Key Takeaways for News Corporation Stock

- News Corporation stock’s total revenue rose 9% year-over-year to $2.19 billion in Q3 fiscal 2026, beating Street estimates of $2.11 billion.

- Operating income grew 23% year-over-year to $221 million, with operating margins expanding from 9% to 10% over the same period.

- The three core growth pillars, Dow Jones, Digital Real Estate Services, and Book Publishing, collectively delivered 17% segment EBITDA growth, accelerating from Q2’s pace.

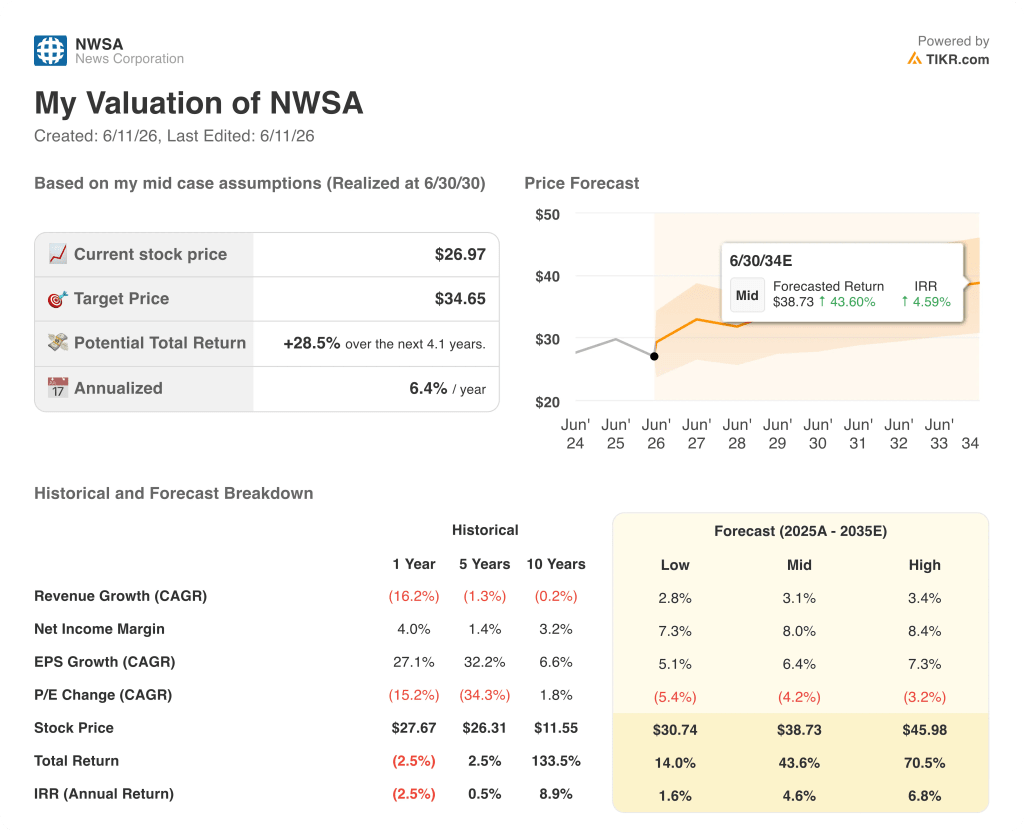

- TIKR’s mid-case values News Corporation stock at approximately $39 by June 2030, implying around 44% total return from the current price of $27.

News Corp’s Three Core Engines Accelerate Profits While the Stock Lags Behind

News Corporation (NWSA), the diversified media and information company behind The Wall Street Journal, Dow Jones, Realtor.com, HarperCollins, and REA Group, posted its twelfth consecutive quarter of year-over-year profitability growth in Q3 fiscal 2026, with total revenue rising 9% to $2.19 billion and adjusted EPS of $0.21 beating the Street estimate of $0.20.

The quarter’s driving force was the concentrated performance of three segments that management has explicitly targeted for strategic investment.

Dow Jones delivered revenue of $619 million, up 8%, with segment EBITDA of $147 million growing 11% and the margin widening 70 basis points to 23.7%, marking 13 consecutive quarters of year-over-year EBITDA growth for the unit.

The professional information business, which includes Risk and Compliance and Energy and represented approximately 40% of Dow Jones revenues, accounted for a disproportionately larger share of EBITDA given its higher-margin profile.

Risk and Compliance revenue surged 19% to $100 million, driven by customer growth, product expansion, and improved pricing, with the recently integrated Dragonfly and Oxford Analytica acquisitions contributing meaningfully during a period of heightened geopolitical demand.

Dow Jones Energy revenues grew 12% to $77 million, with customer retention holding at approximately 90%, as the shift in U.S. energy export patterns creates a new customer base that management says can be captured without proportional incremental investment.

Digital Real Estate Services reported segment EBITDA of $155 million, up 25% on a reported basis, with REA Group revenues growing 20% and Realtor.com revenues rising 10% to $148 million despite 30-year mortgage rates remaining above 6% and existing home sales near historic lows.

CFO Lavanya Chandrashekar noted that revenue per existing home sale, measured on a trailing 12-month basis as of Q3, is now more than 20% higher than the Q3 2022 level, a period that represented the prior peak for housing market activity, establishing that Realtor.com has structurally improved its monetization before the market recovery has even arrived.

HarperCollins delivered its highest third-quarter segment EBITDA since fiscal 2021, with revenue growing 8% to $555 million and margins expanding 70 basis points to 13.2%, driven by 17% growth in e-book revenues and 7% growth in audiobooks.

CEO Robert Thomson anchored his outlook on the company’s positioning as what he called in Q3 earnings call an “AI inputs company,” noting active negotiations with several AI platforms beyond the concluded Meta and OpenAI agreements, and highlighting the anticipated receipt of proceeds from the $1.5 billion Anthropic settlement later in calendar 2026: “IP powers AI. IP is an input imperative.”

The one offset in the quarter was News Media, where segment EBITDA fell $18 million year-over-year, reflecting launch and marketing costs for the California Post alongside modestly softer conditions in the UK and Australia. Management was direct in framing the context: while News Media EBITDA declined $18 million, total company EBITDA rose 18%.

Is News Corporation Stock Undervalued? The Operating Leverage Story the Market Is Missing

News Corporation stock’s operating income grew 23% year-over-year to $221 million in Q3 fiscal 2026, on revenue growth of 9%, a ratio that defines operating leverage: costs growing materially slower than revenue.

Total operating expenses in Q3 stood at $1.01 billion against gross profit of $1.23 billion, maintaining the structural gap that has widened meaningfully since the trough periods of fiscal 2024.

The income statement shows operating margins of 10% in Q3 fiscal 2026, up from 9% in Q3 fiscal 2025, with the December 2025 quarter reaching 18% operating margins, establishing the high-watermark potential of this cost structure when revenue concentration is seasonal.

Gross margins have held in the 56% to 58% range across the past eight quarters, ranging from 55% in March 2025 to 58% in June 2025, a range that demonstrates stable content economics even as the revenue mix shifts toward higher-margin professional information and digital real estate.

The most important signal in the data is the spread between gross margin stability and operating margin expansion: with gross margins roughly flat, operating income growing 23% on 9% revenue growth means SG&A is not consuming the gains, and the margin structure is beginning to reflect the business mix shift toward Dow Jones and Digital Real Estate, both of which carry segment EBITDA margins structurally above the corporate average.

NWSA Trades at NYT’s Blended Margin Despite Owning a Business That Looks More Like Thomson Reuters

News Corporation stock’s consolidated EBITDA margin of 17% in Q3 fiscal 2026 sits at near-parity with The New York Times (NYT) at 20%, a comparison that frames NWSA as a legacy media business and prices it accordingly.

Thomson Reuters (TRI) carried an EBITDA margin of 42% in the same period, a gap of roughly 25 percentage points above News Corporation stock that reflects what the market pays for a pure-play B2B data and professional information compounder with recurring, high-retention revenue.

The compression argument sits inside NWSA’s own segment data: Dow Jones, which reported a 24% segment EBITDA margin in Q3 fiscal 2026 with Risk and Compliance revenues growing 19% and customer retention in Energy holding at approximately 90%, already exceeds NYT’s consolidated margin and structurally resembles TRI far more than it resembles a print media business.

The blended NWSA margin is held down by News Media, which reported segment EBITDA of just $15 million in Q3 against Dow Jones’s $147 million, meaning the market is discounting the entire enterprise on a margin that the highest-value segment has already moved past.

TIKR’s $35 Target on NWSA Stock: What Has to Hold for the Upside to Materialize

TIKR’s base case values News Corporation stock at approximately $39 by June 2030, implying around 44% total return from the current price of $27, or roughly 5% annualized over 4.1 years.

The mid-case holds if revenue compounds at around 3% annually and net income margins expand toward 8%, assumptions grounded in the trajectory already visible in the income statement and the segment mix shift toward Dow Jones and Digital Real Estate.

The bear case, which assumes tighter revenue growth of around 3% and compressed returns, produces a stock price of around $31 by June 2030, implying roughly 14% total return and around 2% annualized, a scenario that requires housing market recovery to stall and AI licensing revenue to remain immaterial.

The bull case, anchored by accelerating AI content licensing revenue, Realtor.com monetization recovery as mortgage rates eventually decline, and continued Risk and Compliance market share gains in a $3.7 billion addressable market growing at 11% to 13% annually, produces a stock price of around $46 by June 2030, implying roughly 71% total return and around 7% annualized.

Is News Corporation stock a buy right now?

News Corporation stock trades at $27 against a TIKR mid-case target of approximately $39 by June 2030, implying around 44% total return.

The investment case rests on operating leverage in Dow Jones and Digital Real Estate outpacing the structural decline in News Media, which is already well-understood by the market.

Adjusted EPS of $0.21 beat the $0.20 Street estimate in Q3, and management has guided for continued strong performance in Q4.

What is News Corporation’s outlook for AI licensing revenue?

Management confirmed active negotiations with multiple AI platforms beyond the existing Meta and OpenAI agreements, describing AI content licensing as a multi-tiered opportunity involving both large horizontal AI companies and specialist vertical firms requiring both archive and current content.

The company also expects to begin receiving its share of the $1.5 billion Anthropic settlement later in calendar year 2026. No specific revenue figure for AI licensing was disclosed on the call.

Should You Invest in News Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up News Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track News Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NWSA stock on TIKR for Free →