Key Stats for QUALCOMM Stock

- Today’s Performance: -7%

- 52-Week Range: $122 to $260

- Valuation Model Target Price: around $200

- Implied Upside: about 3%

Analyze your favorite stocks like QUALCOMM Incorporated with TIKR (It’s free) >>>

What Happened?

QUALCOMM Incorporated stock fell about 7% today, recently trading near $191 per share as investors pulled back from semiconductor stocks and questioned how much AI optimism was already reflected in chip valuations. The move was sharp, with shares trading as low as $190 during the session after opening near $199, while volume reached about 15 million shares.

The stock moved lower today because Qualcomm still needs to prove that growth outside smartphones can become large enough to support its valuation. The average analyst price target sits around $180, below the recent share price, while the consensus rating remains Hold. That gap matters because investors are not yet treating Qualcomm like a clear AI infrastructure winner, especially compared with Nvidia, which trades around 31x earnings, while Qualcomm trades around 21x. Broadcom, AMD, and Marvell are also more directly tied to AI accelerators, custom silicon, and data center spending, which is why Qualcomm still needs clearer proof that its data center and edge AI strategy can scale.

This week, Qualcomm’s Bernstein conference appearance gave investors a clearer look at the company’s diversification strategy. CEO Cristiano Amon said the handset business remains artificially constrained by memory supply, but Qualcomm can see a Q3 bottom because it is “significantly undershipping to consumer demand.” He also said Samsung share is now north of 70%, automotive remains supported by a $45 billion pipeline and a year-end run rate near $6 billion, IoT is approaching a $2 billion quarterly business, and custom ASIC shipments are expected to begin in calendar 2026 before data center revenue becomes material in fiscal 2027.

The company still has positive offsets. Qualcomm recently reported revenue of $10.6 billion and non-GAAP EPS of $2.65, guided Q3 fiscal 2026 non-GAAP EPS to $2.10 to $2.30, raised its quarterly dividend to $0.92 per share, and authorized a $20 billion buyback. It also announced a collaboration with SLB on edge AI solutions for energy operations, which adds another example of Qualcomm moving low-power AI chips into markets beyond phones. For investors, the setup now comes down to whether automotive chips, IoT, edge AI, and data center opportunities can become large enough to offset handset pressure while Qualcomm competes with Broadcom, AMD, and Marvell in AI and custom silicon, and with Texas Instruments, NXP, and Analog Devices in automotive and industrial chips.

Value QUALCOMM Incorporated instantly (Free with TIKR) >>>

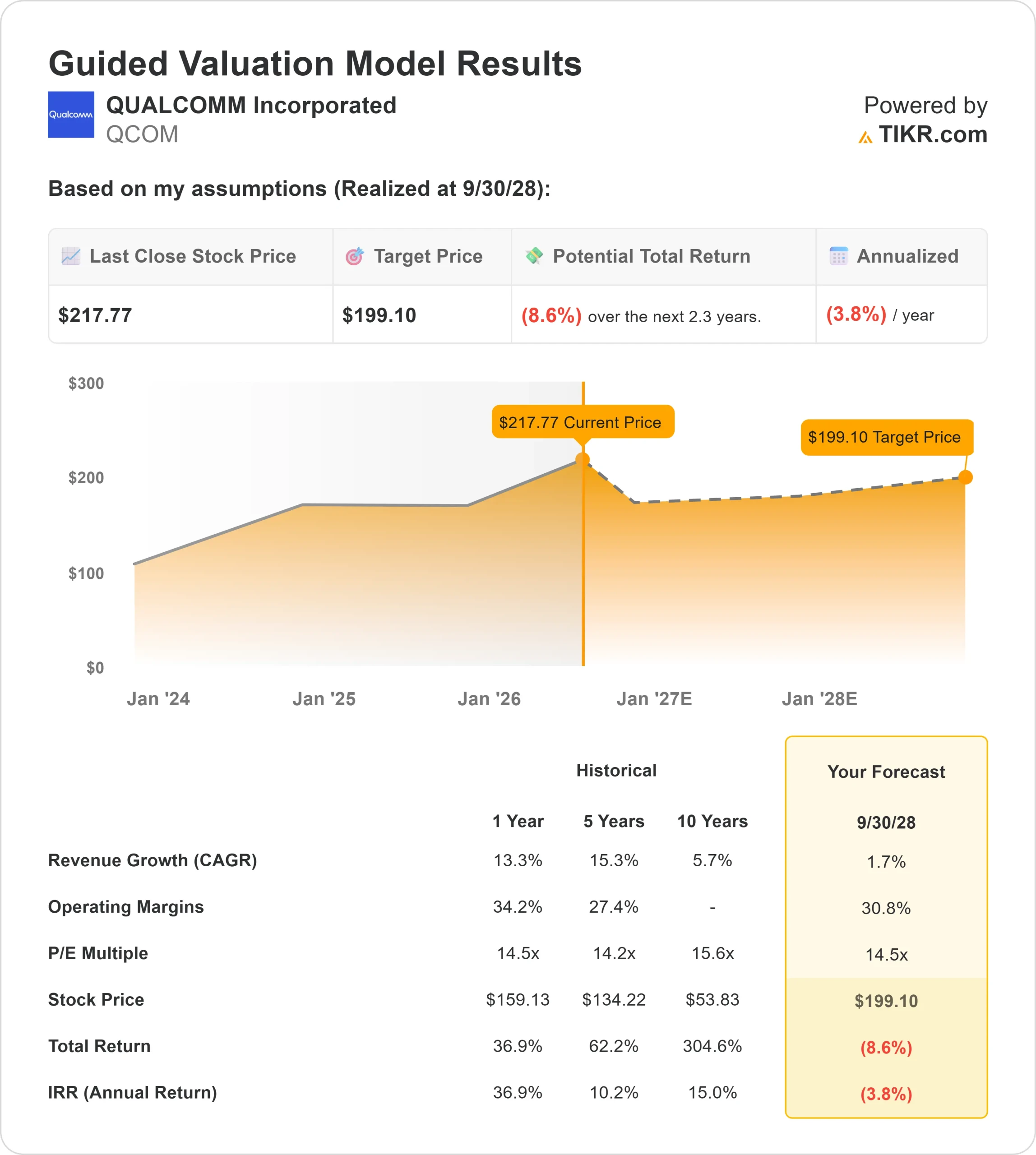

Is Qualcomm Fairly Valued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 2%

- Operating Margins: around 31%

- Exit P/E Multiple: around 15x

Qualcomm’s model points to a target price of around $200, implying about 5% upside from the recent price near $191, which suggests the stock looks close to fairly valued after today’s pullback.

Revenue growth is modeled at a low-single-digit pace because Qualcomm’s smartphone chip business remains pressured by memory supply issues and slower handset demand, while newer areas such as automotive, IoT, edge AI, and data center are still scaling from a smaller base.

Margins are modeled near 31%, which lines up with the EBIT margin chart and assumes Qualcomm can keep strong profitability from premium Snapdragon mobile chips, licensing revenue, and higher-value automotive and industrial products while still investing in AI, PCs, and data center chips.

See analysts’ growth forecasts and price targets for QUALCOMM Incorporated (It’s free) >>>

The 15x exit P/E multiple reflects a middle-ground view: Qualcomm is not being valued like Nvidia or Broadcom because its AI revenue is still early, but it also deserves more credit than a slow-growth handset supplier if diversification keeps working.

The next 12 months will likely depend on whether Qualcomm can turn that diversification story into visible growth. Automotive remains one of the cleaner drivers because design wins can support revenue over several years, while stronger premium Android demand could help stabilize the core handset business. Edge AI and industrial chips also matter because Qualcomm’s low-power processors can run AI tasks closer to where data is created, which is useful in phones, cars, energy systems, and connected devices.

At current levels, Qualcomm looks close to fairly valued, with future performance likely driven by proof that growth outside smartphones can accelerate enough to support a higher earnings multiple in 2026.

How Much Upside Does QCOM Stock Have From Here?

Investors can estimate QUALCOMM Incorporated’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value QUALCOMM Incorporated in under 60 seconds with TIKR (It’s free) >>>