a structural deterioration.

DAL Trails United on Gross Margin by 15 Points, and the Gap Is Getting Wider

Delta Air Lines stock’s gross margin of 15% in Q1 2026 sits at the bottom of its peer group, trailing United Airlines (UAL) at 31%, Southwest Airlines (LUV) at 23%, and American Airlines (AAL) at 20% in the same period.

The gap between DAL and UAL has widened materially over the past eight quarters: in Q2 2024, Delta Air Lines stock carried a 25% gross margin against United’s 37%, a 12-point deficit that has now stretched to 15 points, meaning Delta’s relative cost position at the gross profit line has deteriorated even as its revenue premium over peers has held.

The competitive implication for the thesis is specific: if the Q1 2026 margin compression is fuel-driven and temporary, as the income statement’s stable overhead base suggests, then Delta Air Lines stock’s gross margin should recover toward the mid-20s when fuel normalizes, closing the gap with Southwest and narrowing it against United to something closer to the historical range.

What the peer chart does not show is a structural disadvantage at the revenue line. Delta’s unit revenue premium is well-documented. What it does show is that DAL’s cost of goods sold, dominated by jet fuel, is currently running hotter than any peer on a relative basis, which is the single condition the bull case requires to reverse.

Is Delta Air Lines Stock Undervalued in 2026? TIKR’s $110 Model Says Yes, With One Condition

TIKR’s base case values Delta Air Lines at approximately $110 by December 2030, implying around 36% total return from the current price of $81, or roughly 7% annualized over 4.6 years.

If fuel moderates and Delta delivers on its guidance of 6% to 8% operating margins in Q2, the income statement recovery is underway and the stock’s current level captures only a fraction of the earnings power the company has already demonstrated, with the high case targeting approximately $149 and roughly 83% total return, or around 7% annualized.

If fuel stays elevated for longer and margin recapture stalls, the low case of approximately $101 still implies around 25% total return over the period, a floor grounded in the structural diversification of the revenue base rather than in a cyclical bet on oil prices.

The condition that makes or breaks every scenario is the same one Bastian named on the call: whether elevated fuel becomes the catalyst for industry rationalization, compressing capacity from weaker carriers and allowing Delta Air Lines stock to recapture pricing and margin at an accelerated rate.

The income statement shows the mechanism clearly. Now see how TIKR’s model translates the margin recovery assumption into a price target and IRR under three scenarios. Run the DAL valuation model on TIKR for free →

Is Delta Air Lines stock a buy right now?

Delta Air Lines stock trades at $81 with TIKR’s mid-case placing fair value at approximately $110 by December 2030, implying around 36% total return.

The income statement shows gross margins compressed to 15% in Q1 2026 from 17% a year ago, driven by a fuel cost spike, not a demand problem.

Corporate sales set a quarterly record and diverse revenue streams representing 62% of total revenue give the stock a floor that pure-play carrier comparisons miss.

What did Delta say about fuel costs and guidance for 2026?

Delta guided Q2 2026 operating margins of 6% to 8% on flat capacity, with a fuel assumption of approximately $4.30 per gallon and an estimated $300 million refinery benefit.

CEO Ed Bastian said the company expects to recapture 40% to 50% of the more than $2 billion fuel headwind in Q2, and stated that full-year guidance remains on hold pending greater visibility into where fuel prices settle.

The MRO business, on track for $1.2 billion in 2026 revenue, adds a non-fuel, non-ticket revenue stream that partially insulates margins from further energy shocks.

Should You Invest in Delta Air Lines, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Delta Air Lines stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Delta Air Lines stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DAL stock on TIKR for Free →