Key Takeaways for Atlassian Stock

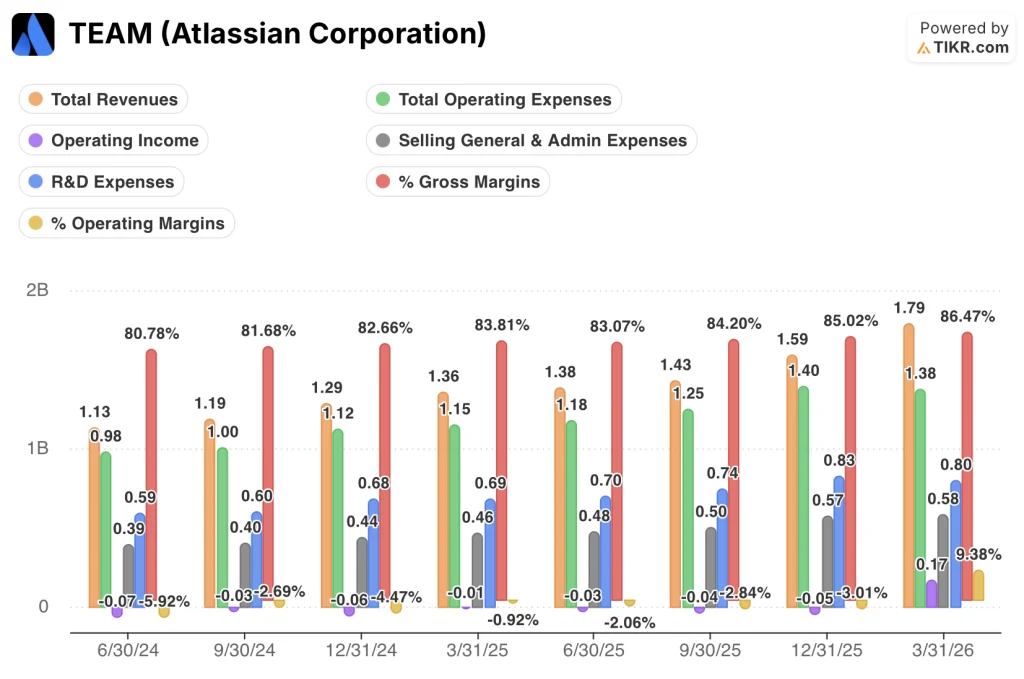

- Total revenue grew 32% year-over-year to $1.79 billion in Q3 FY2026, beating the analyst consensus of $1.70 billion by roughly $89 million.

- Gross margins expanded from 83% in Q3 FY2025 to 87% in Q3 FY2026, while GAAP operating income turned positive at $170 million for the first time in at least eight quarters.

- JSM’s Service Collection crossed $1 billion in ARR, growing 30% year-over-year, while Rovo AI credit usage is growing more than 20% month-over-month.

- TIKR’s mid-case values Atlassian stock at approximately $192 by June 2030, implying around 110% total return from the current price of $92.

Atlassian Stock Posts 32% Revenue Growth and Its First GAAP Operating Profit in Years

Atlassian Corporation (TEAM) builds the enterprise collaboration platform that connects how organizations plan, ship, and govern work across teams, and its fiscal Q3 2026 print delivered the kind of result that forces a reassessment of a thesis that had driven the stock down more than 57% from its 52-week high of $223.

Total revenue reached $1.79 billion in the quarter ended March 31, 2026, growing 32% year-over-year and beating the $1.70 billion analyst consensus by roughly $89 million.

The beat came from two places: cloud and data center.

Cloud revenue crossed $1.1 billion and accelerated to 29% growth year-over-year, as CEO Mike Cannon-Brookes noted in Q3 earnings call that “customers using Rovo are also growing their ARR at roughly 2x the rate of customers who are not using Rovo,” with Rovo AI credit usage growing more than 20% month-over-month.

The data center line added approximately $50 million in upfront term license revenue beyond expectations, as large enterprise customers with complex migrations pulled forward expansion activity ahead of data center’s March 2029 end-of-life date.

Net revenue retention remained north of 120% on the cloud side for what CFO James Chuong described as the third or fourth consecutive quarter of sequential improvement, and RPO grew 37% year-over-year to roughly $4 billion.

The Service Collection, Atlassian’s ITSM-focused bundle that includes Jira Service Management (JSM), crossed $1 billion in ARR and is growing 30% year-over-year, a milestone the company called its largest-ever quarter for competitive displacements from a major ITSM provider.

The Teamwork Collection, the bundle that grants customers 10x more Rovo AI credits, continues to show momentum: customers in Teamwork Collection are using AI credits at twice the rate and deploying twice as many agents as those outside it.

At the Bank of America 2026 Global Technology Conference, Chuong also framed the investment case directly: “The $1 million cohort of customers has grown 6x over the last 4 years, growing at 39% year-over-year. The customer cohorts of $3 million plus, that’s grown 10x over that same time frame, and that’s growing roughly 54% year-over-year.”

Atlassian Stock’s Gross Margin Inflection Is the Story the Income Statement Is Telling

Atlassian stock’s gross margin has moved from 81% in Q1 FY2025 to 87% in Q3 FY2026, an expansion of roughly 6 percentage points across seven consecutive quarters without a single reversal.

That trajectory matters because cost of goods sold held essentially flat at $240 million across five of the last eight quarters, while total revenues expanded from $1.13 billion to $1.79 billion, meaning Atlassian is delivering significantly more revenue for nearly the same platform delivery cost.

The operating leverage story is equally clear: total operating expenses actually declined quarter-over-quarter in Q3 FY2026, dropping from $1.40 billion in Q2 to $1.38 billion, even as revenue grew 13% sequentially from $1.59 billion to $1.79 billion.

That cost discipline, combined with gross profit growing 36% year-over-year to $1.55 billion, produced the quarter’s most significant income statement development: GAAP operating income turned positive at $170 million, versus an operating loss in every prior quarter shown in the dataset, producing a GAAP operating margin of 9% against seven consecutive quarters of negative figures.

The gap between gross margin and operating margin remains wide, with SG&A at $580 million and R&D at $800 million in Q3 FY2026, but both categories declined or held flat quarter-over-quarter, confirming that the margin inflection is structural rather than episodic.

Atlassian Stock Leads Salesforce and ServiceNow on Gross Margin and the Gap Is Growing

Atlassian stock’s gross margin reached 86% in Q3 FY2026, compared to 77% for Salesforce (CRM) and 75% for ServiceNow (NOW) in the same period, a spread of roughly 9 and 11 percentage points respectively against two of enterprise software’s most widely held names.

That gap has widened materially over the past eight quarters. In Q1 FY2025 (ended June 2024), Atlassian stock’s gross margin stood at 81% against Salesforce’s 77% and ServiceNow’s 77%, a spread of roughly 4 points in each direction. By Q3 FY2026, Atlassian stock had expanded to 86% while both peers compressed slightly, with Salesforce declining to 77% and ServiceNow to 75%, meaning the competitive distance on this metric roughly doubled across two years.

The implication for the investment thesis is direct: Atlassian’s platform cost structure is not just competitive, it is diverging favorably from two larger, more mature enterprise software businesses at precisely the moment its revenue base is accelerating to 32% year-over-year growth.

Is Atlassian Stock Undervalued in 2026? TIKR’s $146 Near-Term Target and $192 Mid-Case Say Yes

TIKR’s base case values Atlassian stock at approximately $146 by the near term and around $192 by June 2030, implying roughly 110% total return from the current price of $92, or approximately 10% annualized over the next 4.1 years.

If Atlassian executes on the mid-case trajectory, with revenue compounding at roughly 15% annually and net income margins expanding toward 25%, the stock reaches around $192 by June 2030, delivering roughly 10% annualized returns.

The bull case, requiring roughly 17% revenue growth and margins approaching 26%, produces a stock price of approximately $266 and around 14% annualized returns over the same period.

The bear case, modeling roughly 14% growth and margins near 23%, still reaches approximately $135 per share, implying around 5% annually, with the downside anchored by a business already demonstrating positive GAAP operating income and gross margins above 86%.

Is Atlassian stock a buy right now?

Atlassian stock trades at $92, more than 58% below its 52-week high of $223 and more than 37% below the average Wall Street analyst price target.

The Q3 FY2026 income statement shows gross margins at 87%, the highest level in the dataset, and GAAP operating income turned positive at $170 million for the first time in at least eight quarters.

Whether that inflection justifies the current price depends on assumptions for the pace of cloud migration and the stickiness of enterprise seat expansion, both of which showed positive signals in the quarter.

What is the Atlassian stock forecast for 2026 and beyond?

TIKR’s mid-case values Atlassian stock at approximately $192 by June 2030, implying around 110% total return from the current price of $92 and roughly 10% annualized.

The model assumes roughly 15% annual revenue growth and net income margins expanding toward 25%.

The bull case reaches approximately $266, and even the bear case, modeling roughly 14% growth, reaches approximately $135 per share, anchored by a business already generating positive GAAP operating income and gross margins above 86%.

Should You Invest in Atlassian Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Atlassian Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Atlassian Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TEAM stock on TIKR for Free →